- NLI Research Institute >

- Economics >

- Japan’s Economic Outlook for Fiscal Years 2020 and 2021

18/08/2020

Japan’s Economic Outlook for Fiscal Years 2020 and 2021

Economic Research Department Executive Research Fellow Taro Saito

Font size

- S

- M

- L

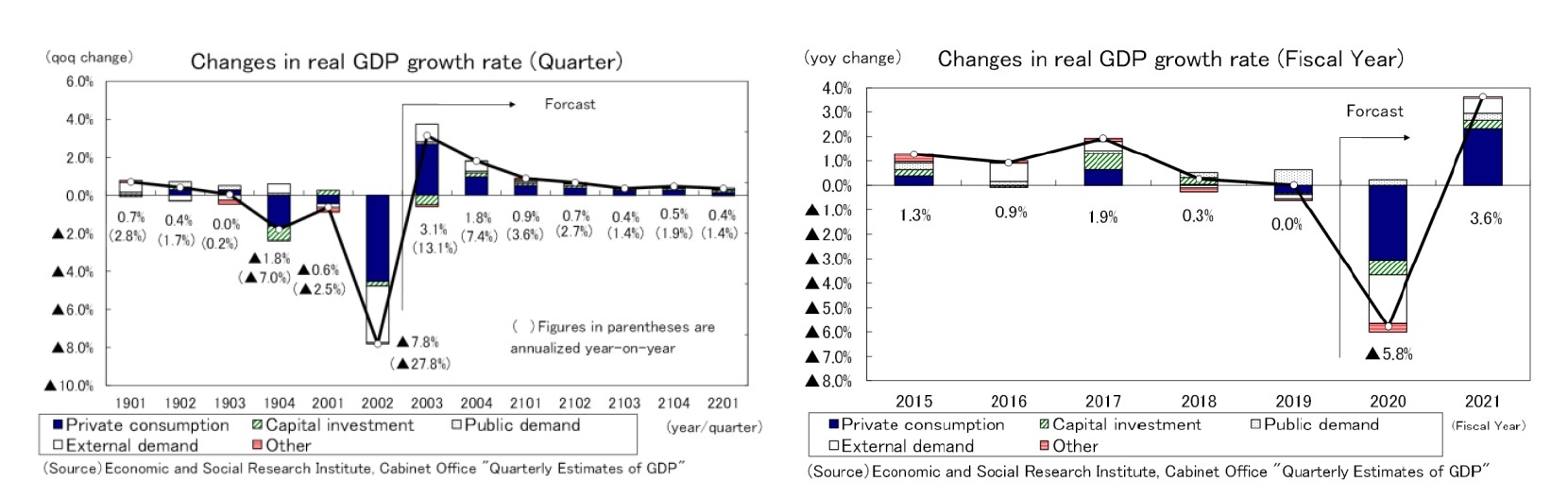

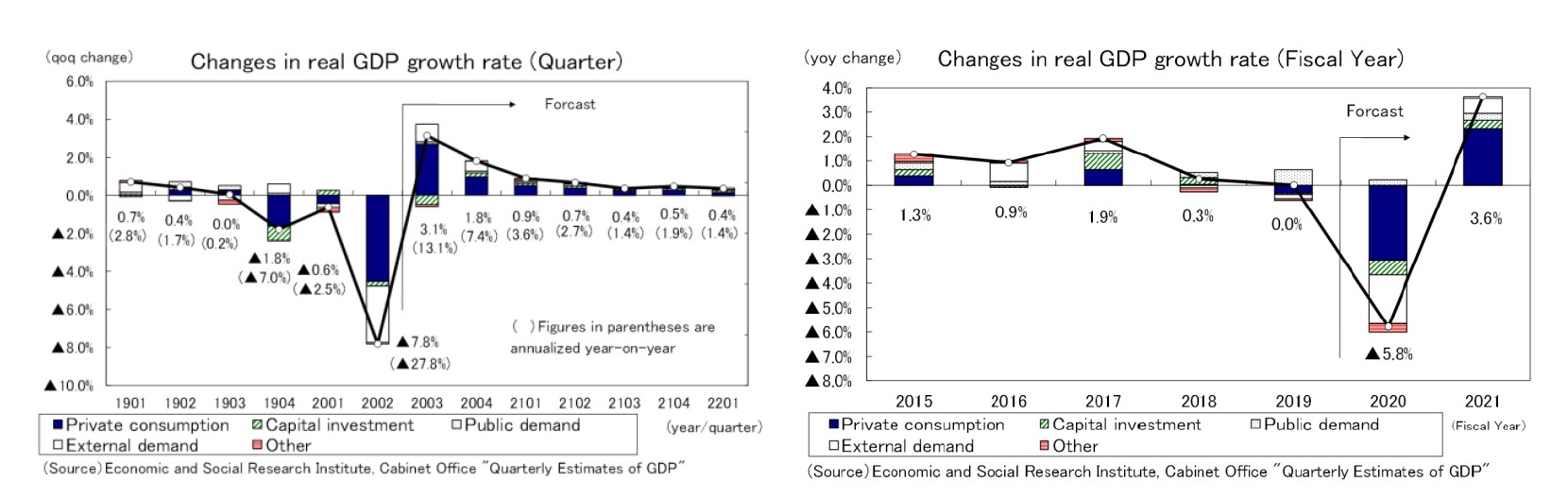

1.Record negative growth in April–June 2020 at an annualized rate of minus 27.8%

In the April–June quarter of 2020, real GDP declined by 7.8% (down 27.8% per annum) from the previous quarter, marking the third consecutive quarter of negative growth. The negative range of the growth rate exceeded that of the January–March quarter of 2009 (down 17.8% per annum), which followed the world financial crisis, and was the largest since at least 1955 (the earliest year to which GDP statistics can be traced).1

Private consumption dropped by 8.2% from the previous quarter due to self-restraint in going out and store closures following the declaration of a state of emergency in response to the spread of the new coronavirus. Capital investment decreased by 1.5%, the first decline in three quarters, due to worsening corporate earnings and growing uncertainty about the future. The use of medical institutions declined sharply to avoid infection with the new coronavirus, and government consumption declined by 0.3% from the previous quarter. As a result, public demand declined by 0.0% from the previous quarter, and domestic demand contributed minus by 4.8% (annual rate of minus 19.1%).

Exports declined by 18.5% from the previous quarter due to the rapid deterioration of overseas economies and the disappearance of inbound demand, while external demand contributed minus 3.0% (annual rate of minus 10.8%), significantly lowering the growth rate.

