- NLI Research Institute >

- Economics >

- Japan’s Economic Outlook for Fiscal Years 2022 to 2024 (November 2022)

16/11/2022

Japan’s Economic Outlook for Fiscal Years 2022 to 2024 (November 2022)

Economic Research Department Executive Research Fellow Taro Saito

Font size

- S

- M

- L

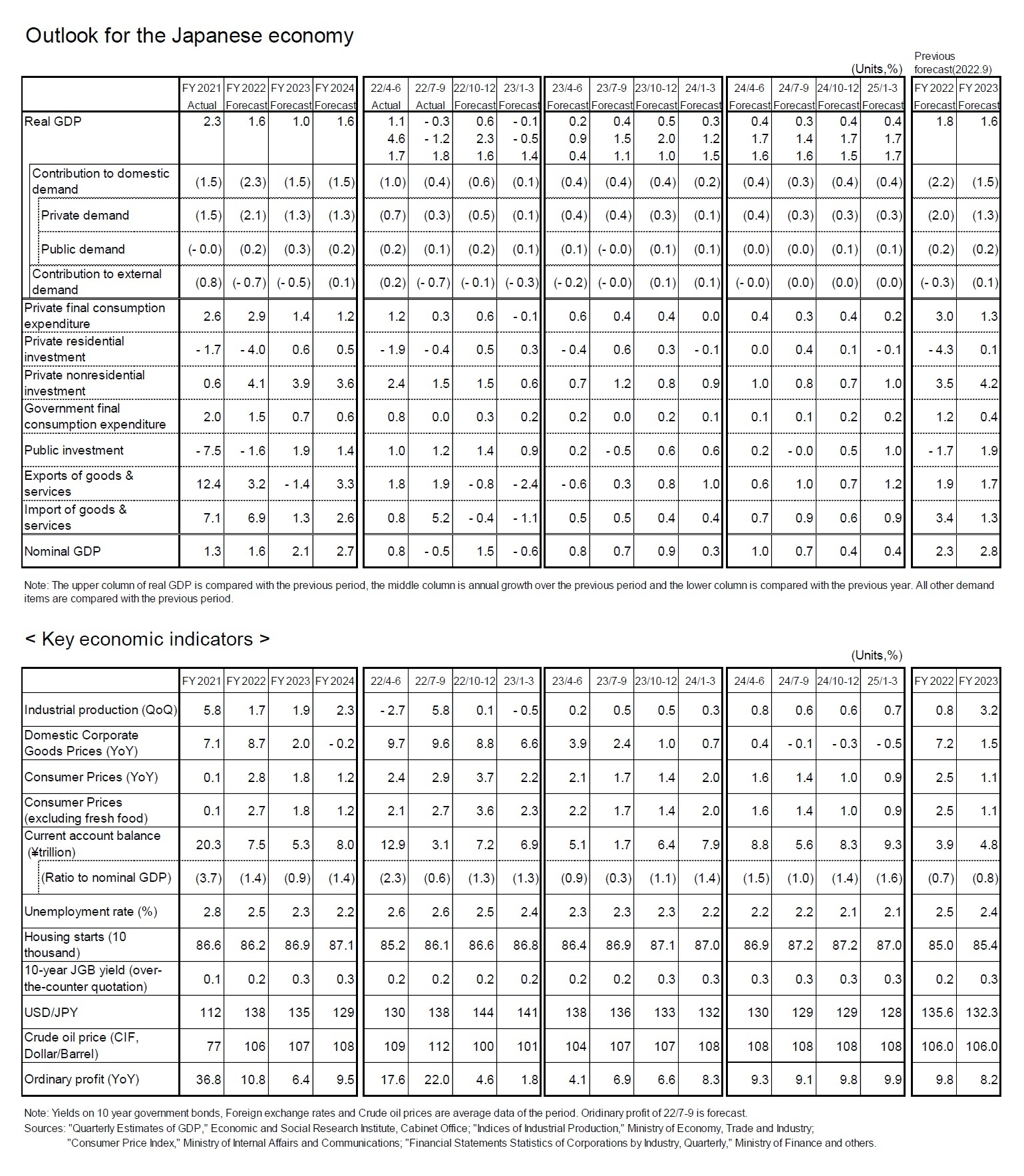

(Real GDP will surpass its most recent peak in FY 2024.)

