- NLI Research Institute >

- Economics >

- Japan’s Economic Outlook for the Fiscal Years 2022 to 2024 (February 2023)

15/02/2023

Japan’s Economic Outlook for the Fiscal Years 2022 to 2024 (February 2023)

Economic Research Department Executive Research Fellow Taro Saito

Font size

- S

- M

- L

■Summary

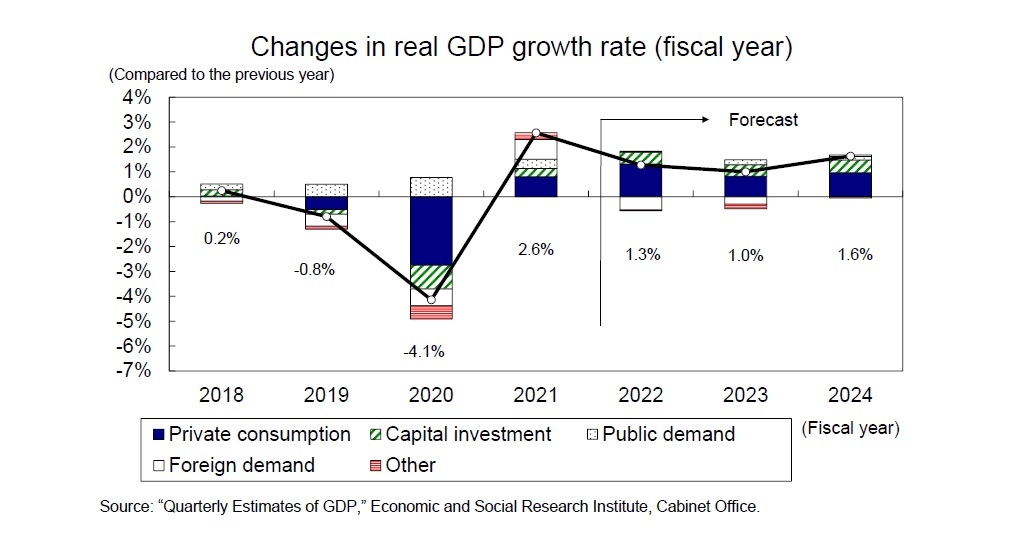

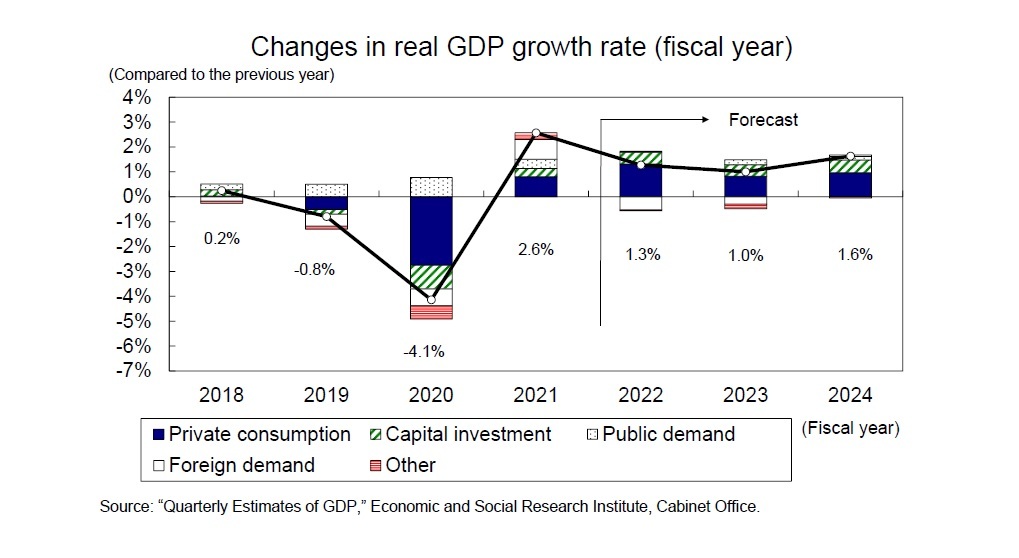

<Real GDP growth: 1.3% in FY 2022, 1.0% in FY 2023, 1.6% in FY 2024>

- Real GDP grew at an annual rate of 0.6% from the previous quarter in the October–December quarter of 2022, which marked the first positive growth in two quarters yet was not sufficient to bring about a full recovery from the decline in the July–September quarter (down 1.0% from the previous quarter).

- In the January–March quarter of 2023, Japan’s economy is expected to grow at a low rate of around 0% per annum as exports start to decline against the backdrop of a slowdown in overseas economies. The main scenario for Japan is that a recession will be avoided because negative growth in the United States and the euro area will be only modest while the Chinese economy is continuing to recover from the lifting of its zero-COVID-19 policy, all of which indicate that economic recovery is fragile and downside risks remain.

- Real GDP is expected to grow 1.3% in FY 2022, 1.0% in FY 2023, and 1.6% in FY 2024. Exports are not expected to be a driver of the economy, but private consumption and capital investment will increase on the back of high household savings and corporate earnings, and thus domestic demand-led growth will continue.

- Consumer price inflation (excluding fresh food) will decline from the current 4% level to around 3% in February 2023 due to the government's measures to combat inflation, but energy prices will rise again after April when electricity rates are scheduled to rise. Moreover, the pause in high oil prices and the weak yen will weaken the movement to pass on raw material costs, while the pace of increase in service prices will gradually rise due to higher wage rates. Consumer price inflation (excluding fresh food) is forecast to be 3.0% in FY 2022, 2.3% in FY 2023, and 1.1% in FY 2024.

■目次

1. Positive growth of 0.6% per annum from the previous quarter in the October–December quarter of 2022

・Indexes of Business Conditions' underlying assessment is revised downward

・Household savings rate approaches pre-COVID-19 crisis level

・The spring wage increase rate will reach a 26-year high

2. Real GDP growth rate expected to be 1.3% in FY 2022, 1.0% in FY 2023, and 1.6% in FY 2024

・Inflation will be a factor in declining savings

・Real GDP will surpass its most recent peak in the fiscal year 2024

・Current account balance outlook

・Price outlook

1. Positive growth of 0.6% per annum from the previous quarter in the October–December quarter of 2022

・Indexes of Business Conditions' underlying assessment is revised downward

・Household savings rate approaches pre-COVID-19 crisis level

・The spring wage increase rate will reach a 26-year high

2. Real GDP growth rate expected to be 1.3% in FY 2022, 1.0% in FY 2023, and 1.6% in FY 2024

・Inflation will be a factor in declining savings

・Real GDP will surpass its most recent peak in the fiscal year 2024

・Current account balance outlook

・Price outlook

03-3512-1836

レポート紹介

-

研究領域

-

経済

-

金融・為替

-

資産運用・資産形成

-

年金

-

社会保障制度

-

保険

-

不動産

-

経営・ビジネス

-

暮らし

-

ジェロントロジー(高齢社会総合研究)

-

医療・介護・健康・ヘルスケア

-

政策提言

-

-

注目テーマ・キーワード

-

統計・指標・重要イベント

-

媒体

- アクセスランキング

Copyright © 2016 NLI Research Institute. All rights reserved.