Real GDP fell by 10.0% from the October–December quarter of 2019 to the April–June quarter of 2020 (three quarters) due to the increase in consumption tax and outbreak of the new coronavirus infection. In comparison, the April–June quarter of 2008 to the January–March quarter of 2009—four quarters during the world financial crisis—saw a decline of more than 8.6%.

1 Simple retrospective series for 1955–1979 and 1980–1993, based on 68 SNA, 1990 basis.

Private consumption dropped by 8.2% from the previous quarter due to self-restraint in going out and store closures following the declaration of a state of emergency in response to the spread of the new coronavirus. Capital investment decreased by 1.5%, the first decline in three quarters, due to worsening corporate earnings and growing uncertainty about the future. The use of medical institutions declined sharply to avoid infection with the new coronavirus, and government consumption declined by 0.3% from the previous quarter. As a result, public demand declined by 0.0% from the previous quarter, and domestic demand contributed minus by 4.8% (annual rate of minus 19.1%).

Exports declined by 18.5% from the previous quarter due to the rapid deterioration of overseas economies and the disappearance of inbound demand, while external demand contributed minus 3.0% (annual rate of minus 10.8%), significantly lowering the growth rate.

Real GDP fell by 10.0% from the October–December quarter of 2019 to the April–June quarter of 2020 (three quarters) due to the increase in consumption tax and outbreak of the new coronavirus infection. In comparison, the April–June quarter of 2008 to the January–March quarter of 2009—four quarters during the world financial crisis—saw a decline of more than 8.6%.

