1.Positive Growth of 1.0% on an Annualized Basis in the April–June Quarter of 2025

Real gross domestic product (GDP) in the April–June quarter of 2025 grew by 0.3% from the previous quarter (1.0% on an annualized basis), marking the fifth consecutive quarter of positive growth. While domestic demand decreased by 0.1% from the previous quarter, exports increased by 2.0% despite the Trump tariffs, and external demand contributed 0.3% on a quarter-to-quarter basis, offsetting the sluggishness in domestic demand. Supported by strong corporate earnings, capital investment significantly increased by 1.3% from the previous quarter, while private consumption also continued to increase by 0.2%. However, private demand as a whole remained flat at 0.0% from the previous quarter, due to a substantial negative contribution of -0.3% from the change in private inventories. Public demand declined for the third consecutive quarter, with government consumption flat at 0.0% and public investment falling by 0.5%, resulting in a 0.3% decrease from the previous quarter.

At the time of the First Preliminary Quarterly Estimates of GDP for the April–June quarter of 2025, past growth rates were revised due to updates in basic statistics and re-estimations of seasonal adjustments. The real GDP growth rate in the January–March quarter of 2025 was revised upward from negative growth of -0.2% on an annualized basis to positive growth of 0.6%, mainly due to an upward revision in private consumption. Consequently, real GDP recorded five consecutive quarters of positive growth since the April–June quarter of 2024.

(US-Bound Export Volumes Remain Flat Even After Tariff Hikes)

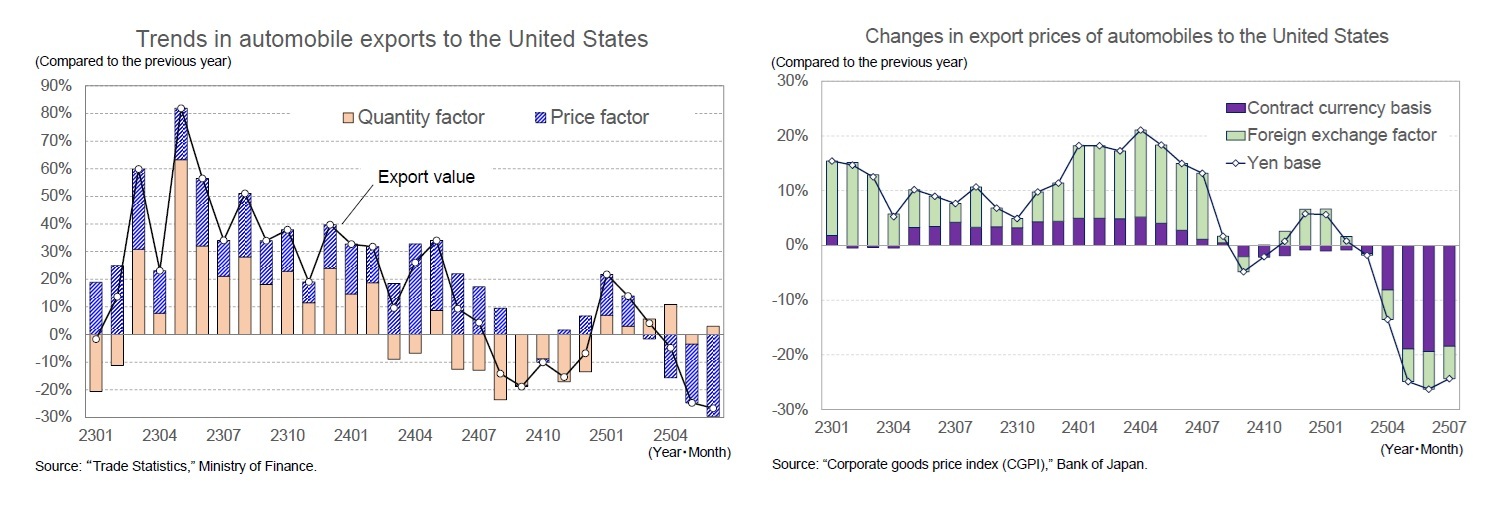

The economic impact of US tariff hikes has gradually become evident but remains limited to date. According to the trade statistics published by the Ministry of Finance (seasonally adjusted by NLI Research Institute), the export volume index to the US in the April–June quarter of 2025 was up 0.4% from the previous quarter. Even under the Trump tariffs, US-bound exports in terms of volume have remained within a flat range.

In terms of value, exports of automobiles to the US—which have been subject to an additional 25% tariff since April—declined by 4.8% compared to the previous April, marking the first decrease in four months, before subsequently sharply declining by over 20% in both May and June. While export volumes remained broadly flat, a sharp decline in export prices led to a substantial fall in export values.

Although the export price index in the trade statistics is yen-based and therefore reflects foreign exchange fluctuations, the Bank of Japan’s corporate goods price index (CGPI) provides export price indices in both contract-currency and yen terms. Looking at the contract-currency-based index for automobile exports to the US, the decline sharply accelerated from -1.5% compared to the previous year in March to -8.1% in April, remaining at nearly -20% since May.

