- NLI Research Institute >

- Real estate >

- Japanese Property Market Quarterly Review, Fourth Quarter 2016-J-REITs Appreciate by 6% and Record Third Largest Yearly Acquisition Amount in 2016-

06/02/2017

Japanese Property Market Quarterly Review, Fourth Quarter 2016-J-REITs Appreciate by 6% and Record Third Largest Yearly Acquisition Amount in 2016-

Financial Research Department Economic Research Department Researcher Hiroto Iwasa

Font size

- S

- M

- L

4.J-REIT and Property Investment Markets

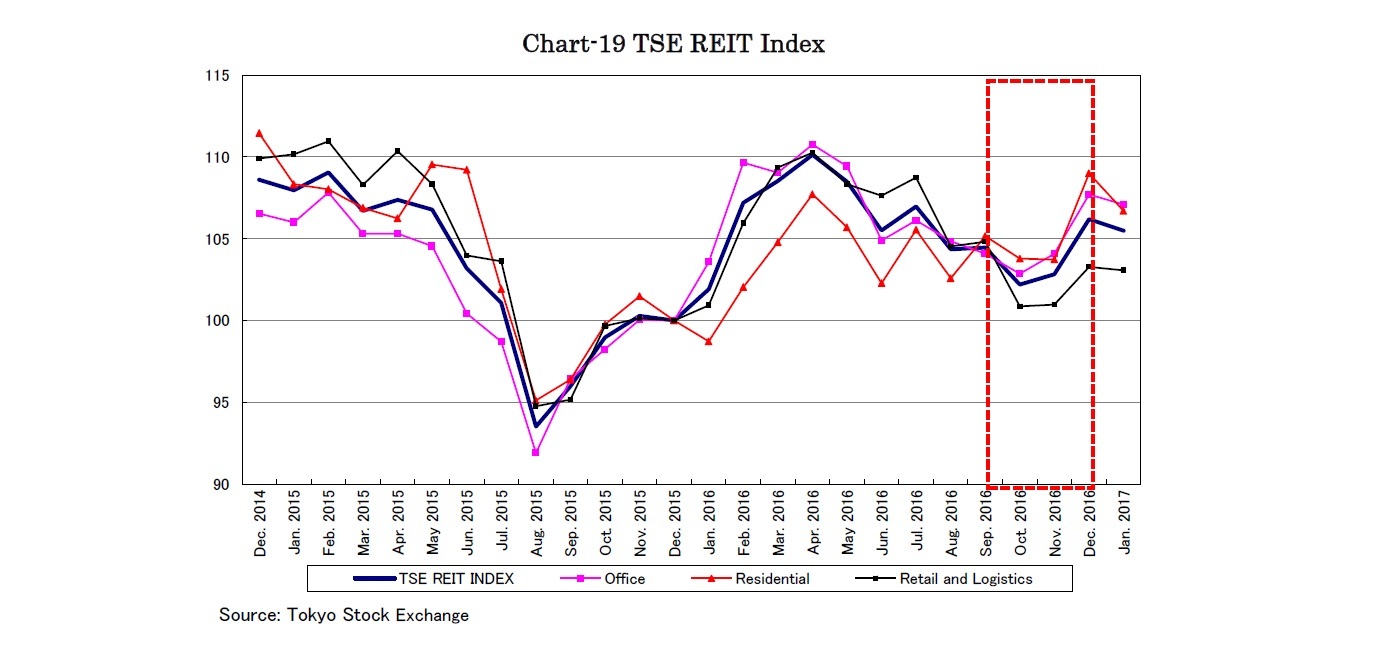

The TSE REIT Index rose by 1.7% q-o-q in the fourth quarter pulled up by the equity market rallying after the U.S. presidential election, despite having stagnated before the event. The office and residential sectors rose by 3.5% and 3.7% q-o-q respectively, while other sectors – including retail and logistics – declined by 5.1% (Chart-19). At the end of December, the J-REIT market value was 12.1 trillion JPY, while the price to NAV ratio was 1.2 times and the dividend yield was 3.5%, with a 3.5% yield spread on 0% of ten year JGBs.

The TSE REIT Index rose by 6.2% in 2016 after declining in 2015. Even affected by the significant events overseas such as the U.K. withdrawal from the EU and the U.S. presidential election, the financial results of J-REITs have steadily improved and supported the unit prices.