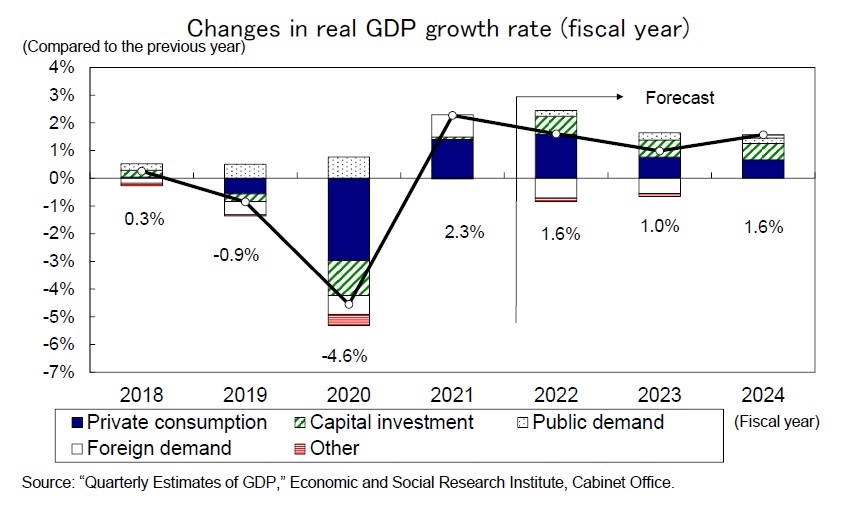

In the July–September quarter of 2022, the economy contracted for the first time in four quarters. However, this was mainly due to a significant increase in imports and does not mean that the economy is deteriorating. The economy is judged to be on a recovery track as solid activity continues, mainly in consumption and capital investment.

In the October–December quarter of 2022, real GDP is expected to grow at an annual rate of 2.3%. While exports are expected to decline due to sluggish overseas economies, private consumption will grow at a higher rate due to a boost from nationwide travel support, and capital investment will remain strong on the back of high corporate earnings. However, the forecast for the January–March quarter of 2023 is for a slight contraction of 0.5% on an annualized basis from the previous quarter, due to a larger decline in exports amid continued negative growth in Europe and the United States and a renewed slowdown in private consumption in response to the spread of COVID-19. Although exports are not expected to be a driver of the economy once FY 2023 starts, positive growth is expected to continue in the absence of special action restrictions, mainly due to increased private consumption and capital investment backed by substantial household savings and corporate earnings.

In the July–September quarter of 2022, the economy contracted for the first time in four quarters. However, this was mainly due to a significant increase in imports and does not mean that the economy is deteriorating. The economy is judged to be on a recovery track as solid activity continues, mainly in consumption and capital investment.

In the October–December quarter of 2022, real GDP is expected to grow at an annual rate of 2.3%. While exports are expected to decline due to sluggish overseas economies, private consumption will grow at a higher rate due to a boost from nationwide travel support, and capital investment will remain strong on the back of high corporate earnings. However, the forecast for the January–March quarter of 2023 is for a slight contraction of 0.5% on an annualized basis from the previous quarter, due to a larger decline in exports amid continued negative growth in Europe and the United States and a renewed slowdown in private consumption in response to the spread of COVID-19. Although exports are not expected to be a driver of the economy once FY 2023 starts, positive growth is expected to continue in the absence of special action restrictions, mainly due to increased private consumption and capital investment backed by substantial household savings and corporate earnings.