On the other hand, estimates of US-bound export price indices for products other than automobiles—based on the trade statistics and the CGPI—indicate that while prices have fallen in yen terms due to yen appreciation, they have remained almost flat in contract-currency terms compared to the previous year. The impact of tariff hikes on exports can be attributed to the decline in volumes due to reduced price competitiveness, and exporters reducing prices to mitigate the drop in volumes. In the case of automobiles, exporters have managed to prevent a significant decline in export volumes by making substantial price cuts. Since many automobiles exported to the US are sold by Japanese subsidiaries in the US, it is inferred that Japanese parent companies are absorbing the tariff costs to maintain market share.

For exports other than automobiles, exporters have not reduced contract-currency prices, and export volumes have remained broadly flat. This suggests that the full pass-through of tariff costs to prices in the US has not yet materialized, meaning that the relative price increase of Japanese exports compared to domestically produced goods in the US has not yet become evident.

(Impact of Tariff Hikes Expected to Materialize Going Forward)

However, looking ahead, tariff costs are expected to be gradually passed on to prices in the US, making it difficult for Japanese exporters to avoid a decline in price competitiveness. In the case of automobiles, although large price cuts have helped mitigate declines in export volumes, this has worsened domestic corporate earnings. In fact, according to the June 2025 Tankan Survey by the Bank of Japan, operating profit plans for the automobile sector in FY 2025 were sharply revised downward by -24.9% compared to the previous survey in March, resulting in a projected decline of -23.4% compared to the previous year. This was due not only to a modest downward revision in export growth but also a substantial deterioration of -3.05 percentage points in the ordinary profit-to-sales ratio, with price cuts on exports being the main factor behind the declining profitability.

Maintaining market share through price reductions accompanied by a sharp deterioration in profits has its limits, and major Japanese automakers have begun to increase sales prices in the US. In the future, US-bound exports are expected to inevitably decline in volume, mainly due to Japan’s loss of price competitiveness.

Although the tariff rate on automobiles was reduced from 27.5% to 15%, this still represents a significant increase compared to the original 2.5%, and the timing of implementation has not been determined. Moreover, reciprocal tariffs have been raised from 10% to 15%, leaving the average tariff rate on US-bound exports largely unchanged. The main assumptions regarding US tariff policy against Japan in this economic outlook are as follows: (i) reciprocal tariffs will remain at 15%; (ii) tariffs on steel, aluminum, and copper will remain at 50%; (iii) the automobile tariff will be reduced from 27.5% to 15% by the end of September 2025; and (iv) tariffs of 15% on semiconductors (including exempted items, average) and 25% on pharmaceuticals will be implemented by the end of September 2025.

While Japanese exports have remained broadly flat, they are expected to decline in the July–September quarter of 2025, particularly to the US, as the impact of tariff hikes becomes more pronounced. This outlook assumes that no further tariff hikes will occur beyond those already in place, except for certain items such as semiconductors and pharmaceuticals. The decline in exports due to tariff hikes is expected to be contained by the end of FY 2025. However, with the slowdown of overseas economies—particularly in the US and China—and the contraction of global trade transactions, downward pressure on Japan’s exports is likely to remain strong for the time being.

In addition, this outlook assumes that—reflecting US interest rate cuts and Bank of Japan rate hikes—the yen will appreciate against the US dollar to the mid-¥130 level by the end of FY 2026, which will also serve as a downward factor for exports. Exports of goods and services in the GDP statistics are expected to slow from an increase of 1.7% compared to the previous year in FY 2024 to 0.9% in FY 2025, remaining subdued at 1.2% in FY 2026.

(Spring 2026 Wage Negotiations Expected to Show a Slower Pace of Wage Increases)

According to the Survey on Wage Demands and Settlements of Major Private Companies in Spring released by the Ministry of Health, Labour and Welfare on August 1, the wage increase rate in 2025 was 5.52%, surpassing 5.33% in 2024—which was the highest level in 33 years—by 0.19 percentage points. In addition, according to the Final Aggregated Results of 2025 Spring Wage Negotiations published by RENGO, the average wage increase rate in 2025 was 5.25% (5.10% in 2024), and the wage increase portion equivalent to a base wage increase was 3.70% (3.56% in 2024).

