- NLI Research Institute >

- Real estate >

- Japanese Property Market Quarterly Review, First Quarter 2017-Focus on Coming Large Supply of Offices, Hotels and Logistics Facilities-

Japanese Property Market Quarterly Review, First Quarter 2017-Focus on Coming Large Supply of Offices, Hotels and Logistics Facilities-

Eriko Kato

Font size

- S

- M

- L

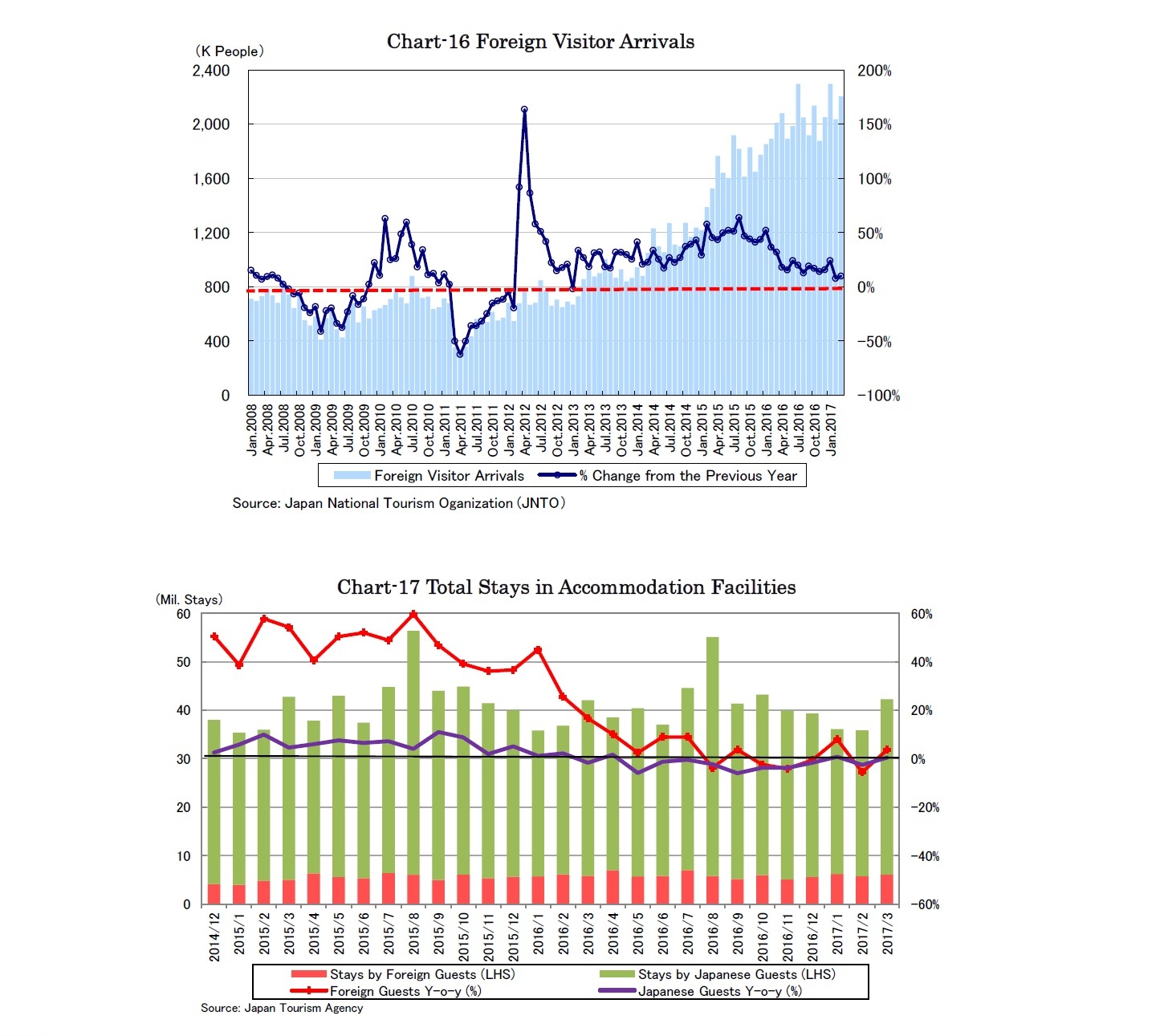

Foreign visitor arrivals which have recently stimulated hotel demand still increased moderately (Chart-16). However, the total number of stays in accommodation facilities by foreign visitors has often posted negative y-o-y growth since October 2016 (Chart-17). One of the reasons may be “Minpaku,” private residential units leased for short stays operated through Airbnb and others.