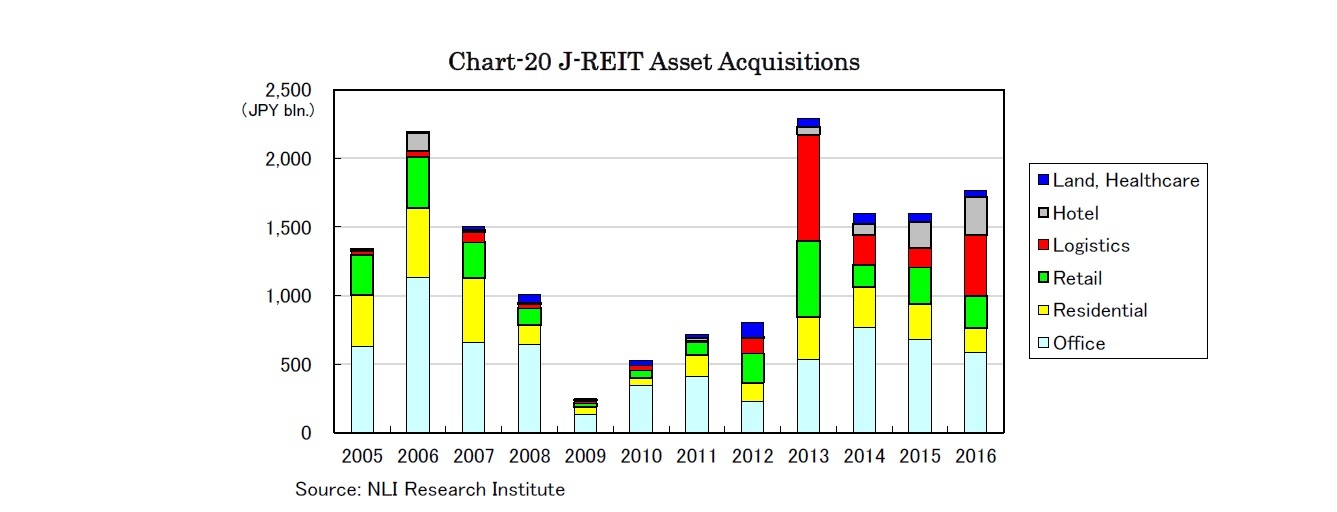

J-REITs acquired property assets amounting to 1.77 trillion JPY with seven IPOs in 2016 (Chart-20). The acquisition volume was 11% more than in 2015, posting the third largest yearly amount in history even when the entire market transaction volume shrank in Japan. J-REITs acquired an increasing number of logistics facilities and hotels noticeably, while the total acquisition volume of the traditional three sectors such as office, residential and retail decreased y-o-y, accounting for the lowest ever 56% of total volume. Besides that, acquisition volume in the five central wards of Tokyo accounted for only 23% of total volume, shrinking from 28% in 2015. Pursuing yield incremental acquisitions, J-REITs have shifted acquisition targets from central Tokyo to suburban areas and from core to sub categories.

The funding environment has been comfortable with the average J-REIT bond issuance condition being 10 years and 0.51%.

The TSE REIT Index rose by 6.2% in 2016 after declining in 2015. Even affected by the significant events overseas such as the U.K. withdrawal from the EU and the U.S. presidential election, the financial results of J-REITs have steadily improved and supported the unit prices.

J-REITs acquired property assets amounting to 1.77 trillion JPY with seven IPOs in 2016 (Chart-20). The acquisition volume was 11% more than in 2015, posting the third largest yearly amount in history even when the entire market transaction volume shrank in Japan. J-REITs acquired an increasing number of logistics facilities and hotels noticeably, while the total acquisition volume of the traditional three sectors such as office, residential and retail decreased y-o-y, accounting for the lowest ever 56% of total volume. Besides that, acquisition volume in the five central wards of Tokyo accounted for only 23% of total volume, shrinking from 28% in 2015. Pursuing yield incremental acquisitions, J-REITs have shifted acquisition targets from central Tokyo to suburban areas and from core to sub categories.

The funding environment has been comfortable with the average J-REIT bond issuance condition being 10 years and 0.51%.