1 Simple retrospective series for 1955–1979 and 1980–1993, based on 68 SNA, 1990 basis.

(Economic developments after the lifting of the declaration of the state of emergency)

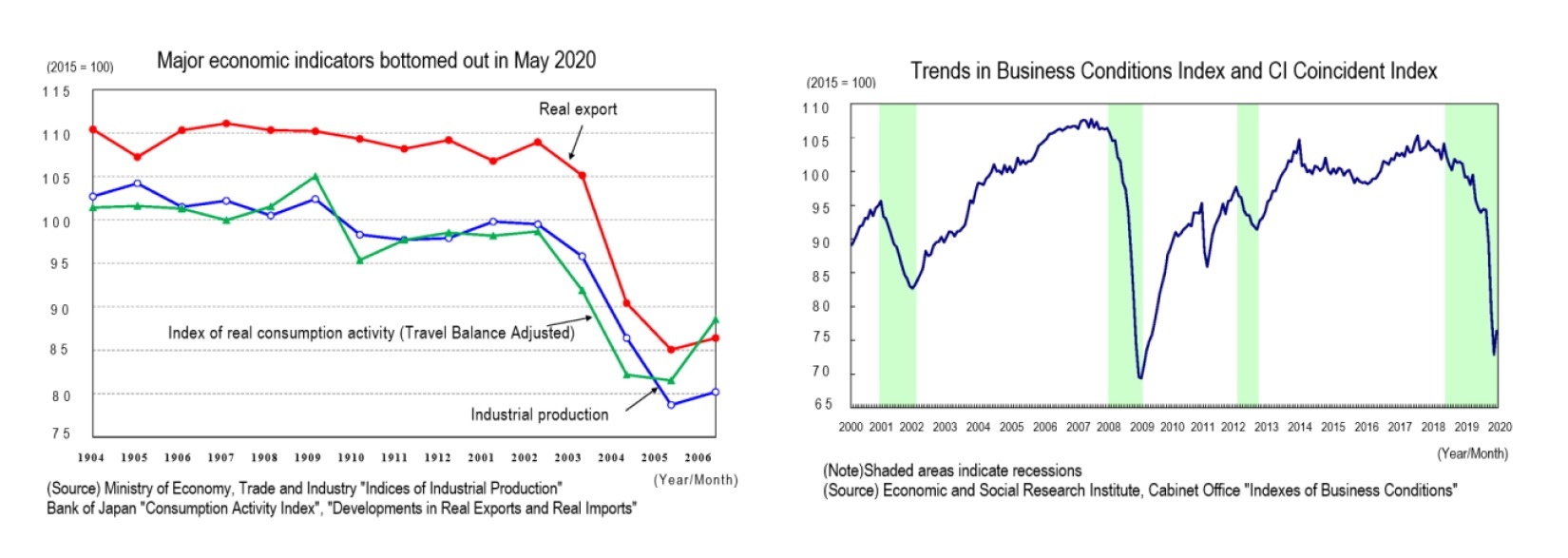

Although the April–June quarter of 2020 saw the largest negative growth on record, major economic indicators, such as production, exports, and consumption, bottomed out in May 2020 after the declaration of a state of emergency was lifted in late May. In the March–May quarter of 2020, when the impact of the new coronavirus was at its fullest, the coincident index (CI) of the business conditions index declined sharply by 21.4 points. In June, however, it increased by 3.5 points from the previous month, the first increase in five months, and all eight concordance lines (preliminary report) that make up the concordance index made a positive contribution. The recession, which began in November 2018, has already ended, and May 2020 is likely to be the trough.2

Although the April–June quarter of 2020 saw the largest negative growth on record, major economic indicators, such as production, exports, and consumption, bottomed out in May 2020 after the declaration of a state of emergency was lifted in late May. In the March–May quarter of 2020, when the impact of the new coronavirus was at its fullest, the coincident index (CI) of the business conditions index declined sharply by 21.4 points. In June, however, it increased by 3.5 points from the previous month, the first increase in five months, and all eight concordance lines (preliminary report) that make up the concordance index made a positive contribution. The recession, which began in November 2018, has already ended, and May 2020 is likely to be the trough.2