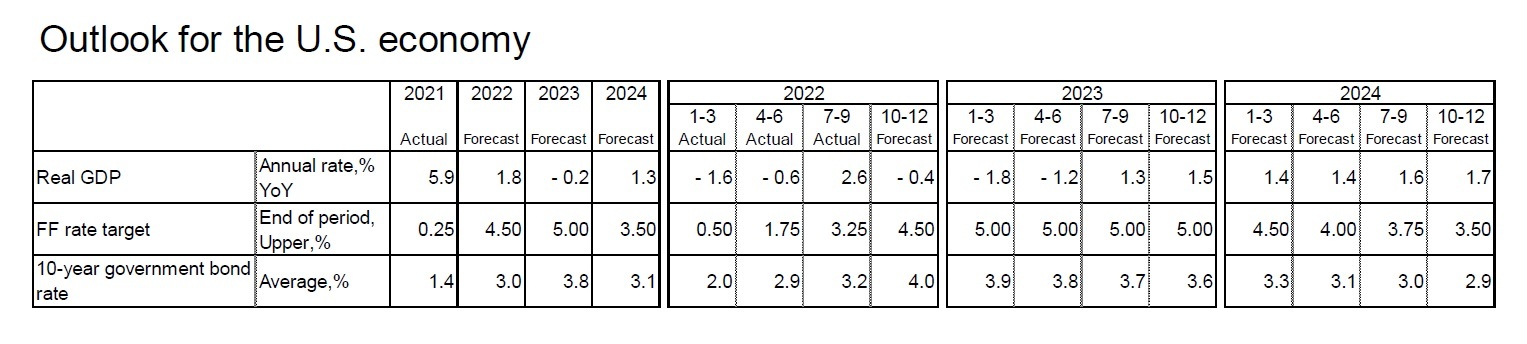

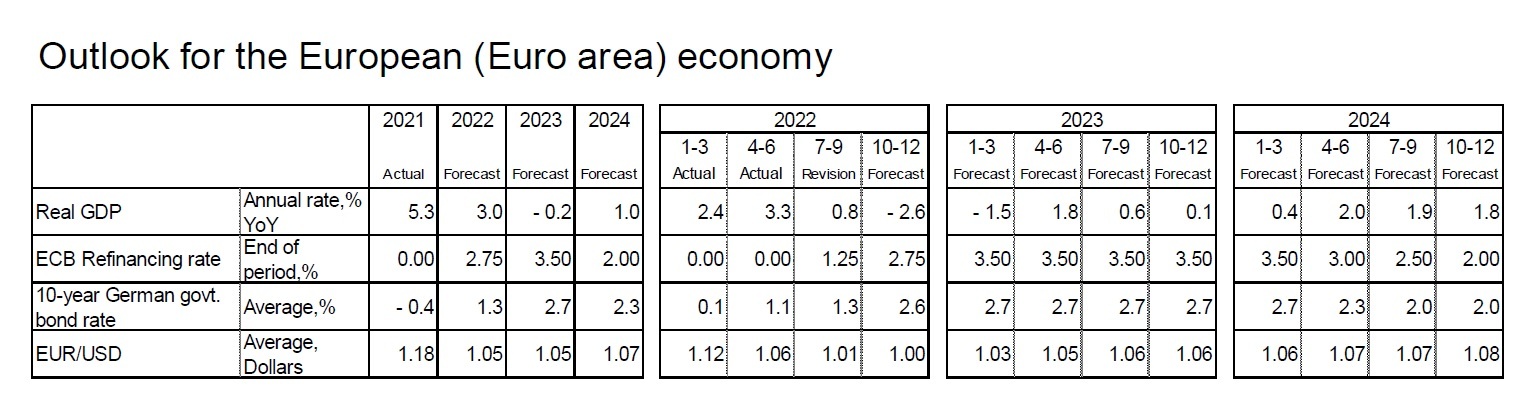

For now, the current scenario indicates that negative growth in the United States and the euro area will be small, while the recovery trend in Japan will be maintained. However, if the recessions in the United States and the euro area intensify, a recession in Japan will become inevitable. Other downside risks are China’s zero-COVID policy, curbs on economic activity due to winter electricity shortages, and uncertainty about policy responses to the spread of COVID-19.

For now, the current scenario indicates that negative growth in the United States and the euro area will be small, while the recovery trend in Japan will be maintained. However, if the recessions in the United States and the euro area intensify, a recession in Japan will become inevitable. Other downside risks are China’s zero-COVID policy, curbs on economic activity due to winter electricity shortages, and uncertainty about policy responses to the spread of COVID-19.It is difficult to completely eradicate COVID-19 and the number of new positive cases is expected to rise and fall in the future. To ensure that economic and social activities are not restricted even in the event of an outbreak, COVID-19 should be reviewed under the Infectious Diseases Act and medical care systems should be developed.

Real GDP is expected to grow 1.6% in FY 2022, 1.0% in FY 2023, and 1.6% in FY 2024. In FY 2023, private consumption and capital investment will remain strong in domestic demand, but the growth rate will decline mainly due to a decline in exports against the backdrop of a slowdown in overseas economies. The growth rate will be higher in FY 2024 as exports start to increase in response to the recovery of overseas economies.

