- NLI Research Institute >

- Do First Movers Have an Edge in the E-Money Market?

Do First Movers Have an Edge in the E-Money Market?

Social Improvement and Life Design Research Department Senior researcher Naoko Kuga

Font size

- S

- M

- L

The sight of people sweeping smart card train passes at turnstiles and mobile phones at cash registers have become commonplace as electronic money grows increasingly widespread.

According to the Communications Usage Trend Survey 2009 (Ministry of Internal Affairs and Communications), the ownership rate of contactless e-money has reached 29.6% in Japan. This represents an approximately three-fold increase since fiscal 2006 when e-money was first added to the survey. In addition, with electronic settlements growing at a record pace for four consecutive months since December 2009 (Nikkei Shimbun, April 22, 2010), the e-money ownership rate is predicted to continue increasing.

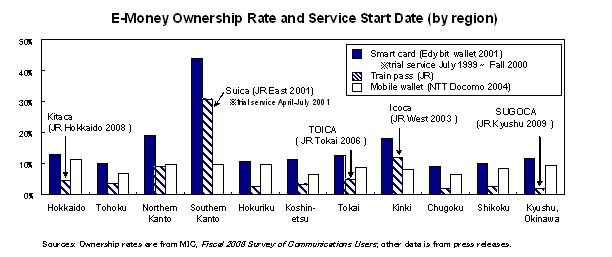

The survey divides e-money into three categories: smart card, smart card with train pass, and mobile wallet. In the southern Kanto and Kinki markets, the ownership rate is highest for the smart card, followed by the train pass and mobile wallet. Service start dates reflect the same order.

In other markets, while the smart card ranks in first place, followed by the mobile wallet in second place and train pass in third place, with service start dates also reflecting this order. Thus the mobile wallet’s early-mover status may have given it an edge over the train pass. Moreover, the mobile wallet ownership rate is only slightly higher in Hokkaido than in southern Kanto, and tends to be roughly the same nationwide. This suggests that the mobile wallet could struggle to make inroads in markets where the train pass was an early mover.

Although we need to understand the services in more detail to fully grasp the competitive situation, a simple glance at the respective e-money media suggests that starting with the smart card, early movers have acquired larger market shares.

However, looking ahead, the market structure could change drastically due to cross-media collaborations and the common e-money infrastructure now under study by the Ministry of Economy, Trade and Industry. Thus first movers may not be able to hold onto their early gains unless they continue to offer more convenient and attractive services.

03-3512-1878

レポート紹介

-

研究領域

-

経済

-

金融・為替

-

資産運用・資産形成

-

年金

-

社会保障制度

-

保険

-

不動産

-

経営・ビジネス

-

暮らし

-

ジェロントロジー(高齢社会総合研究)

-

医療・介護・健康・ヘルスケア

-

政策提言

-

-

注目テーマ・キーワード

-

統計・指標・重要イベント

-

媒体

- アクセスランキング

Copyright © 2016 NLI Research Institute. All rights reserved.