- NLI Research Institute >

- Economics >

- Japan’s Economic Outlook for Fiscal 2022 and 2023 (May 2022)

19/05/2022

Japan’s Economic Outlook for Fiscal 2022 and 2023 (May 2022)

Economic Research Department Executive Research Fellow Taro Saito

Font size

- S

- M

- L

■要旨

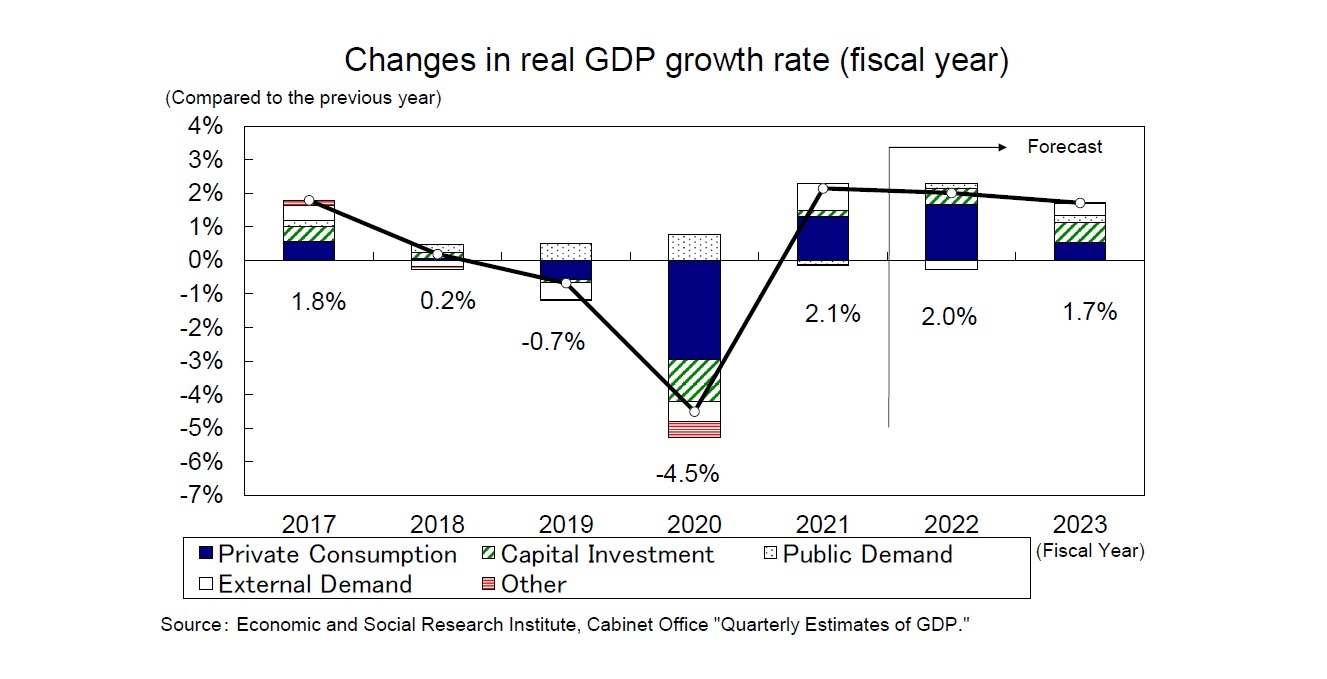

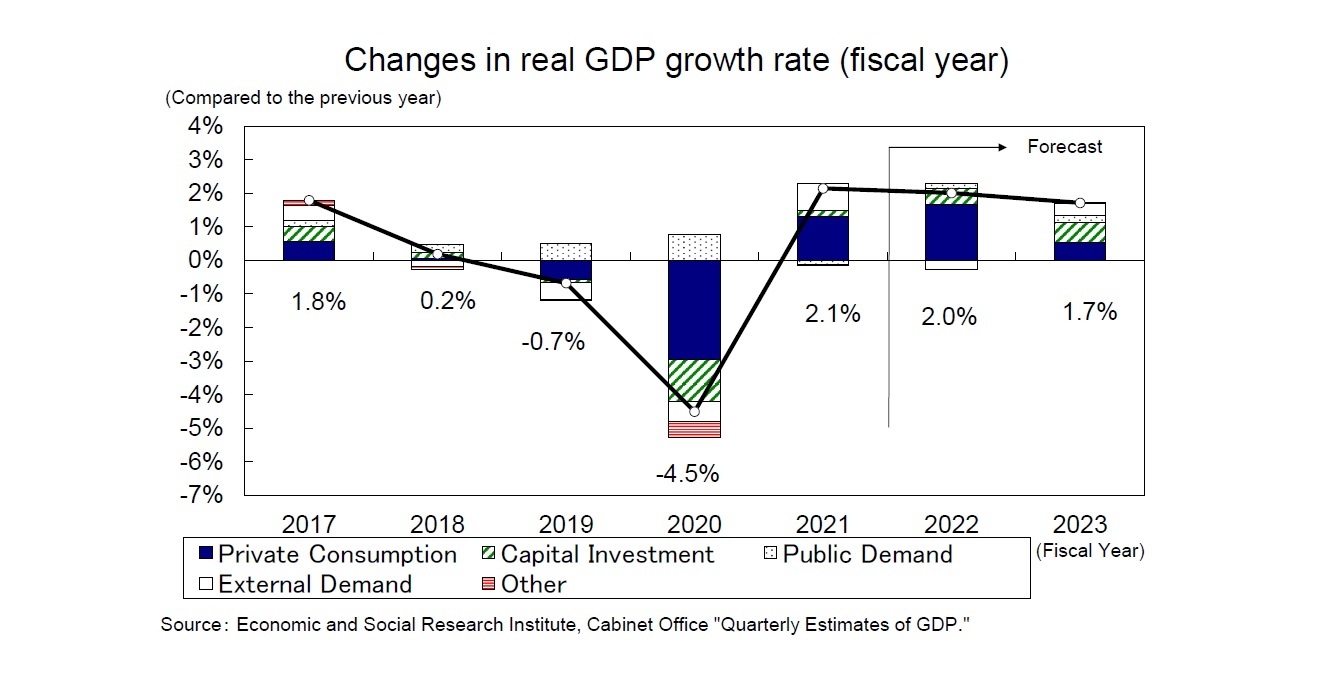

<Real GDP growth rate: 2.0% in FY 2022 and 1.7% in FY 2023>

- In the January-March quarter of 2022, real GDP posted an annualized growth rate of negative 1.0%, the first decline in 2 quarters, due to sluggish private consumption accompanying priority preventative measures and deteriorating external demand.

- Real GDP is expected to grow 2.0% in FY 2022 and 1.7% in FY 2023. In the April-June quarter of 2022, real GDP is expected to recover its pre-COVID-19 level (October-December 2019), with an annualized growth of 4.1% over the previous quarter on the back of strong private consumption growth, mainly in the form of face-to-face services.

- However, there are significant downside risks, such as a further rise in resource prices, the worsening situation in Ukraine, monetary tightening by the United States, China's zero-COVID-19 policy, and electricity shortages due to the disruption of energy supply from Russia. Furthermore, if we continue to tighten restrictions as we have in the past during another outbreak of the new COVID-19 virus, we will not see a sustainable recovery in consumption.