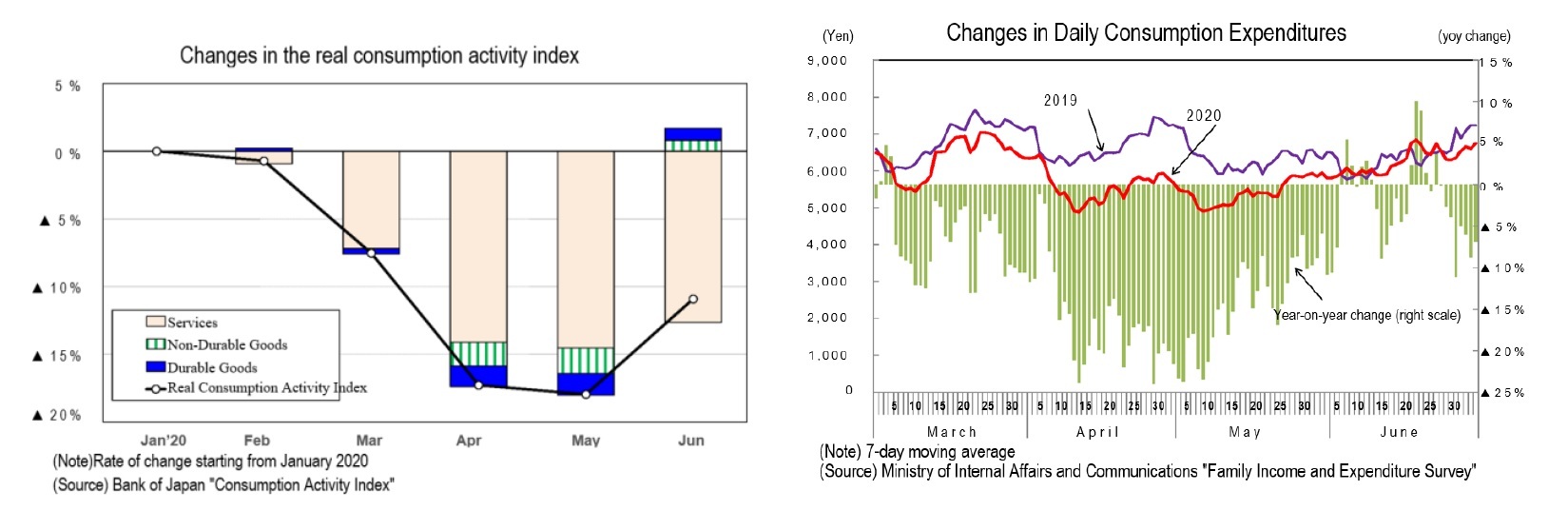

Personal consumption, which declined extremely sharply under the declaration of the state of emergency, generally bottomed out in May, though there are differences among industries. The real consumption expenditure in the Family Income and Expenditure Survey showed a double-digit decrease in April and May under the declaration of a state of emergency, falling by 11.1% and 16.2%, respectively, from the previous year. In June, however, the decrease narrowed to 1.2% and increased 13.0% from the previous month. Demand for pent-ups (suppressed demand) following the lifting of the declaration of a state of emergency and the payment of a special fixed amount of 100,000 yen per person are believed to have pushed up consumption.

