- NLI Research Institute >

- Economics >

- Japan's Economic Outlook for Fiscal Years 2021 and 2022

17/08/2021

Japan's Economic Outlook for Fiscal Years 2021 and 2022

Economic Research Department Executive Research Fellow Taro Saito

Font size

- S

- M

- L

(Real GDP will exceed its most recent peak in FY 2023)

In 2020, the Japanese economy plunged in the first half as a result of requests for self-restraint and the issuance of the state of emergency in response to the spread of the novel coronavirus. A rapid recovery thereafter occurred at a pace faster than expected in the second half due to the resumption of economic activities following the lifting of the state of emergency. However, economic activity stagnated in the first half of 2021 following the reissuance of the state of emergency.

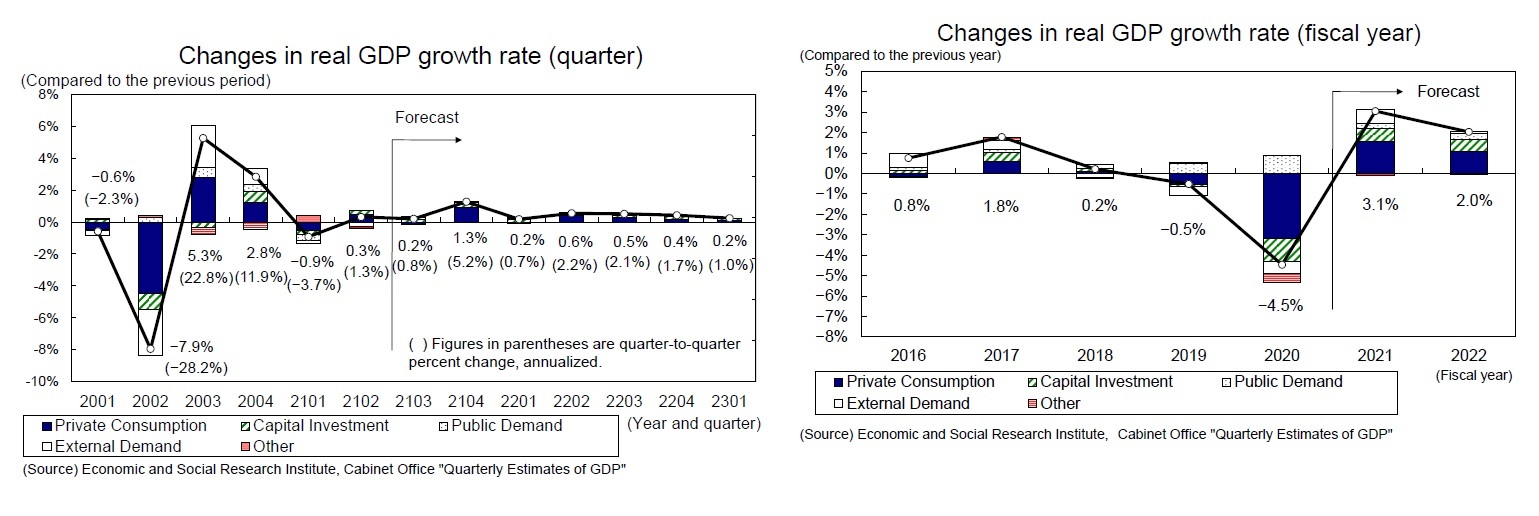

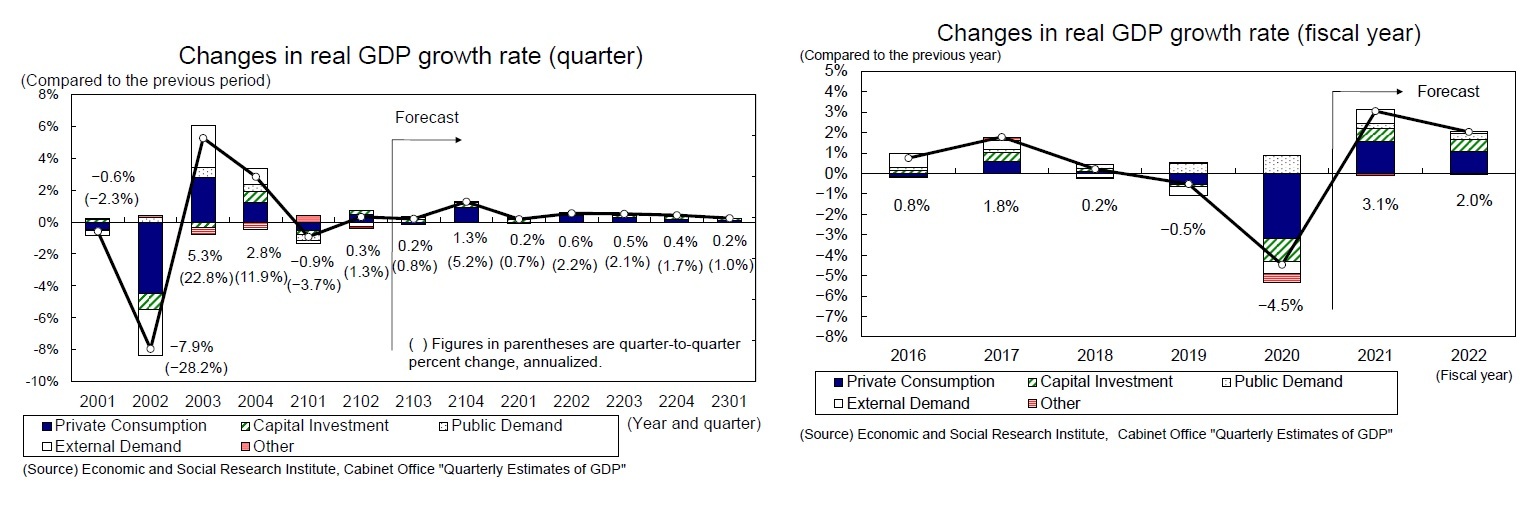

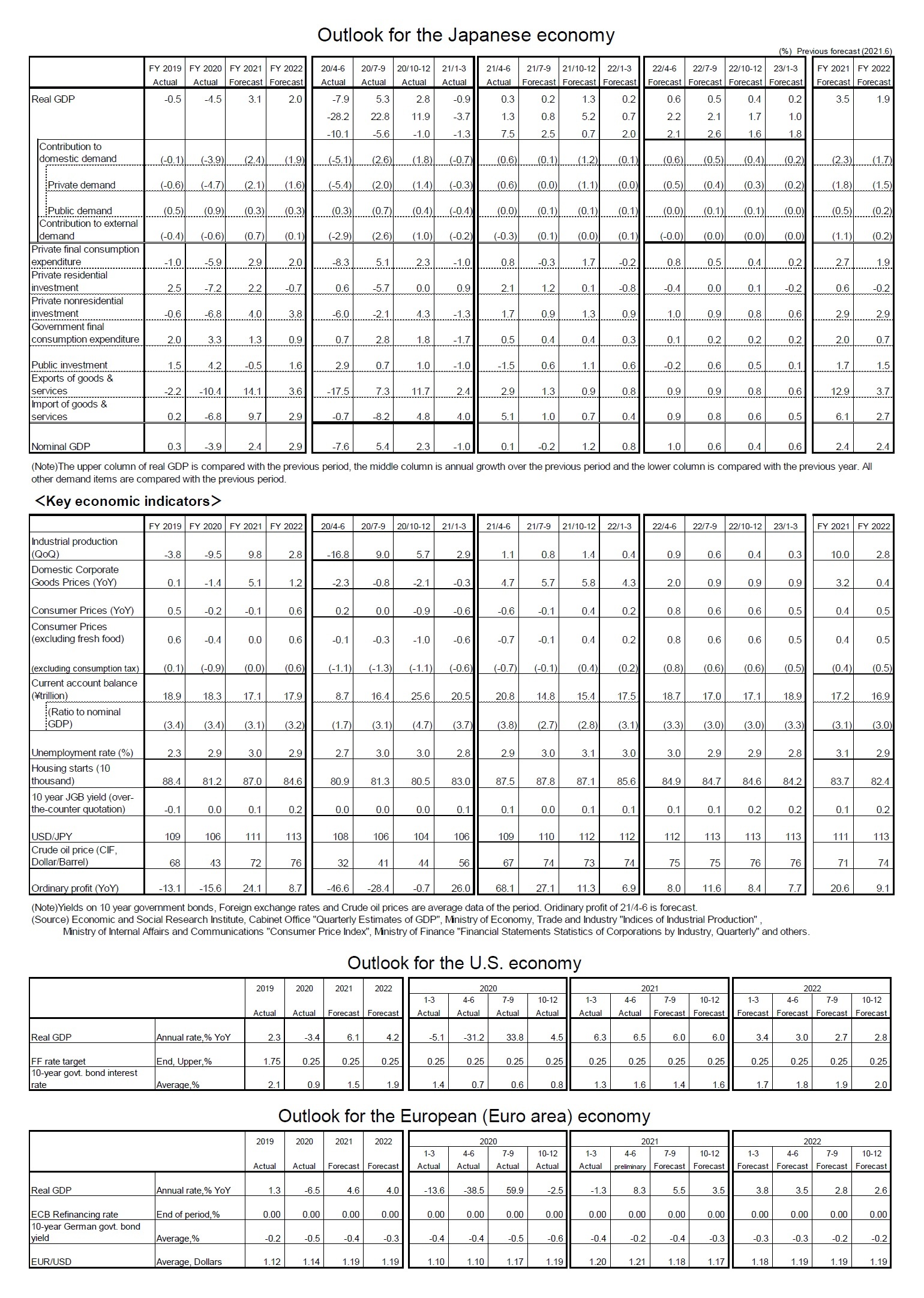

In the July–September quarter of 2021, private consumption is expected to remain sluggish at a 0.3% drop from the previous quarter due to the continuation of the declaration of the state of emergency and the expansion of the target regions. However, real GDP is expected to grow at an annual rate of 0.8% from the previous quarter, as exports will remain steady against the backdrop of a recovery in overseas economies. Housing investment and capital investment, which