- NLI Research Institute >

- Economics >

- Japan's Economic Outlook for Fiscal 2021 to 2023

16/11/2021

Japan's Economic Outlook for Fiscal 2021 to 2023

Economic Research Department Executive Research Fellow Taro Saito

Font size

- S

- M

- L

■Summary

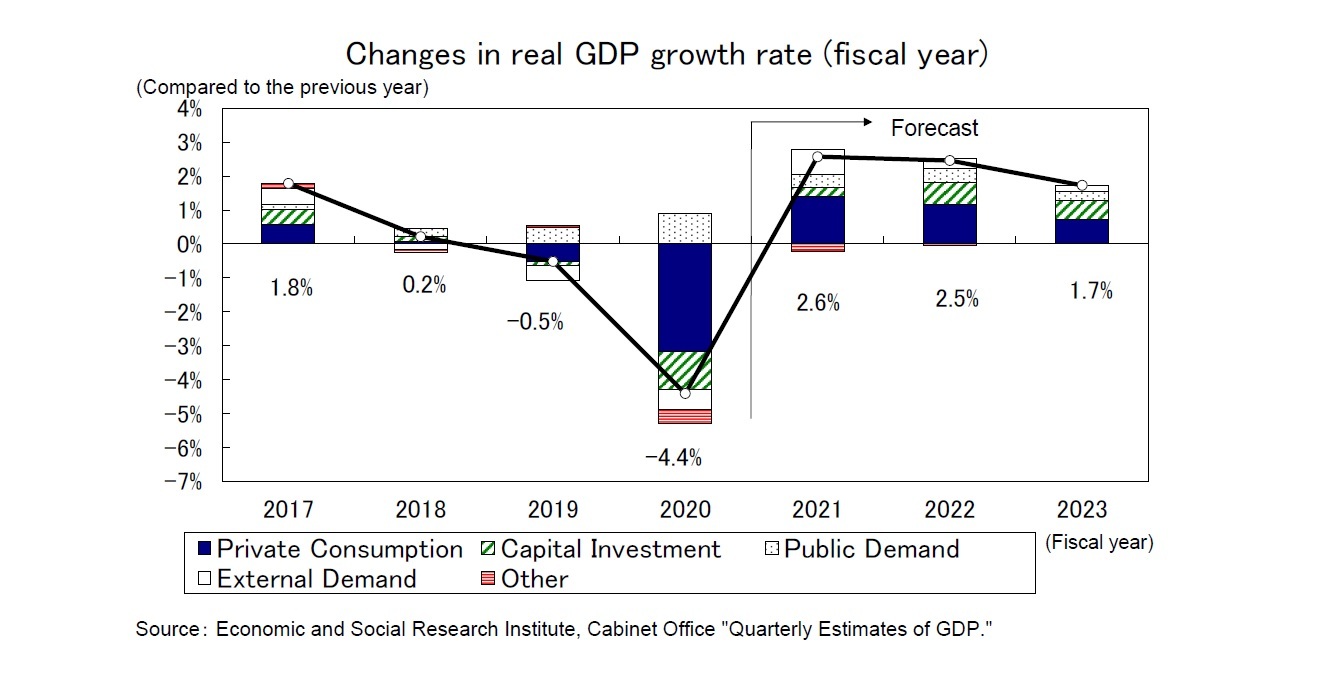

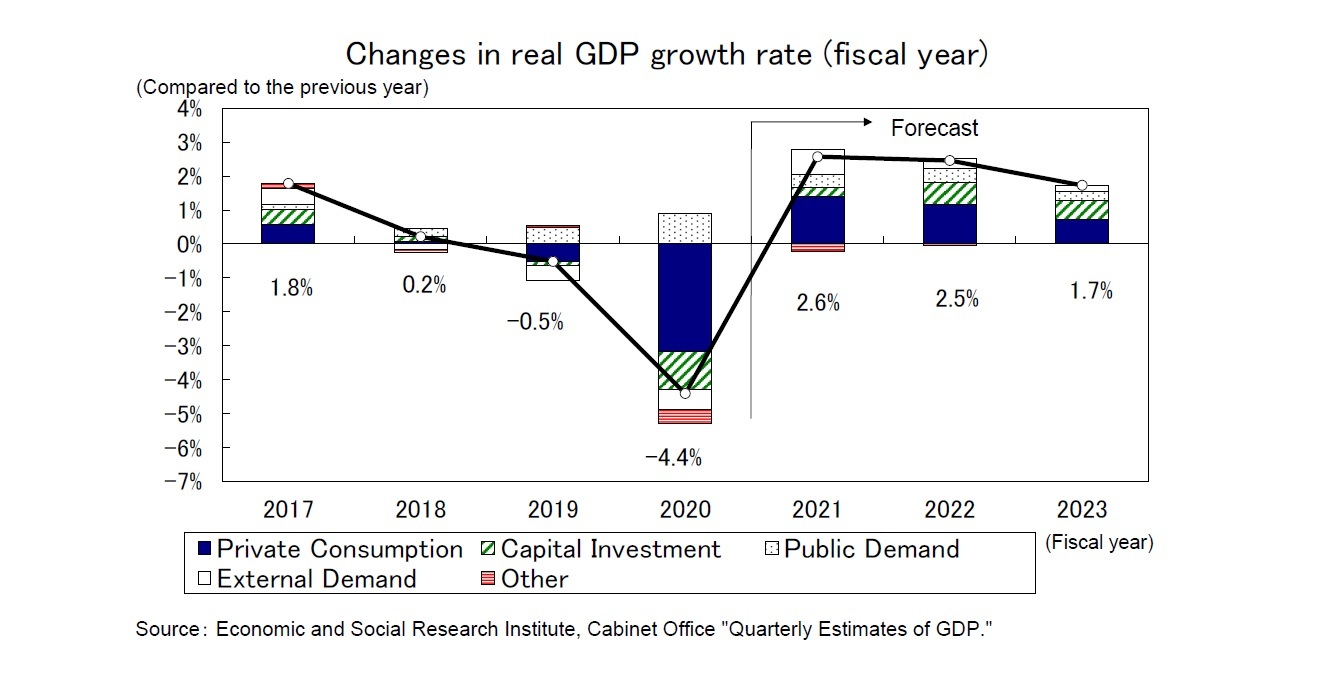

<Real GDP growth rate: 2.6% in FY 2021, 2.5% in FY 2022, 1.7% in FY 2023>

- In the July–September quarter of 2021, real GDP posted an annualized contraction of 3.0%, the first negative growth in two quarters, as private consumption, housing investment, and capital investment all declined sharply due to the state of emergency and supply constraints.

- In the October–December quarter of 2021, real GDP is forecast to post annual growth of 7.3%, mainly due to strong growth in private consumption following the lifting of the state of emergency. However, there are many risk factors, including prolonged supply constraints such as a shortage of semiconductors, deteriorating corporate profits due to worsening terms of trade, a decline in the real purchasing power of households, and tighter activity restrictions due to the spread of the coronavirus.

- The real GDP growth rate is expected to be 2.6% in FY 2021, 2.5% in FY 2022 and 1.7% in FY 2023. Although the state of emergency has been lifted, the pace of recovery in consumption will be slow after the rapid decline in the coronavirus crisis, partly because of continued fears about infectious diseases.