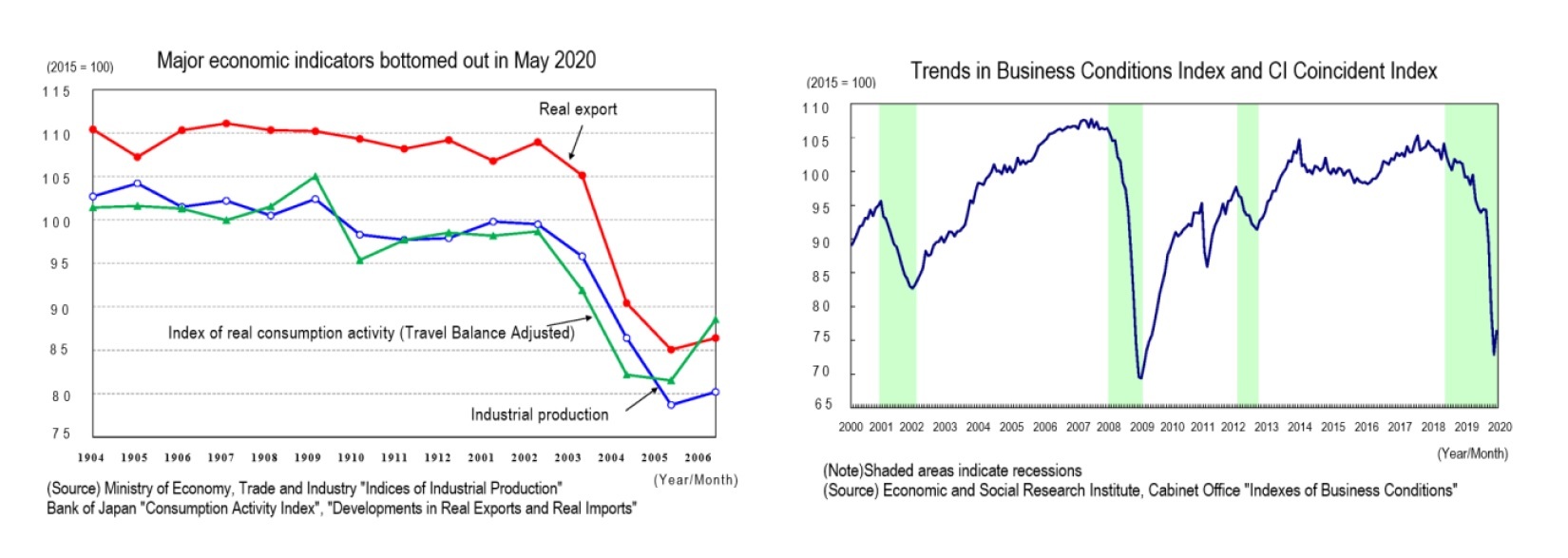

According to the Family Income and Expenditure Survey in June, the disposable income of working households rose by 18.9% in real terms from the previous year. Ordinary income, such as income from work, decreased by 1.1%, but special income increased by 1824.4% due to the payment of special fixed benefits. The actual amount of special income (per household) was 155,000 yen, up 147,000 yen from the previous year. According to the Ministry of Internal Affairs and Communications, of the total amount of 12.73 trillion yen, up to June 26 received 9.12 trillion yen (71.6%) and up to July 31 received 12.32 trillion yen (96.8%). Until July, disposable household income will be bolstered by special fixed benefits. After that, however, a decrease in work income due to the economic downturn will lead directly to a decrease in disposable income.

According to the Family Income and Expenditure Survey in June, the disposable income of working households rose by 18.9% in real terms from the previous year. Ordinary income, such as income from work, decreased by 1.1%, but special income increased by 1824.4% due to the payment of special fixed benefits. The actual amount of special income (per household) was 155,000 yen, up 147,000 yen from the previous year. According to the Ministry of Internal Affairs and Communications, of the total amount of 12.73 trillion yen, up to June 26 received 9.12 trillion yen (71.6%) and up to July 31 received 12.32 trillion yen (96.8%). Until July, disposable household income will be bolstered by special fixed benefits. After that, however, a decrease in work income due to the economic downturn will lead directly to a decrease in disposable income.

