- シンクタンクならニッセイ基礎研究所 >

- 経済 >

- 経済予測・経済見通し >

- Japan's Economic Outlook for Fiscal 2021 to 2023

2021年11月24日

文字サイズ

- 小

- 中

- 大

■Summary

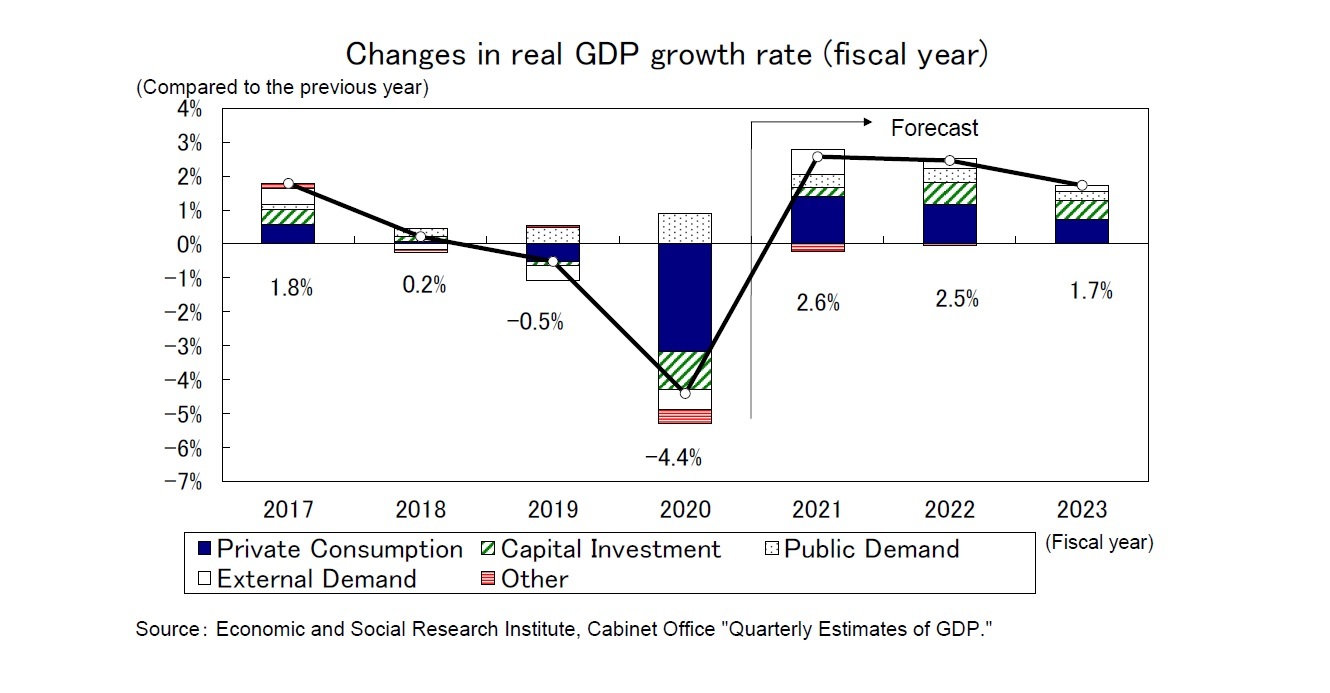

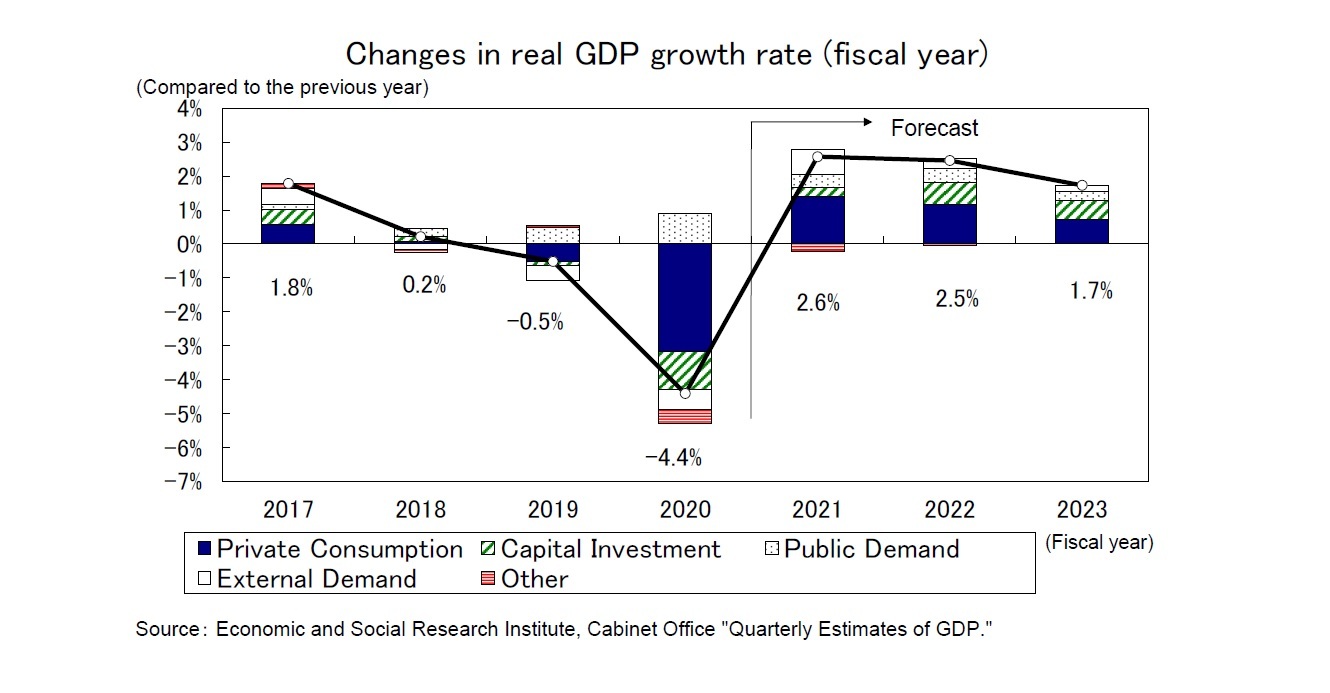

<Real GDP growth rate: 2.6% in FY 2021, 2.5% in FY 2022, 1.7% in FY 2023>

- In the July–September quarter of 2021, real GDP posted an annualized contraction of 3.0%, the first negative growth in two quarters, as private consumption, housing investment, and capital investment all declined sharply due to the state of emergency and supply constraints.

- In the October–December quarter of 2021, real GDP is forecast to post annual growth of 7.3%, mainly due to strong growth in private consumption following the lifting of the state of emergency. However, there are many risk factors, including prolonged supply constraints such as a shortage of semiconductors, deteriorating corporate profits due to worsening terms of trade, a decline in the real purchasing power of households, and tighter activity restrictions due to the spread of the coronavirus.

- The real GDP growth rate is expected to be 2.6% in FY 2021, 2.5% in FY 2022 and 1.7% in FY 2023. Although the state of emergency has been lifted, the pace of recovery in consumption will be slow after the rapid decline in the coronavirus crisis, partly because of continued fears about infectious diseases.