- Real GDP is expected to surpass its pre-coronavirus level (October–December quarter of 2019) in the April–June quarter of 2022 and return to its most recent peak before the consumption tax rate hike ( July–September quarter of 2019) in the April–June quarter of 2023.

■Index

1. In the July–September period of 2021, real GDP decreased by an annualized rate of

3.0% from the previous period

・Increasing outflow of income overseas due to deterioration in terms of trade

2. Real GDP growth rate is expected to be 2.6% in FY 2021, 2.5% in FY 2022 and 1.7%

in FY 2023

・Service consumption will pick up after the state of emergency's cancellation

・High levels of savings, cash and deposits can significantly boost consumption

・Real GDP will surpass its most recent peak in FY 2023

・Price Outlook

1. In the July–September period of 2021, real GDP decreased by an annualized rate of

3.0% from the previous period

・Increasing outflow of income overseas due to deterioration in terms of trade

2. Real GDP growth rate is expected to be 2.6% in FY 2021, 2.5% in FY 2022 and 1.7%

in FY 2023

・Service consumption will pick up after the state of emergency's cancellation

・High levels of savings, cash and deposits can significantly boost consumption

・Real GDP will surpass its most recent peak in FY 2023

・Price Outlook

03-3512-1836

レポート紹介

-

研究領域

-

経済

-

金融・為替

-

資産運用・資産形成

-

年金

-

社会保障制度

-

保険

-

不動産

-

経営・ビジネス

-

暮らし

-

ジェロントロジー(高齢社会総合研究)

-

医療・介護・健康・ヘルスケア

-

政策提言

-

-

注目テーマ・キーワード

-

統計・指標・重要イベント

-

媒体

- アクセスランキング

Copyright © 2016 NLI Research Institute. All rights reserved.