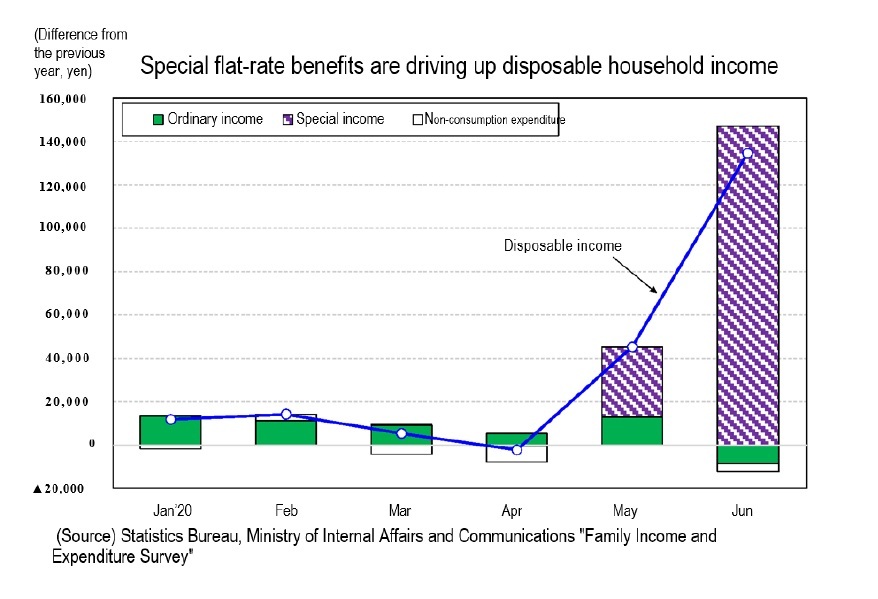

In June, consumption jumped sharply, but spending on services such as dining out, accommodation, and entertainment remained well below the levels before the new coronavirus. The real consumption activity index compiled by the Bank of Japan indicates that consumption of durable goods and non-durable goods dropped steeply in April and May following the declaration of a state of emergency. However, it rebounded rapidly in June due to the emergence of pent-up demand, exceeding the level in January 2020, before the impact of infectious disease became apparent. Meanwhile, spending on services, which were strongly affected by the government’s decision to discourage the public from going out, fell far more than those of goods during the state of emergency and rebounded only minimally in June. The level of service consumption in June was down by more than 20% from January. The heavy consumption of goods in June was partly due to consumers buying in bulk after the declaration of the state of emergency was lifted. In fact, the Family Income and Expenditure Survey showed a year-on-year increase in consumption expenditure by day in early and middle June but a year-on-year decrease again in late June.

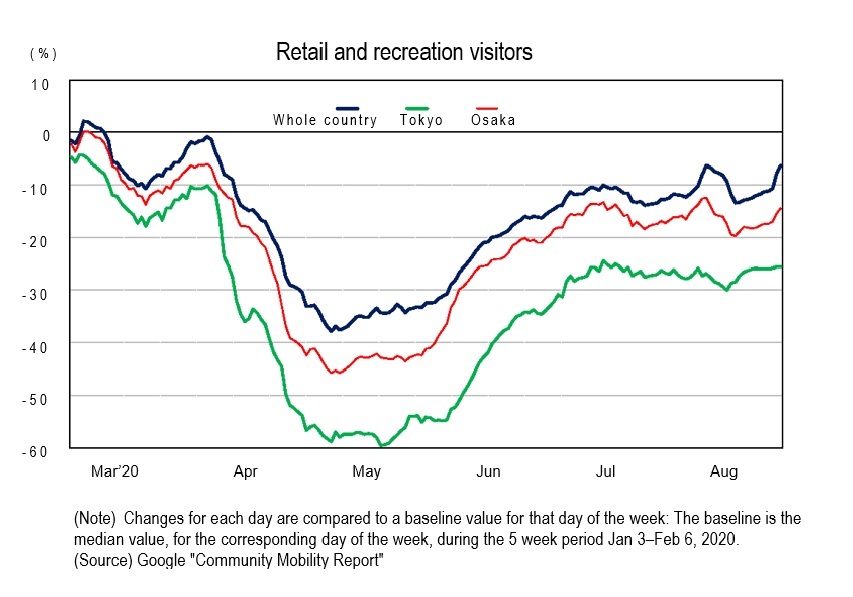

After July, as the number of people who tested positive for the new coronavirus increased again, Aichi and Okinawa prefectures declared their own state of emergency. The Tokyo metropolitan government also requested that from August 3, restaurants and karaoke bars providing alcoholic beverages shorten their business hours (closing at 10 p.m.). According to Google’s “Community mobility report,” retail and entertainment traffic (in restaurants, cafes, shopping centers, theme parks, movie theaters, etc.) increased following the lifting of the state of emergency but has leveled off since July. It is highly likely that personal consumption has been at a standstill now, mainly in service consumption, such as dining out, accommodation, and entertainment.

After July, as the number of people who tested positive for the new coronavirus increased again, Aichi and Okinawa prefectures declared their own state of emergency. The Tokyo metropolitan government also requested that from August 3, restaurants and karaoke bars providing alcoholic beverages shorten their business hours (closing at 10 p.m.). According to Google’s “Community mobility report,” retail and entertainment traffic (in restaurants, cafes, shopping centers, theme parks, movie theaters, etc.) increased following the lifting of the state of emergency but has leveled off since July. It is highly likely that personal consumption has been at a standstill now, mainly in service consumption, such as dining out, accommodation, and entertainment.

2 The Economic and Social Research Institute of the Cabinet Office, with the agreement of the Study Group on the Indexes of Business Conditions held on July 30, decided to tentatively set the peak of the 16-economic cycle at October 2018. The period of 16 cycles of economic expansion was 71 months, falling short of 14 cycles of 73 months, the longest since the end of World War II.