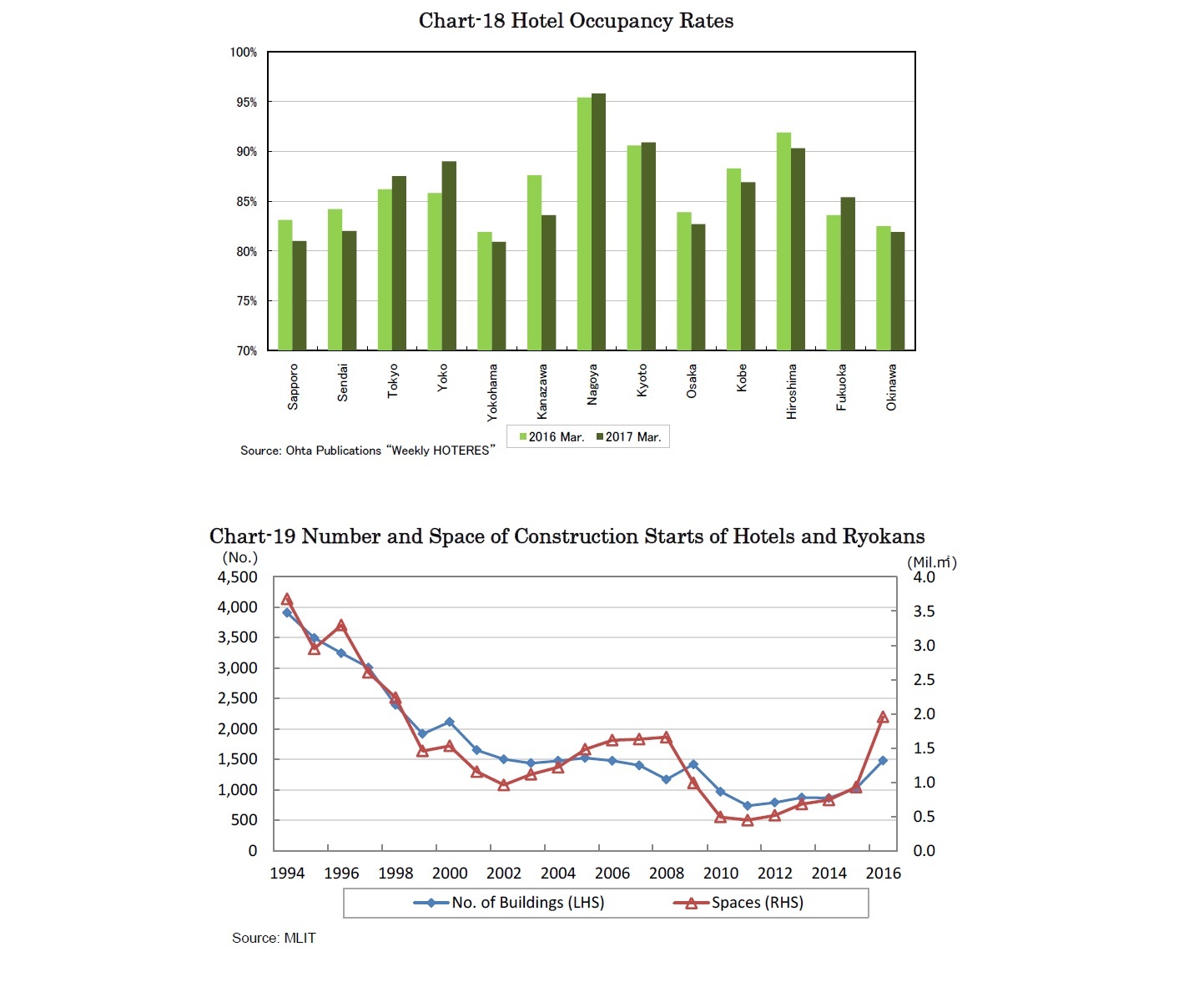

Hotel occupancy rates declined y-o-y in many cities, Yokohama and Nagoya in particular, in March (Chart-18). On the contrary, hotel occupancy rates in Fukuoka, Kyoto and Hiroshima increased y-o-y in March. Fukuoka often faces hotel shortages when live concerts are held, while Kyoto and Hiroshima have high reputations as global, sightseeing cities.

In Tokyo and Osaka, it appears expensive room rates in the city center have pushed tourists to choose to stay in the suburbs. However, hotel occupancy rates have been above the long-term average while hotel investment and development are also active. The number and space for construction starts of accommodation facilities increased by 40% and 86% y-o-y respectively in 2016 (Chart-19). Considering hotel demand has been diverted to Minpaku and the suburbs, increasing hotel developments can bring low occupancy rates in certain areas and categories. In hotel development and operation, targeting customers in appropriate categories is becoming increasingly important in order to secure demand.