are less susceptible to the declaration of the state of emergency, will increase. Given the low level of economic activity, the pace of recovery will be sluggish and real GDP’s level remained below the post-coronavirus peak (October–December quarter 2020). The gap between Japan’s growth rate and that of the United States and Europe will become even clearer.

In the October–December quarter of 2021, real GDP is expected to grow at a high rate of 5.2% on an annualized basis subject to the lifting of the state of emergency. The main reason for the high growth is that the consumption of face-to-face services will pick up as a result of the easing of action restrictions. Therefore, private consumption will grow 1.7% from the previous quarter. However, we cannot deny the risk that consumption could be undermined by the intermittent issuance of priority preventative measures and the declaration of the state of emergency.

In 2020, the Japanese economy plunged in the first half as a result of requests for self-restraint and the issuance of the state of emergency in response to the spread of the novel coronavirus. A rapid recovery thereafter occurred at a pace faster than expected in the second half due to the resumption of economic activities following the lifting of the state of emergency. However, economic activity stagnated in the first half of 2021 following the reissuance of the state of emergency.

In the July–September quarter of 2021, private consumption is expected to remain sluggish at a 0.3% drop from the previous quarter due to the continuation of the declaration of the state of emergency and the expansion of the target regions. However, real GDP is expected to grow at an annual rate of 0.8% from the previous quarter, as exports will remain steady against the backdrop of a recovery in overseas economies. Housing investment and capital investment, which are less susceptible to the declaration of the state of emergency, will increase. Given the low level of economic activity, the pace of recovery will be sluggish and real GDP’s level remained below the post-coronavirus peak (October–December quarter 2020). The gap between Japan’s growth rate and that of the United States and Europe will become even clearer.

In the October–December quarter of 2021, real GDP is expected to grow at a high rate of 5.2% on an annualized basis subject to the lifting of the state of emergency. The main reason for the high growth is that the consumption of face-to-face services will pick up as a result of the easing of action restrictions. Therefore, private consumption will grow 1.7% from the previous quarter. However, we cannot deny the risk that consumption could be undermined by the intermittent issuance of priority preventative measures and the declaration of the state of emergency.

