- NLI Research Institute >

- Real estate >

- Outlook Reverses, Divergence in Forecasts of Property Price Peak from 2015 to 2018~The Twelfth Japanese Property Market Survey~

Outlook Reverses, Divergence in Forecasts of Property Price Peak from 2015 to 2018~The Twelfth Japanese Property Market Survey~

mamoru masumiya

Font size

- S

- M

- L

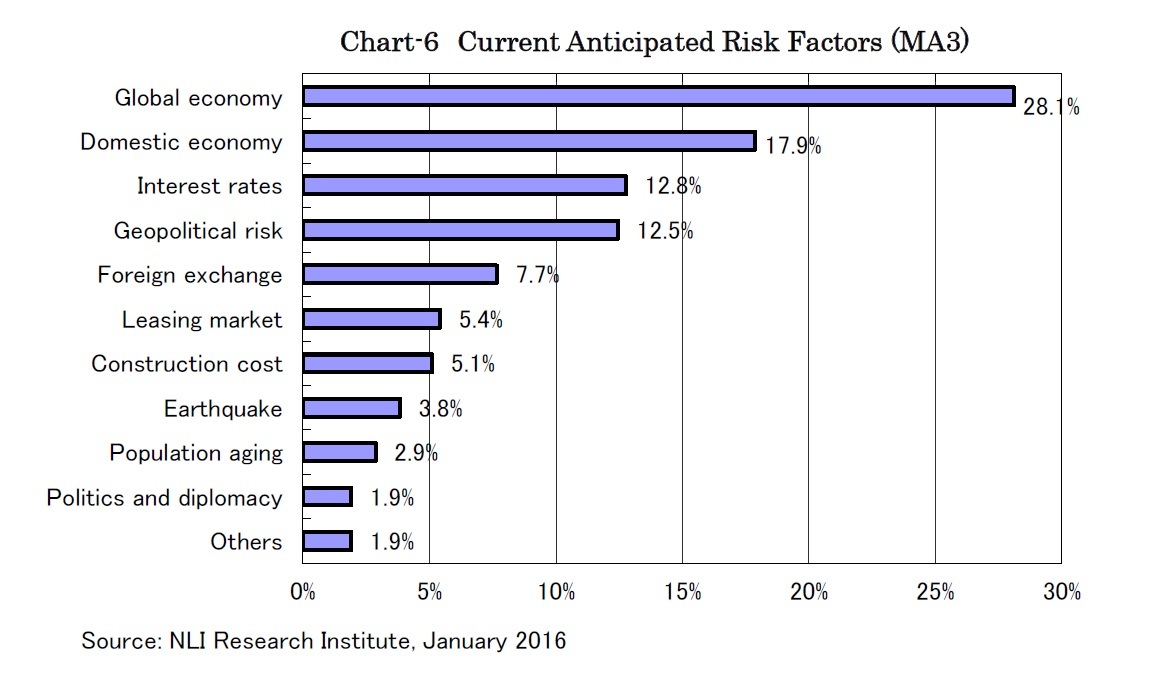

The next question was about which risk factors were the top three influential concerns for the property investment market.

Foreign factors basically have indirect effects on the domestic property market, however, more respondents chose “Global economy” than “Domestic economy,” and not a small number of respondents chose “Geopolitical risk” as well (Chart-6).

Economic growth in many emerging Asian countries has slowed down, affected by the stagnating Chinese demand. It is anticipated that office demand from global companies and shopping and hotel demand by inbound travelers will plateau. In addition, a negative effect is the concern over foreign capital entering the Japanese property investment market, which ballooned in 2014.

Terrorist attacks have expanded out of the Middle East into developed cities such as Paris and Asian cities such as Bangkok and Jakarta, suggesting even the Japanese property market can no longer ignore geopolitical risks.

On the other hand, “Domestic economy,” the most influential factor on the domestic property market, was chosen by only 17.9% of the respondents, as the current economic conditions are still sound. In the same way, only a limited number of respondents chose “Interest rates,” as the loosening monetary policy is expected to continue for the time being. The number of respondents who chose “Construction cost” was also limited with related prices recently leveling off after years of dramatic rise.