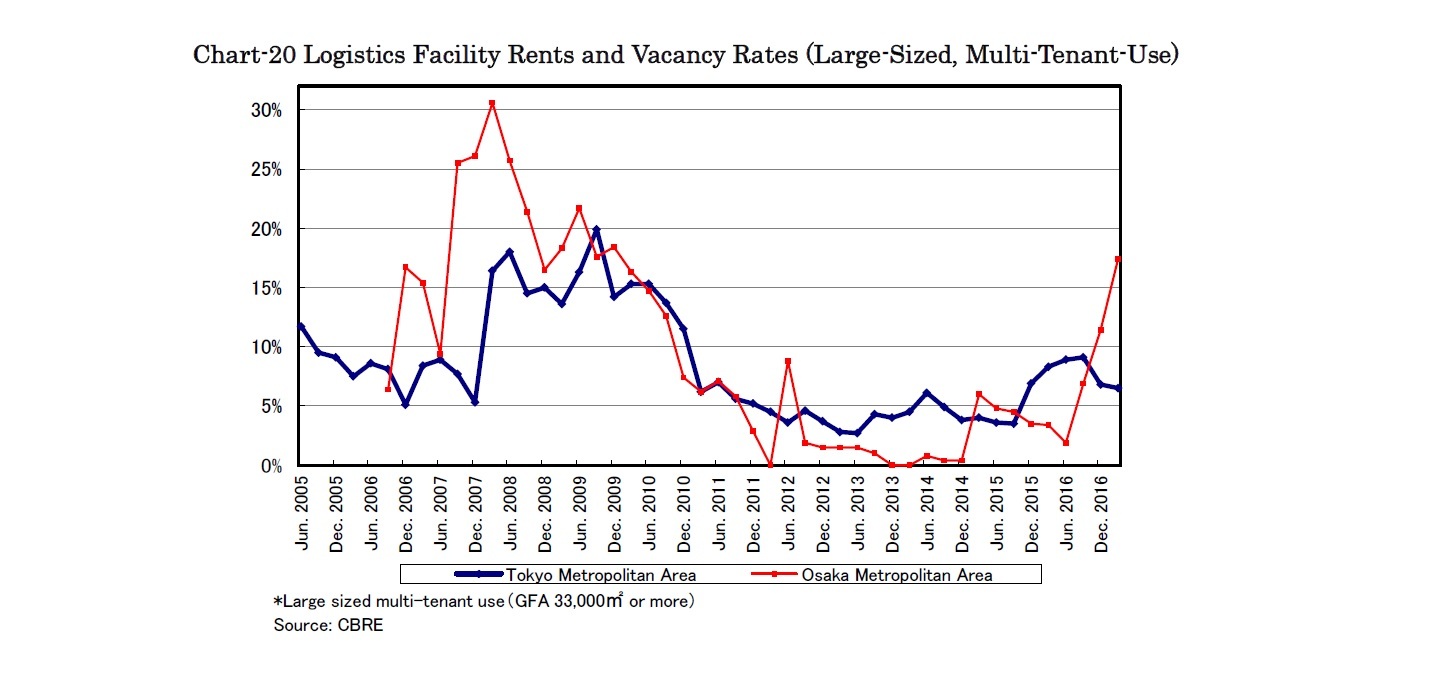

According to CBRE, large, multi-tenant logistics facilities in the Tokyo and Osaka metropolitan areas posted respective vacancy rates of 6.5% and 17.4% in the first quarter (Chart-20). Several large logistics facilities have been supplied in both Tokyo’s and Osaka’s metropolitan areas on the back of high expectations for e-commerce growth.

While a largest-ever 1.9 million square meters of space was newly supplied in the Tokyo metropolitan area, strong demand absorbed 1.76 million square meters and vacancy rates did not deteriorate much in 2016. While new supply volume will shrink somewhat in 2017, there is concern that more than 2.5 million square meters, a glut of new space, will be supplied in 2018.

On the other hand, in the Osaka metropolitan area 0.71 million square meters of space, which is too much for the area, was supplied and vacancy rates surged in 2016. Even worse, another 1.3 and 0.94 million square meters of space will be supplied in 2017 and 2018, respectively. Though high vacancy rates should be inevitable for years, inland areas close to consumers can expect relatively strong demand and high rents.

In addition, the recent fire accident at a large logistics facility will lead to additional costs charged to investors in preparation for fire prevention and recovery processes.

Eriko Kato

Research field

レポート紹介

-

研究領域

-

経済

-

金融・為替

-

資産運用・資産形成

-

年金

-

社会保障制度

-

保険

-

不動産

-

経営・ビジネス

-

暮らし

-

ジェロントロジー(高齢社会総合研究)

-

医療・介護・健康・ヘルスケア

-

政策提言

-

-

注目テーマ・キーワード

-

統計・指標・重要イベント

-

媒体

- アクセスランキング

Copyright © 2016 NLI Research Institute. All rights reserved.