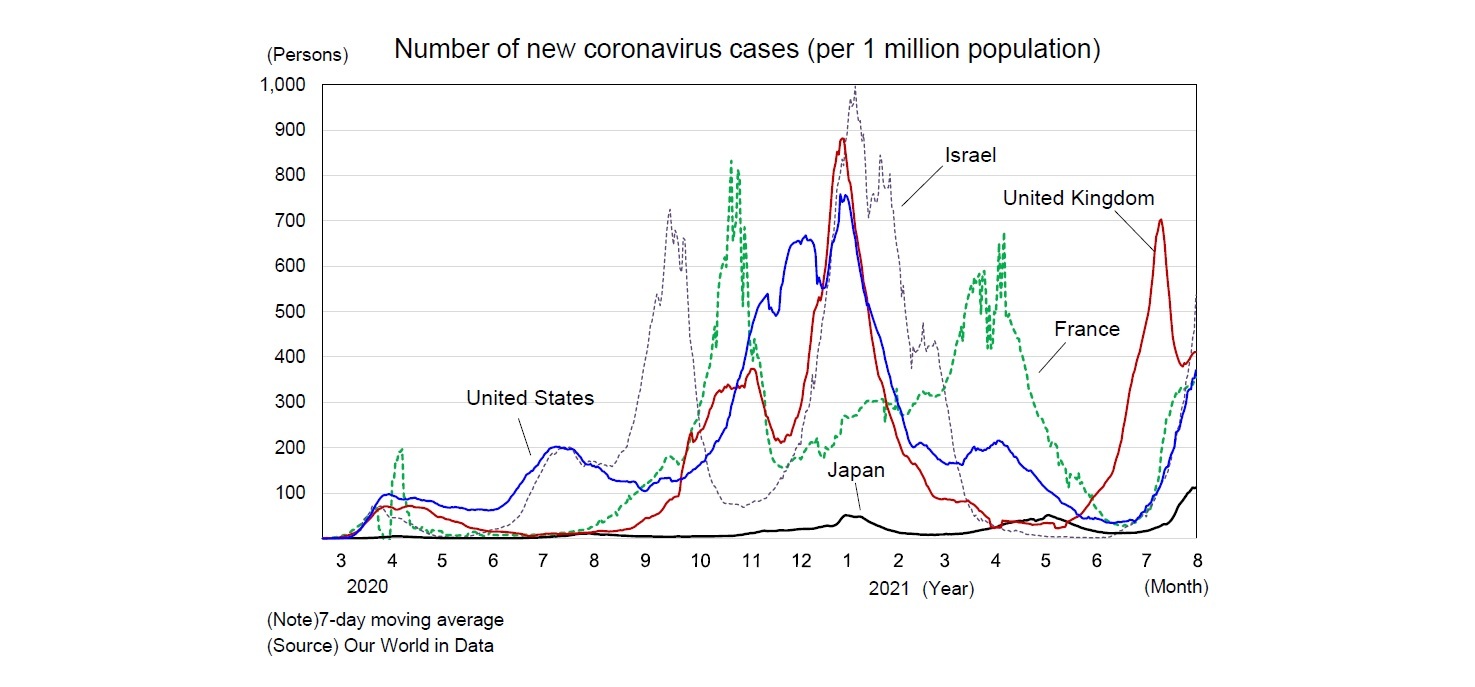

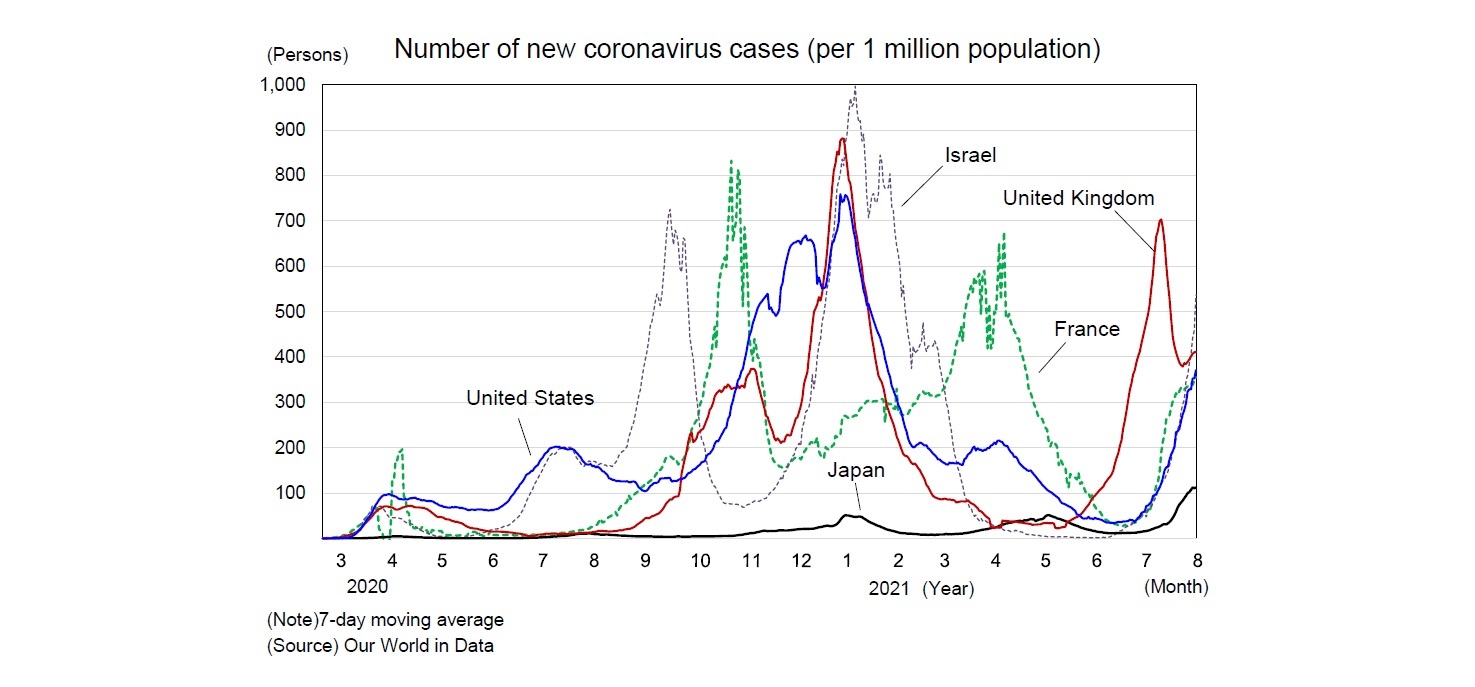

In the future, the progress of vaccinations is expected to contribute to the suppression of infection to a certain extent. However, it is unlikely that the number of infected people will drop to zero, and there is a high possibility that the number will fluctuate depending on the emergence of new variants or changes in temperature.

As is clear from the examples of other countries, the number of people infected with the novel coronavirus has fluctuated due to the emergence of variants regardless of the vaccination rate. Although the number of new infections in Japan has increased significantly, the number of new infections (per 1 million population) in the United States and the United Kingdom, where the vaccination rate is much higher than in Japan, is approximately three times higher than in Japan. Moreover, the number of new deaths (per 1 million population) is approximately 10 times higher than in Japan (as of August 15, 2021).

As is clear from the examples of other countries, the number of people infected with the novel coronavirus has fluctuated due to the emergence of variants regardless of the vaccination rate. Although the number of new infections in Japan has increased significantly, the number of new infections (per 1 million population) in the United States and the United Kingdom, where the vaccination rate is much higher than in Japan, is approximately three times higher than in Japan. Moreover, the number of new deaths (per 1 million population) is approximately 10 times higher than in Japan (as of August 15, 2021).

Every time the number of new coronavirus cases increases, measures to curb the spread of the disease, such as asking people to take time off or refraining from going out, could prolong the economic slump.

Real GDP is forecast to grow by 3.1% in FY 2021, 2.0% in FY 2022. On the one hand, even if the restrictions on economic activities are eased, consumer spending will not recover in earnest because social distancing and other measures will continue to curb consumption of face-to-face services such as dining out and travel. Private consumption is expected to grow modestly by 2.9% in FY 2021 and 2.0% in FY 2022, after the sharp decline of 5.9% in FY 2020.