- The consumer price inflation (excluding fresh food) is expected to be 2.0% in FY 2022 and 0.9% in FY 2023. Although energy prices have plateaued as a result of measures to counter rising prices, it will continue to grow by about 2% in FY 2022 as a result of a growing trend of passing prices on to consumers for food and daily necessities. However, in FY 2023, when the impact of the rise in raw material prices will be over, growth will slow to less than 1%.

■目次

1. Annual decline of 1.0% in January-March 2022

・Impact of yen depreciation and high crude oil prices

2. Real growth rate is expected to be 2.0% in FY 2022 and 1.7% in FY 2023

・Consumer spending picks up after priority preventative measures end

・Accelerated pace of price increases depresses real income

・Adverse effects of higher prices can be offset by a reduction in the savings rate

・Real GDP will exceed the latest peak in FY 2023

・Outlook of current account balance

・Price outlook

1. Annual decline of 1.0% in January-March 2022

・Impact of yen depreciation and high crude oil prices

2. Real growth rate is expected to be 2.0% in FY 2022 and 1.7% in FY 2023

・Consumer spending picks up after priority preventative measures end

・Accelerated pace of price increases depresses real income

・Adverse effects of higher prices can be offset by a reduction in the savings rate

・Real GDP will exceed the latest peak in FY 2023

・Outlook of current account balance

・Price outlook

03-3512-1836

レポート紹介

-

研究領域

-

経済

-

金融・為替

-

資産運用・資産形成

-

年金

-

社会保障制度

-

保険

-

不動産

-

経営・ビジネス

-

暮らし

-

ジェロントロジー(高齢社会総合研究)

-

医療・介護・健康・ヘルスケア

-

政策提言

-

-

注目テーマ・キーワード

-

統計・指標・重要イベント

-

媒体

- アクセスランキング

Copyright © 2016 NLI Research Institute. All rights reserved.