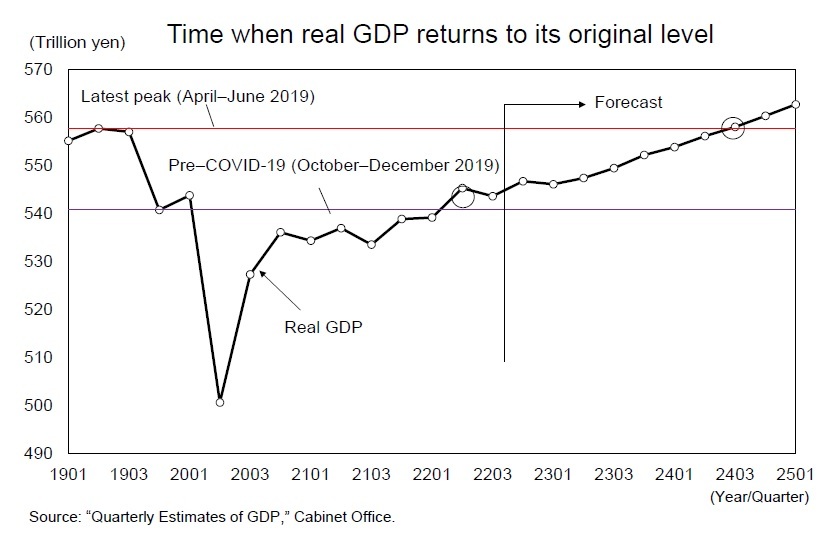

Real GDP is expected to grow 1.6% in FY 2022, 1.0% in FY 2023, and 1.6% in FY 2024. In FY 2023, private consumption and capital investment will remain strong in domestic demand, but the growth rate will decline mainly due to a decline in exports against the backdrop of a slowdown in overseas economies. The growth rate will be higher in FY 2024 as exports start to increase in response to the recovery of overseas economies.Although the economy contracted in the July–September quarter of 2022, the level in real GDP is 0.5% higher than that in the pre–COVID-19 period (October–December 2019). However, due to the impact of the consumption tax rate hike, Japan’s economy contracted at an annualized rate of 11.2% in the October–December quarter of 2019 compared to the previous quarter, and the level of economic activity dropped significantly before the impact of the COVID-19 pandemic became apparent. Compared to the most recent peak in the April–June quarter of 2019, real GDP was down 2.5% in the July–September quarter of 2022, which means there is still a long way to go to normalize the economy.

We expect real GDP to recover its most recent peak in the April–June quarter of 2019 in the July–September quarter of 2024.

(Price outlook)