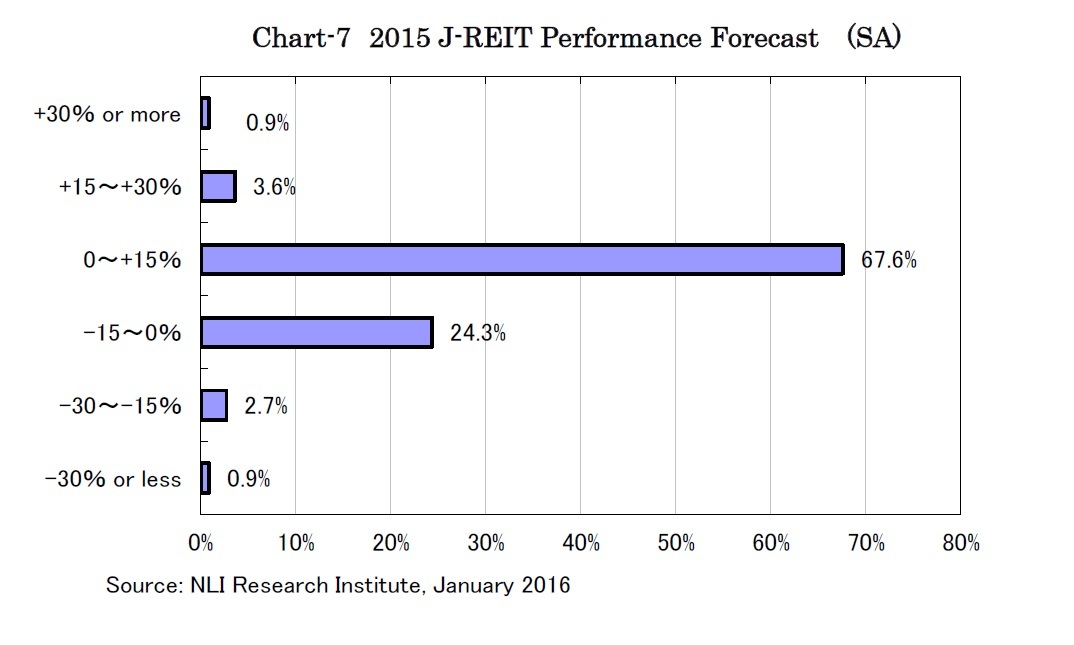

Regarding the J-REIT market forecast, 67.6% of respondents chose “0~+15%” of performance for TSE REIT index in 2016 (Chart-7). More than 90% of the respondents forecasted that the J-REIT prices will stay within a range of ±15% at the end of 2016.

J-REITs have shown relative resilience during the violent equity market correction at the beginning of this year, partly because J-REITs under-performed in 2015 and quite a few investors apparently prefer the stable dividends of J-REITs. On the other hand, it is difficult to imagine J-REIT prices to go beyond the level where dividend yields shrink to 3% as was seen at the beginning of 2015.

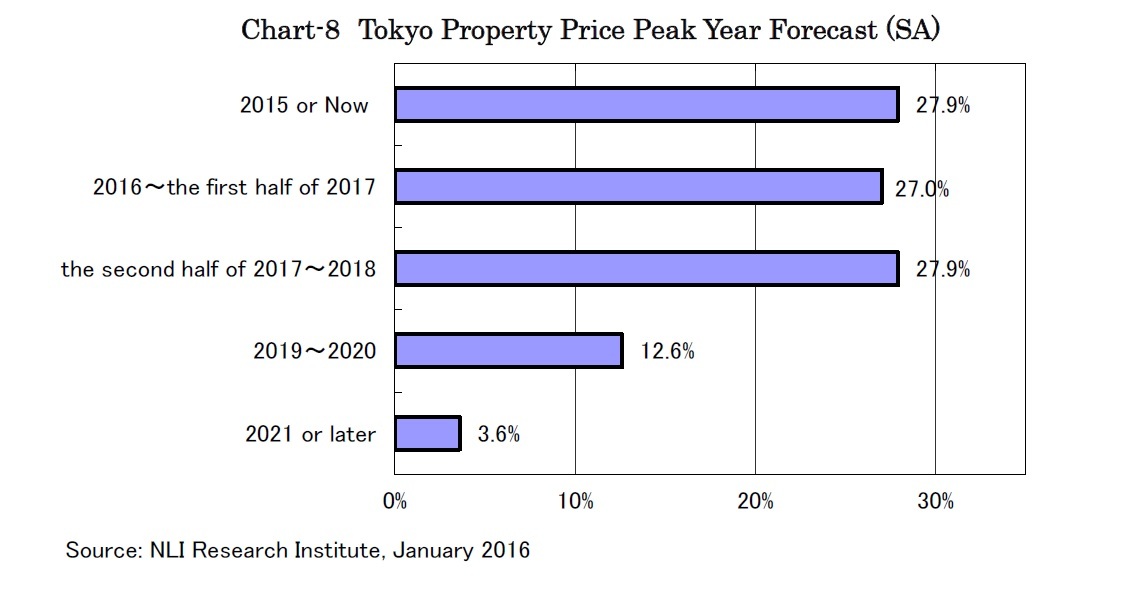

Finally, when asked about the peak year forecast for property prices in Tokyo, responses were divided into the three periods of “2015 or now” with 27.9%, “the second half of 2017~2018” with 27.9% and “2016~the first half of 2017” with 27.0% (Chart-8).

Considering the recent risk aversion in financial markets and high transaction prices in the physical property market, quite a few respondents think the property prices have already peaked out.

On the other hand, more than half of respondents still think the investment market has been in a positive mood. However, half of them forecast the price appreciation to continue to no later than the first half of 2017, considering the US interest-rate increases and the domestic consumption tax-rate hike in 2017. The other half think the domestic loosening monetary policy continues for years and that property prices can benefit from the conditions.

Despite the 2020 Tokyo Olympic Games definitely being a positive for the property market, only a limited number of respondents forecasted property prices to continue to appreciate until the Olympic event.

The responses “2021 or later” were even less, suggesting few respondents expect the Olympic event to make Tokyo more competitive as an international city or future inflation to support property prices for the long term.

mamoru masumiya

Research field

Related Reports

- Japanese Property Market Quarterly Review, Third Quarter 2015-Markets Steady but Some Weaknesses Creeping In-

- Japanese Property Market Quarterly Review,Second Quarter 2015-Housing Starts Recover, Foreign Visitors Boost Hotel and Retail-

- Utmost Optimistic Sentiment Still Rising, but Property Prices to Peak Out by 2017-The Eleventh Japanese Property Market Survey-

Copyright © 2016 NLI Research Institute. All rights reserved.