2. Real GDP growth rate is expected to decrease 5.8% in FY 2020 and increase 3.6% in FY 2021

(Strong growth of more than 10% per annum in the July–September 2020 quarter failed to fully recover from the decline in the April–June quarter)

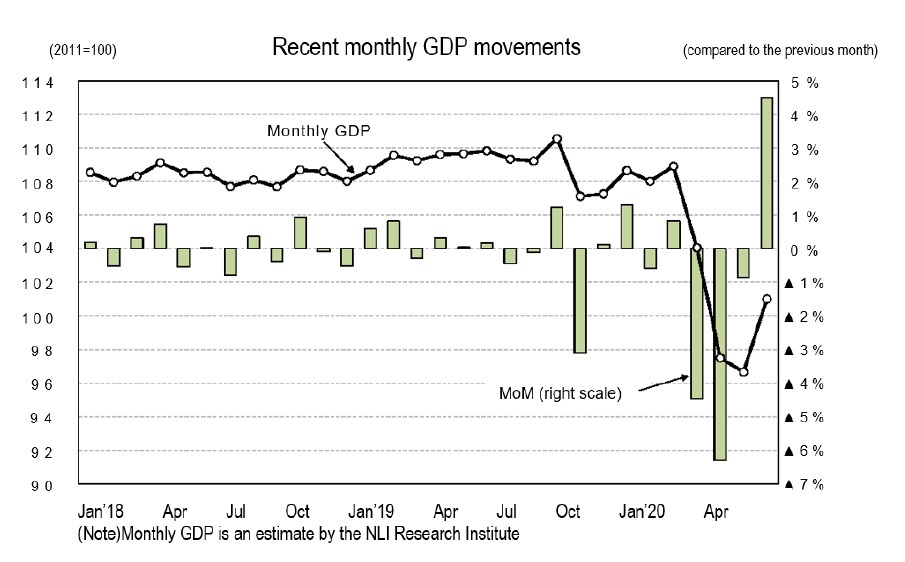

Although the April–June quarter of 2020 saw the largest negative growth on record, monthly economic activity rebounded strongly in June, when the level of activity was much higher than the average for the April–June quarter.

The monthly real GDP estimated by our Institute fell sharply in April 2020 to minus 6.3% from the previous month. In May, however, the decline narrowed to minus 0.9%, and June saw a high growth of 4.5%. Monthly GDP in June was 2.7% above the April–June average. This means that even if GDP remains flat in the July–September quarter, real GDP would grow by 2.7% (over 10% per annum) from the previous quarter.

Although the April–June quarter of 2020 saw the largest negative growth on record, monthly economic activity rebounded strongly in June, when the level of activity was much higher than the average for the April–June quarter.

The monthly real GDP estimated by our Institute fell sharply in April 2020 to minus 6.3% from the previous month. In May, however, the decline narrowed to minus 0.9%, and June saw a high growth of 4.5%. Monthly GDP in June was 2.7% above the April–June average. This means that even if GDP remains flat in the July–September quarter, real GDP would grow by 2.7% (over 10% per annum) from the previous quarter.

In the July–September quarter, we expect annual growth of 13.1%, resulting partly from a higher launch pad. However, economic activity has been slow to normalize due to a limited recovery in the consumption of services, such as dining out and accommodation, and a growing call for self-restraint following a rising number of people who tested positive for the new coronavirus in July. While real GDP growth in the July–September quarter will be high on the surface, it is reasonable to assume that the pace of recovery will be slow given the sharp decline in the April–June quarter.

In the July–September quarter, we expect annual growth of 13.1%, resulting partly from a higher launch pad. However, economic activity has been slow to normalize due to a limited recovery in the consumption of services, such as dining out and accommodation, and a growing call for self-restraint following a rising number of people who tested positive for the new coronavirus in July. While real GDP growth in the July–September quarter will be high on the surface, it is reasonable to assume that the pace of recovery will be slow given the sharp decline in the April–June quarter.

By demand category, in the July–September quarter, private consumption grew by 4.9% from the previous quarter, but the slump in service consumption will prevent it from recovering from the decline in the April–June quarter (down 8.2% from the previous quarter). The rise in housing and capital investment, which is calculated on the basis of construction progress, will be delayed until the October–December quarter. Even if domestic economic activities return to normal, it is highly likely that it will be some time before restrictions on immigration are eased or lifted globally. As a result, exports and imports are expected to recover at a slow pace, particularly in services.