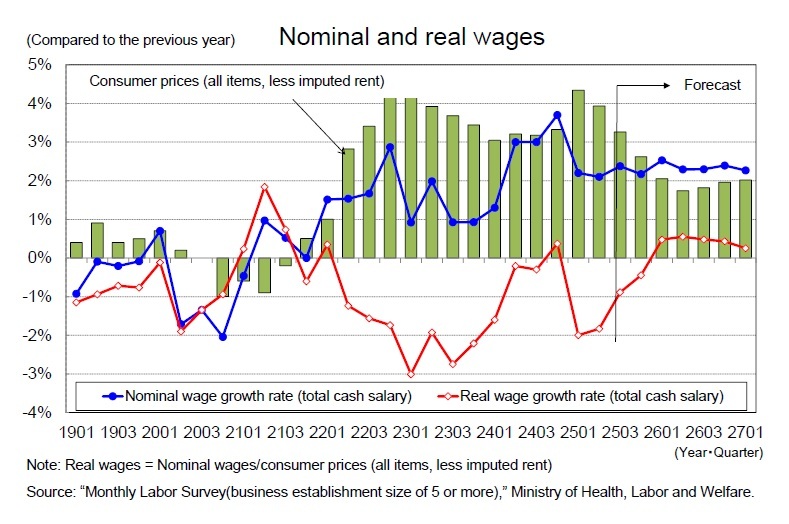

Real wages adjusted for consumer prices turned positive compared to the previous year in June, July, November, and December 2024, mainly due to a sharp increase in special cash earnings, although they remained negative in all other months.Regularly paid wages (scheduled cash earnings plus non-scheduled cash earnings) ,which is more stable than total cash earnings, have remained negative since February 2022 for more than three years.

The decline in real wages reflects not only persistently high consumer price inflation but also the fact that nominal wage growth has remained sluggish despite two consecutive years of wage increases above 5%. Total cash earnings per employee increased by 3.7% compared to the previous year in the October–December quarter of 2024, mainly due to a sharp rise in year-end bonuses, although growth slowed to the low 2% range after entering 2025.

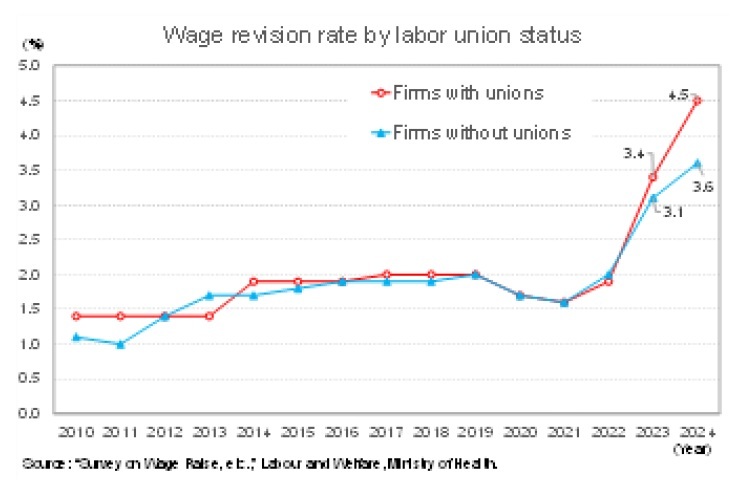

For regular workers, scheduled cash earnings are closely linked to the base wage increase, excluding regular seniority-based raises. However, in FY 2024, scheduled cash earnings for regular workers rose only 2.5% compared to the previous year, considerably below the 4.02% base wage increase reported by the Central Labour Relations Commission’s Comprehensive Survey on Wage Conditions. One factor is that wage increase rates based on labor union negotiations no longer fully reflect overall labor market trends due to the declining unionization rate. Indeed, according to the Ministry of Health, Labour and Welfare’s Survey on the Actual Situation of Wage Increases, the average wage revision rate in 2024 was 4.5% for firms with unions versus only 3.6% for those without, significantly widening the gap.

Furthermore, the rising share of part-time workers—who have relatively low wage levels—has been a factor in depressing average wages. In addition, the Monthly Labour Survey suffers from statistical breaks every January due to sample replacement, contributing to wage growth rates being lower than high spring wage increase rates suggest. The difference between old and new samples for total cash earnings (pre-replacement minus post-replacement) was +0.6% in January 2022, +0.2% in January 2023, -0.2% in January 2024, and -0.9% in January 2025. Consequently, the wage growth rate in the survey was overstated in 2022 and 2023, and understated in 2024 and 2025.

Although the wage increase rate in the spring negotiations remained at a high 5% range for two consecutive years, the outlook suggests a worsening environment for wage negotiations due to the economic slowdown caused by the Trump tariffs. While structural demographic factors such as population decline and aging are likely to sustain a sense of labor shortage among firms, declining corporate earnings due to reduced exports and falling inflation rates are expected to limit wage increases.

The wage increase rate in the 2026 spring negotiations is projected at 4.5% (based on the Ministry of Health, Labour and Welfare’s survey), inevitably lower than the previous year. However, a wage increase rate in the mid-4% range translates to about 3% in terms of base wage increases excluding seniority raises, still exceeding the Bank of Japan’s 2% price stability target. Real wages—which have been declining by around -2% compared to the previous year since early 2025—are expected to see the pace of decline narrow mainly due to a slowdown in consumer price inflation. Sustained and stable positive growth in real wages is projected from the January–March quarter of 2026 onward, when nominal wage growth is expected to remain in the 2% range while consumer price inflation falls below 2%.

レポートについてお問い合わせ

(取材・講演依頼)

{kind=link}

{kind=link}

{kind=link}