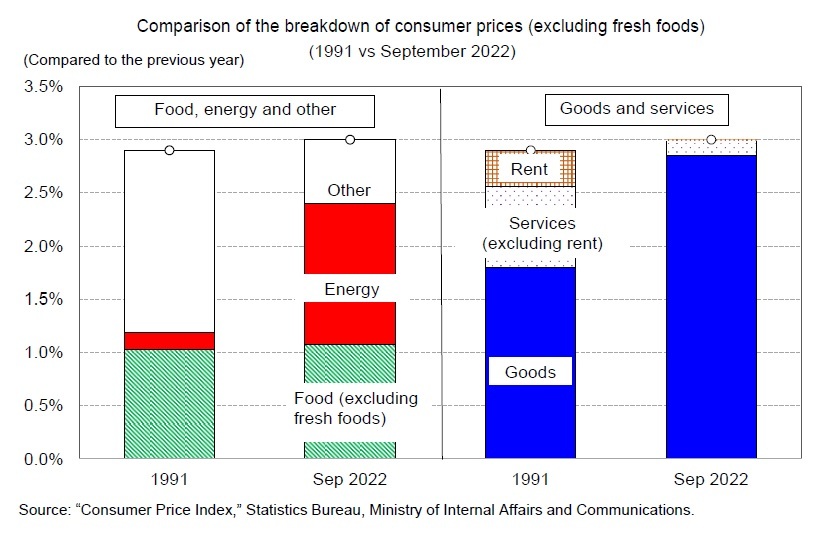

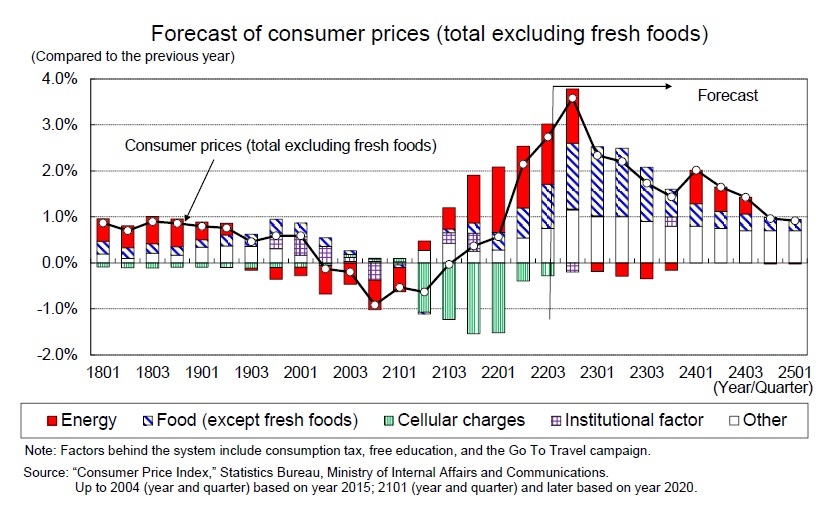

Consumer prices (total CPI excluding fresh foods; hereafter core CPI) rose to 3.0% in September 2022 from a year earlier, mainly due to higher energy and food prices, and excluding the impact of the consumption tax rate hike, rose to 3%, the first 3% increase in 31 years and one month since August 1991. In October, core CPI inflation is expected to accelerate to the mid 3% range, as the impact of steep cuts in mobile phone bills passes and food (excluding fresh food) growth accelerates sharply.

Consumer prices (total CPI excluding fresh foods; hereafter core CPI) rose to 3.0% in September 2022 from a year earlier, mainly due to higher energy and food prices, and excluding the impact of the consumption tax rate hike, rose to 3%, the first 3% increase in 31 years and one month since August 1991. In October, core CPI inflation is expected to accelerate to the mid 3% range, as the impact of steep cuts in mobile phone bills passes and food (excluding fresh food) growth accelerates sharply.

The reason for the current price increases is very different than from 31 years ago. The main cause of the recent rise in prices is a sharp rise in the cost of energy and food (excluding fresh foods), which has been driven by rising prices of resources and grains and the weakening yen. Energy and food contributed more than 80% of the 3.0% core CPI increase in September 2022. In comparison, energy and food contributed only 40% in 1991.

By goods and services, almost all of the rise in prices in September 2022 came from goods, while the contribution of services was almost zero. Declines in household-related services and medical and welfare services, as well as low rent growth, are contributing to the low service prices. In contrast, goods contributed about 60% and services about 40% in 1991.

By goods and services, almost all of the rise in prices in September 2022 came from goods, while the contribution of services was almost zero. Declines in household-related services and medical and welfare services, as well as low rent growth, are contributing to the low service prices. In contrast, goods contributed about 60% and services about 40% in 1991.Service prices are closely linked to wages, and they will not rise as wages continue to stagnate. A rise in service prices through wage increases is a condition for stable and sustained price increases.

With U.S. interest rate hikes coming to an end around the beginning of 2023, the forecast assumes that the yen will accelerate moderately and that crude oil prices, which peaked in the middle of 2022, will rise only moderately. Therefore, although prices will continue to rise for some time in the form of price pass-through increases in raw material prices, the pace of the increase in goods prices is expected to slow after the arrival of FY 2023. However, service prices, which are currently growing at almost 0%, will rise modestly in response to higher wage increases.