The economy is believed to have bottomed out in May 2020, but the pace of recovery is likely to remain moderate after a sharp downturn. The practice of a “new way of life” is a constant factor in curbing service expenditures, such as dining out and travel. In addition, the contraction of economic activity over a substantial period has necessarily resulted in bankruptcies and a large increase in unemployment. This damage to the economic base makes it difficult for demand to return to its previous level in a short period, even with the removal of restrictions on economic activity. Declines in employee income and deteriorating corporate earnings will continue to exert downward pressure on personal consumption and capital investment.

Furthermore, people are more likely than ever to avoid crowded places, which may lead to a decline in the demand for leisure activities. Even during a normal flu outbreak, many people avoid eating out, traveling, concerts, and other events. Therefore, it is possible that people may change their leisure activities significantly if high daily numbers of infected people and deaths are reported even during an ordinary flu epidemic. While the new lifestyle prompted by the coronavirus epidemic is expected to create demand that has not existed before, it will be difficult to recover the loss of traditional demand in a short period.

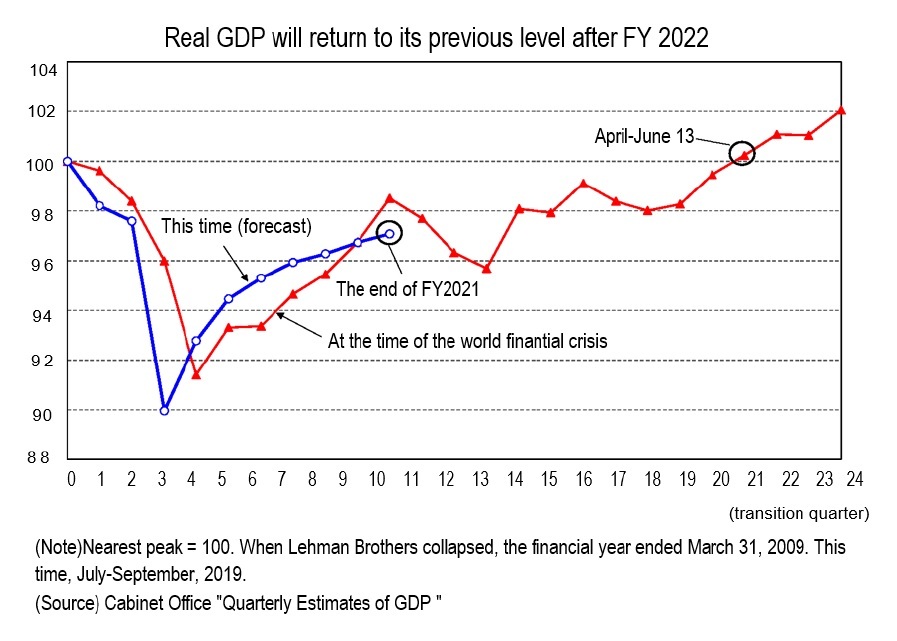

Furthermore, people are more likely than ever to avoid crowded places, which may lead to a decline in the demand for leisure activities. Even during a normal flu outbreak, many people avoid eating out, traveling, concerts, and other events. Therefore, it is possible that people may change their leisure activities significantly if high daily numbers of infected people and deaths are reported even during an ordinary flu epidemic. While the new lifestyle prompted by the coronavirus epidemic is expected to create demand that has not existed before, it will be difficult to recover the loss of traditional demand in a short period.The real GDP growth rate is forecast to be minus 5.8% in FY 2020 and positive 3.6% in FY 2021. At the end of the forecast period in January–March 2022, real GDP will be 2.9% lower than the latest peak (July–September 2019). Real GDP will not return to its previous level until FY 2022 or later.

03-3512-1836

レポート紹介

-

研究領域

-

経済

-

金融・為替

-

資産運用・資産形成

-

年金

-

社会保障制度

-

保険

-

不動産

-

経営・ビジネス

-

暮らし

-

ジェロントロジー(高齢社会総合研究)

-

医療・介護・健康・ヘルスケア

-

政策提言

-

-

注目テーマ・キーワード

-

統計・指標・重要イベント

-

媒体

- アクセスランキング

Copyright © 2016 NLI Research Institute. All rights reserved.