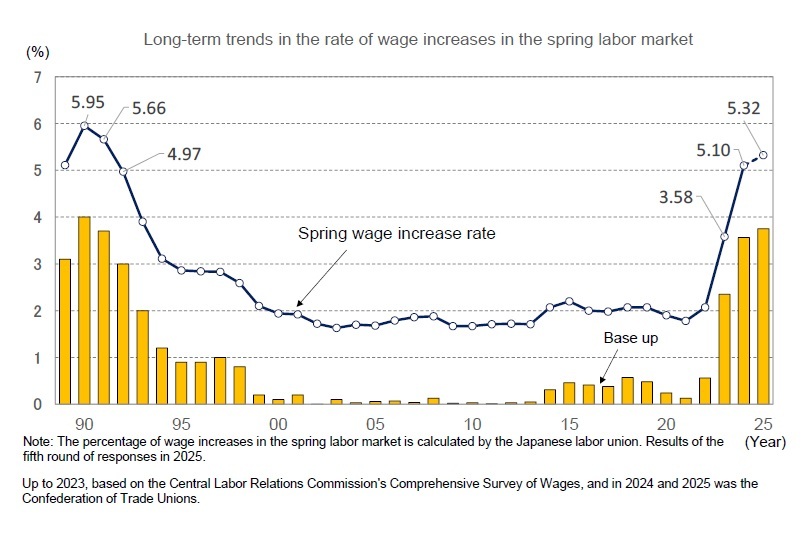

The average increase was 4.93% among small and medium-sized enterprises (fewer than 300 union members), reflecting a 0.48 percentage point rise from the previous year. While this is below the 5.36% increase seen among large enterprises (300 or more union members, up 0.17 percentage points from the previous year), the gap has narrowed compared to 2024.

Rengo’s basic policy for the 2025 negotiations called for wage hikes of over 5%, including regular pay raises, and urged smaller unions to actively demand corrections to wage disparities. The current settlement outcomes align with this policy.

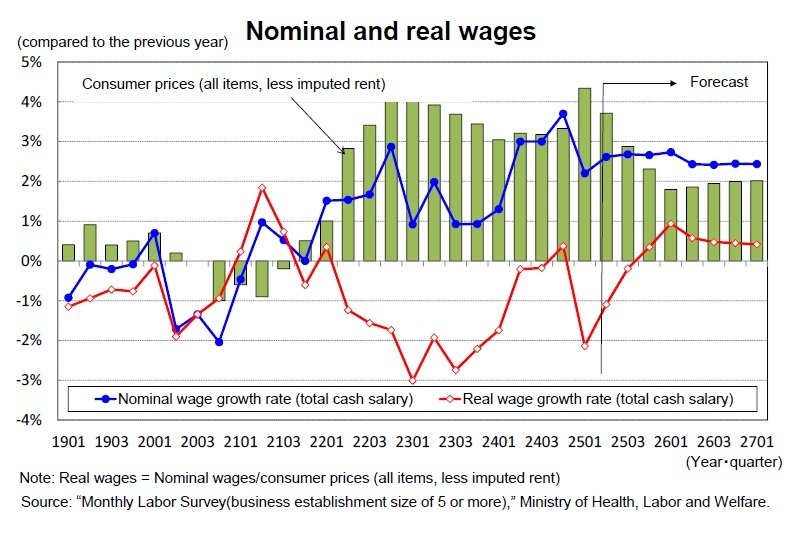

Total cash earnings per employee posted a strong 3.7% increase in the October–December quarter of 2024, mainly due to a significant rise in winter bonuses. However, the growth rate slowed to 2.2% with limited bonus payments in the January–March quarter of 2025.

Real wages—adjusted for consumer prices—showed positive growth compared to the previous year in June, July, November, and December 2024, largely due to increases in special cash earnings. However, they remained negative in other months.

Regular cash earnings (scheduled + non-scheduled earnings)—which are more stable than total cash earnings—have been in negative territory for over three years since February 2022.

Two consecutive years of 5% wage hikes can be attributed to substantial improvements in labor demand-supply conditions, corporate earnings, and prices. However, going forward, wage hike momentum is expected to weaken due to the economic slowdown caused by Trump’s tariffs.

Although structural-demographic factors such as a declining population and aging society will continue to create a labor shortage, deteriorating corporate profits due to declining exports and slowing inflation are likely to suppress wage increases.

The spring wage hike rate for 2026 is projected to be 4.2%. According to the Ministry of Health, Labour and Welfare’s Spring Wage Negotiation Status of Major Private Companies, the wage hike rate was 5.33% in 2024, the highest in 33 years, and is expected to remain in the 5% range in 2025 (NLI Research Institute forecast: 5.20%). Although a significant decline in 2026 seems inevitable, a wage hike rate in the low 4% range would still translate to a base wage increase (excluding regular raises) in the high 2% range, remaining above the Bank of Japan’s 2% inflation target.

{kind=link}

{kind=link}

{kind=link}

{kind=link}