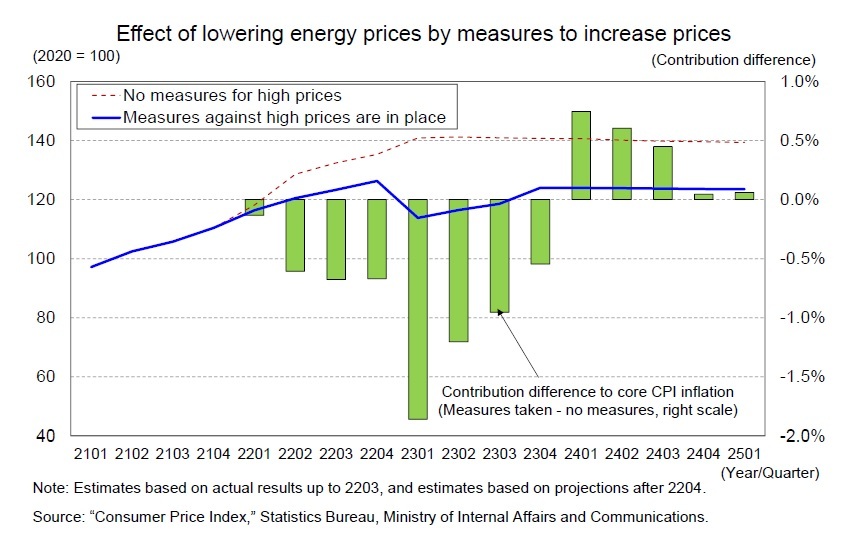

Major changes in energy prices due to policy measures against inflation will determine price trends in the future. As for energy prices, gasoline and kerosene prices have been suppressed by the mitigation measures toward drastic changes in fuel oil prices since January 2022, and the additional suppression of electricity and gas bills from January 2023 will greatly expand the suppression effect of energy prices.

Major changes in energy prices due to policy measures against inflation will determine price trends in the future. As for energy prices, gasoline and kerosene prices have been suppressed by the mitigation measures toward drastic changes in fuel oil prices since January 2022, and the additional suppression of electricity and gas bills from January 2023 will greatly expand the suppression effect of energy prices.

According to our estimates, the downward effect on core CPI inflation due to the suppression of energy prices as a result of measures against inflation will sharply increase from approximately 0.7% in July–September and October–December 2022 to nearly 2% in January–March 2023. Core CPI inflation for the October–December quarter of 2022 is expected to be 3.6%, but it would be in the 4% range if there were no inflation measures. In the January–March 2023 period, core CPI inflation is likely to decline sharply to 2.3%, mainly due to the downward effect of measures to combat inflation.

According to our estimates, the downward effect on core CPI inflation due to the suppression of energy prices as a result of measures against inflation will sharply increase from approximately 0.7% in July–September and October–December 2022 to nearly 2% in January–March 2023. Core CPI inflation for the October–December quarter of 2022 is expected to be 3.6%, but it would be in the 4% range if there were no inflation measures. In the January–March 2023 period, core CPI inflation is likely to decline sharply to 2.3%, mainly due to the downward effect of measures to combat inflation.

The downward effect of the measures against higher prices will gradually diminish after the April–June quarter of 2023, and after the January–March quarter of 2024; the rebound will push up the year-on-year rate of energy prices. The annual impact of inflation measures on core CPI inflation is expected to be −1.0% in FY 2022, −0.5% in FY 2023 and +0.3% in FY 2024. While this forecast assumes that measures to combat inflation will continue through the end of FY 2024, even with the reduction of subsidies, it should be noted that measures to combat inflation will make it difficult to gauge the trend of prices.

The downward effect of the measures against higher prices will gradually diminish after the April–June quarter of 2023, and after the January–March quarter of 2024; the rebound will push up the year-on-year rate of energy prices. The annual impact of inflation measures on core CPI inflation is expected to be −1.0% in FY 2022, −0.5% in FY 2023 and +0.3% in FY 2024. While this forecast assumes that measures to combat inflation will continue through the end of FY 2024, even with the reduction of subsidies, it should be noted that measures to combat inflation will make it difficult to gauge the trend of prices.Core CPI inflation is expected to be 2.7% year-on-year in FY 2022, 1.8% year-on-year in FY 2023 and 1.2% year-on-year in FY 2024.

Please note: The data contained in this report has been obtained and processed from various sources, and its accuracy or safety cannot be guaranteed. The purpose of this publication is to provide information, and the opinions and forecasts contained herein do not solicit the conclusion or termination of any contract.

03-3512-1836

レポート紹介

-

研究領域

-

経済

-

金融・為替

-

資産運用・資産形成

-

年金

-

社会保障制度

-

保険

-

不動産

-

経営・ビジネス

-

暮らし

-

ジェロントロジー(高齢社会総合研究)

-

医療・介護・健康・ヘルスケア

-

政策提言

-

-

注目テーマ・キーワード

-

統計・指標・重要イベント

-

媒体

- アクセスランキング

Copyright © 2016 NLI Research Institute. All rights reserved.