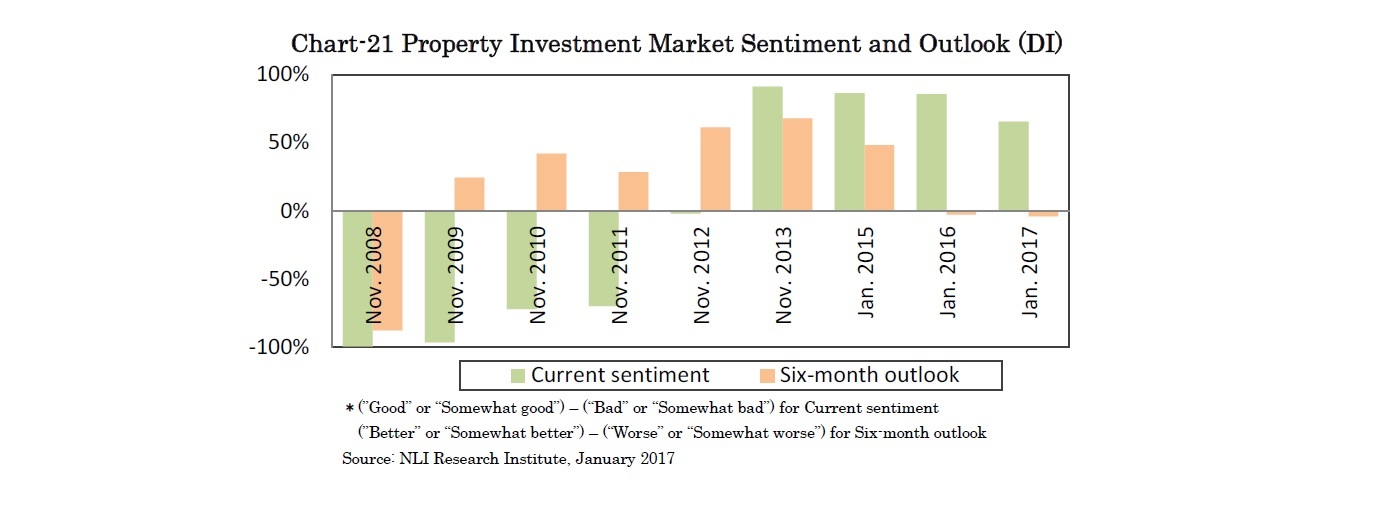

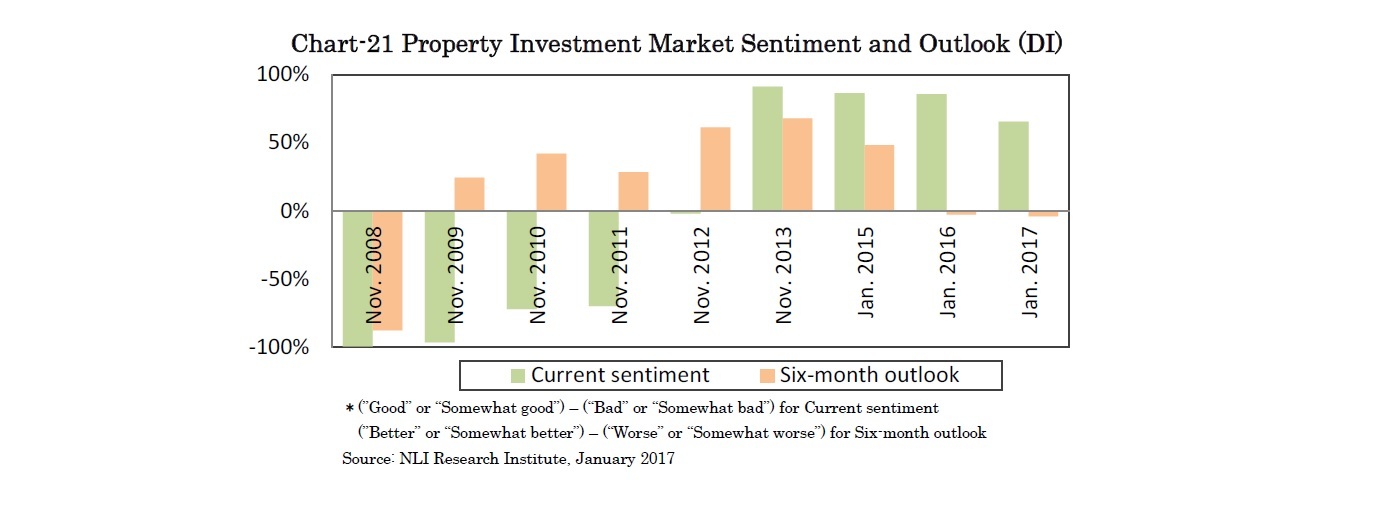

In the NLI Research Institute’s “thirteenth annual property investment market survey,”2 regarding the current sentiment, “Good” or “Somewhat good” responses overwhelmed “Bad” or “Somewhat bad” responses for the fourth consecutive year (Chart-21). However, regarding the six-month outlook, the market direction was unassertive with the small difference between the positives and negatives and “No change” responses accounting for two-thirds of responses.

Despite domestic economic conditions looking stable, with the uncertainty concerning policy measures by the new U.S. government and several elections scheduled throughout the EU, the market direction has become increasingly difficult to read.

Despite domestic economic conditions looking stable, with the uncertainty concerning policy measures by the new U.S. government and several elections scheduled throughout the EU, the market direction has become increasingly difficult to read.

2 Mamoru Masumiya “ Interest Rate Concerns Emerge, Property Prices Forecasted to Decline after Going Sideways~The Thirteenth Japanese Property Market Survey~ -” Real Estate Analysis Report, February 7, 2017

03-3512-1858

Copyright © 2016 NLI Research Institute. All rights reserved.