- Real GDP is expected to surpass its pre-coronavirus level (October–December quarter of 2019) in the April–June quarter of 2022 and return to its most recent peak before the consumption tax rate hike ( July–September quarter of 2019) in the April–June quarter of 2023.

■Index

1. In the July–September period of 2021, real GDP decreased by an annualized rate of

3.0% from the previous period

・Increasing outflow of income overseas due to deterioration in terms of trade

2. Real GDP growth rate is expected to be 2.6% in FY 2021, 2.5% in FY 2022 and 1.7%

in FY 2023

・Service consumption will pick up after the state of emergency's cancellation

・High levels of savings, cash and deposits can significantly boost consumption

・Real GDP will surpass its most recent peak in FY 2023

・Price Outlook

1. In the July–September period of 2021, real GDP decreased by an annualized rate of

3.0% from the previous period

・Increasing outflow of income overseas due to deterioration in terms of trade

2. Real GDP growth rate is expected to be 2.6% in FY 2021, 2.5% in FY 2022 and 1.7%

in FY 2023

・Service consumption will pick up after the state of emergency's cancellation

・High levels of savings, cash and deposits can significantly boost consumption

・Real GDP will surpass its most recent peak in FY 2023

・Price Outlook

(2021年11月24日「Weekly エコノミスト・レター」)

このレポートの関連カテゴリ

各種レポート配信をメールでお知らせ。読み逃しを防ぎます!

各種レポート配信をメールでお知らせ。読み逃しを防ぎます!