On the other hand, capital investment, which has become less susceptible to the declaration of the state of emergency, increased slightly by 4.0% from the previous year in FY 2021 against the backdrop of improved corporate earnings, and will remain steady at 3.8% in FY 2022. In FY 2021, exports jumped 14.1% from the previous year on the back of the recovery of overseas economies, and a continued 3.6% robust growth in FY 2022 will likely boost the growth rate.

Real GDP is forecast to grow by 3.1% in FY 2021, 2.0% in FY 2022. On the one hand, even if the restrictions on economic activities are eased, consumer spending will not recover in earnest because social distancing and other measures will continue to curb consumption of face-to-face services such as dining out and travel. Private consumption is expected to grow modestly by 2.9% in FY 2021 and 2.0% in FY 2022, after the sharp decline of 5.9% in FY 2020.

On the other hand, capital investment, which has become less susceptible to the declaration of the state of emergency, increased slightly by 4.0% from the previous year in FY 2021 against the backdrop of improved corporate earnings, and will remain steady at 3.8% in FY 2022. In FY 2021, exports jumped 14.1% from the previous year on the back of the recovery of overseas economies, and a continued 3.6% robust growth in FY 2022 will likely boost the growth rate.

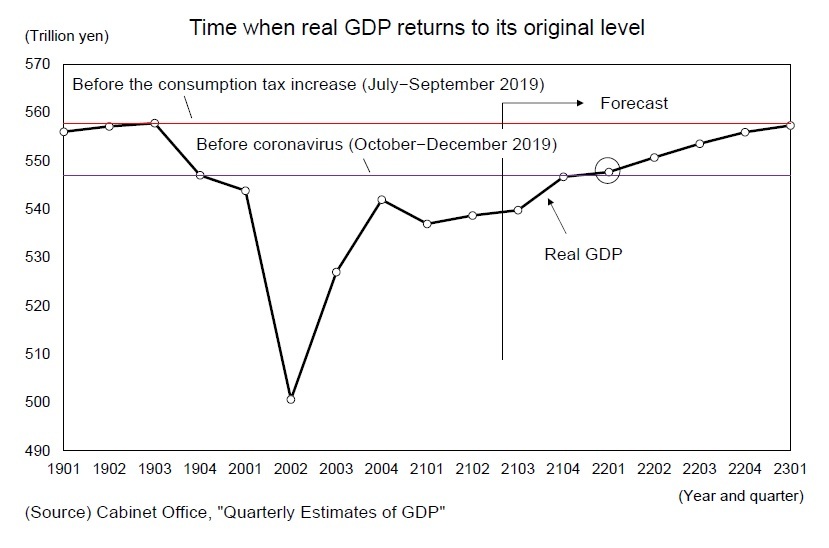

Currently, we expect the real GDP level to rise above pre-coronavirus levels (October–December quarter 2019) in the January–March quarter of 2022 and to return to its most recent peak (July–September quarter 2019) in 2023. However, it is extremely difficult to anticipate future trends in the spread of COVID-19 and the corresponding public health measures. If the government continues to implement the same policy measures as it has in the past, it will likely further delay the normalization of the economy.

Currently, we expect the real GDP level to rise above pre-coronavirus levels (October–December quarter 2019) in the January–March quarter of 2022 and to return to its most recent peak (July–September quarter 2019) in 2023. However, it is extremely difficult to anticipate future trends in the spread of COVID-19 and the corresponding public health measures. If the government continues to implement the same policy measures as it has in the past, it will likely further delay the normalization of the economy.

Please note: The data contained in this report has been obtained and processed from various sources, and its accuracy or safety cannot be guaranteed. The purpose of this publication is to provide information, and the opinions and forecasts contained herein do not solicit the conclusion or termination of any contract.

03-3512-1836

レポート紹介

-

研究領域

-

経済

-

金融・為替

-

資産運用・資産形成

-

年金

-

社会保障制度

-

保険

-

不動産

-

経営・ビジネス

-

暮らし

-

ジェロントロジー(高齢社会総合研究)

-

医療・介護・健康・ヘルスケア

-

政策提言

-

-

注目テーマ・キーワード

-

統計・指標・重要イベント

-

媒体

- アクセスランキング

Copyright © 2016 NLI Research Institute. All rights reserved.