03-3512-1836

経歴

- ・ 1992年:日本生命保険相互会社

・ 1996年:ニッセイ基礎研究所へ

・ 2019年8月より現職

・ 2010年 拓殖大学非常勤講師(日本経済論)

・ 2012年~ 神奈川大学非常勤講師(日本経済論)

・ 2018年~ 統計委員会専門委員

斎藤 太郎のレポート

| 日付 | タイトル | 執筆者 | 媒体 |

|---|---|---|---|

| 2025/10/31 | 2025年7-9月期の実質GDP~前期比▲0.7%(年率▲2.7%)を予測~ | 斎藤 太郎 | Weekly エコノミスト・レター |

| 2025/10/31 | 鉱工業生産25年9月-7-9月期の生産は2四半期ぶりの減少も、均してみれば横ばいで推移 | 斎藤 太郎 | 経済・金融フラッシュ |

| 2025/10/31 | 雇用関連統計25年9月-女性の正規雇用比率が50%に近づく | 斎藤 太郎 | 経済・金融フラッシュ |

| 2025/10/30 | 潜在成長率は変えられる-日本経済の本当の可能性 | 斎藤 太郎 | 基礎研レポート |

新着記事

-

2025年11月07日

フィリピンGDP(25年7-9月期)~民間消費の鈍化で4.0%成長に減速、電子部品輸出は堅調 -

2025年11月07日

次回の利上げは一体いつか?~日銀金融政策を巡る材料点検 -

2025年11月07日

個人年金の改定についての技術的なアドバイス(欧州)-EIOPAから欧州委員会への回答 -

2025年11月07日

中国の貿易統計(25年10月)~輸出、輸入とも悪化。対米輸出は減少が続く -

2025年11月07日

英国金融政策(11月MPC公表)-2会合連続の据え置きで利下げペースは鈍化

お知らせ

-

2025年07月01日

News Release

-

2025年06月06日

News Release

-

2025年04月02日

News Release

【Japan's Economic Outlook for Fiscal 2021 to 2023】【シンクタンク】ニッセイ基礎研究所は、保険・年金・社会保障、経済・金融・不動産、暮らし・高齢社会、経営・ビジネスなどの各専門領域の研究員を抱え、様々な情報提供を行っています。

Japan's Economic Outlook for Fiscal 2021 to 2023のレポート Topへ- 新型コロナウイルス

- ウィズコロナ・アフターコロナ

- 生成AI・AI

- IoT

- デジタルトランスフォーメーション(DX)

- フィンテック(FinTech)

- キャッシュレス

- デジタル通貨

- デジタルプラットフォーム

- マイナンバー

- MaaS、CASE

- SDGs

- ESG

- 気候変動

- カーボンニュートラル・脱炭素社会

- サステナビリティ

- ウェルビーイング

- 生物多様性

- イデコ(iDeCo)

- 新NISA・NISA

- 日本銀行

- 人手不足・人材不足

- 働き方改革

- 人的資本経営

- 従業員エンゲージメント

- テレワーク・在宅勤務

- ダイバーシティ(多様性)社会

- 外国人雇用・就労

- 労働政策

- 地域包括ケア・地域共生社会

- 認知症

- 金融(ファイナンシャル)ジェロントロジー

- 全世代型社会保障

- 社会保障・税改革

- 医療・介護制度改革

- 健康寿命

- 健康経営

- 格差・貧困

- 世代間格差

- パワーカップル

- 未婚化

- プレコンセプションケア

- 少子高齢化

- 東京一極集中

- インバウンド

- シェアリングエコノミー

- Z世代・α世代

- エンタメ

- オフィスレントインデックス

- 生命保険事業概況

- 米中貿易摩擦

- 米国

- 中国

- 欧州

- アジア・新興国

- 韓国

- ASEAN

- 統計

- 確定拠出年金

- 企業型DC

- 資産所得倍増プラン

- 金融リテラシー

- 住宅リテラシー

- 年金制度改革

- インド

- 経済安全保障

- 供給網(サプライ・チェーン)

- 消費者物価指数(CPI)│日本

- 雇用統計│日本

- 鉱工業生産指数│日本

- 貿易統計│日本

- 法人企業統計│日本

- QE速報・予測

- 日銀金融政策決定会合

- 日銀短観│日本

- 資金循環統計│日本

- 景気ウォッチャー調査│日本

- 地域経済報告(さくらレポート)

- マネタリーベース│日本

- GDP等│米国

- FOMC(連邦公開市場委員会)│米国

- 住宅販売・着工│米国

- 雇用統計│米国

- 米個人所得・支出|米国

- ECB政策理事会│欧州

- ユーロ圏消費者物価指数

- ユーロ圏GDP

- ユーロ圏失業率

- 英国雇用関連統計

- 英国金融政策

- 英国GDP

- 将来人口推計

- 人口動態統計

- 宿泊旅行統計

- 中国GDP

- インドGDP

- タイGDP

- マレーシアGDP

- フィリピンGDP

- インドネシアGDP

- ベトナムGDP

- ロシアGDP

- ブラジルGDP

- IMF世界経済見通し

- 企業物価指数

- インド消費者物価

研究領域

Copyright © NLI Research Institute. All rights reserved.