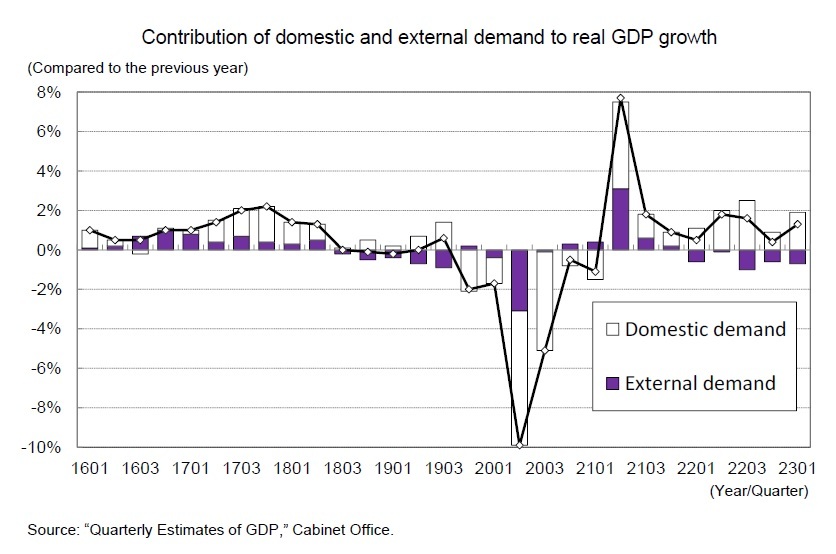

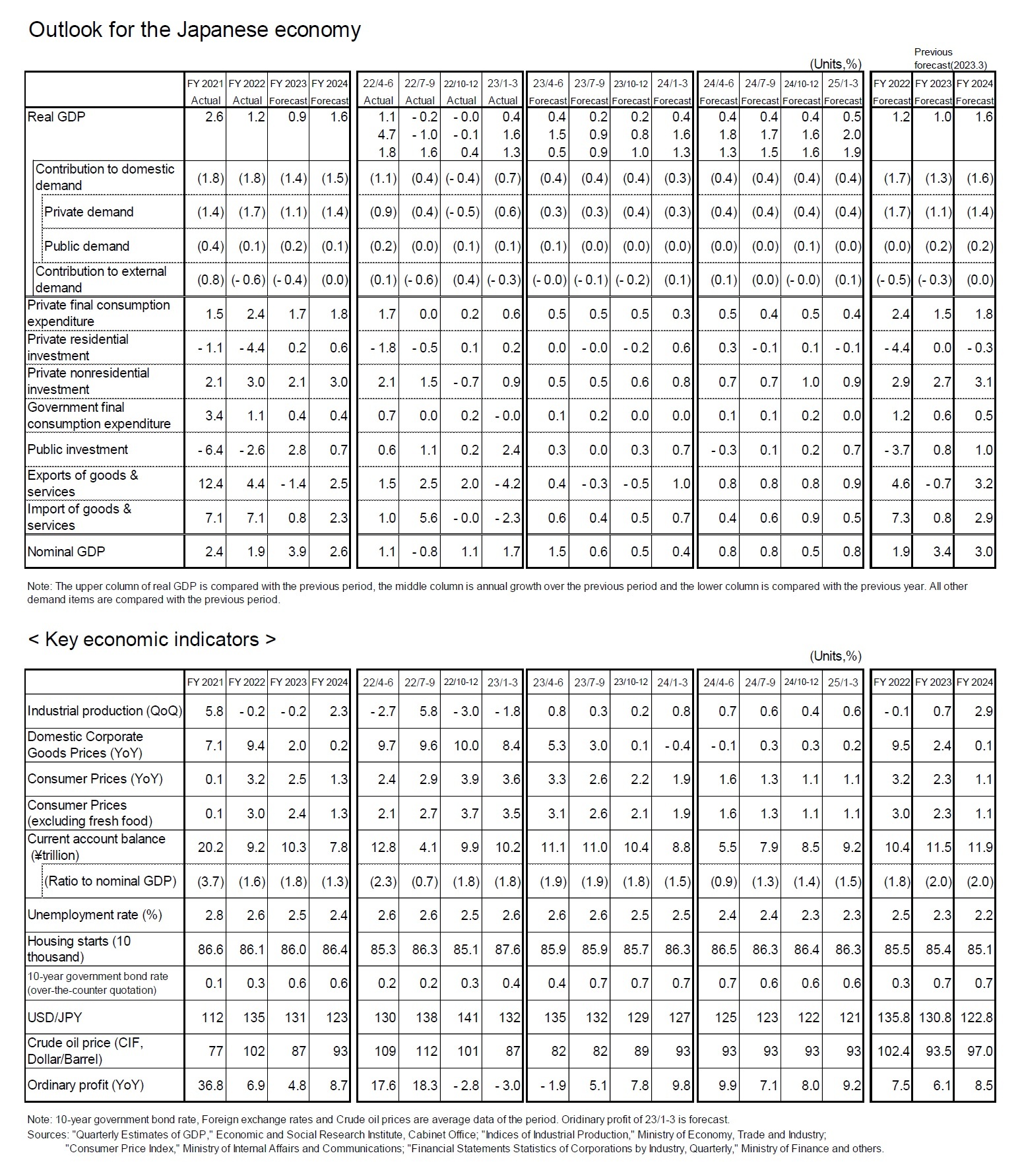

Indeed, while external demand is deteriorating, domestic demand remains resilient, as evidenced by the business sentiment of firms. The DI for the manufacturing sector (all sizes), which is strongly influenced by exports, peaked at +6 in the December 2021 survey and then declined, turning negative at -4 in the March 2023 survey, while the DI for the non-manufacturing sector (all sizes), which is more closely linked to domestic demand, turned positive in the June 2022 survey and has since risen to +12 in the March 2023 survey.

The Japanese economy is expected to continue to grow primarily as a result of domestic demand, as exports are not expected to be the driving force of the economy in the foreseeable future due to sluggish overseas economies. In the April–June quarter of 2023, exports of goods and services are expected to grow at an annualized rate of 1.5%, roughly the same as that seen in the January–March quarter, as domestic demand, mainly private consumption, will remain firm.

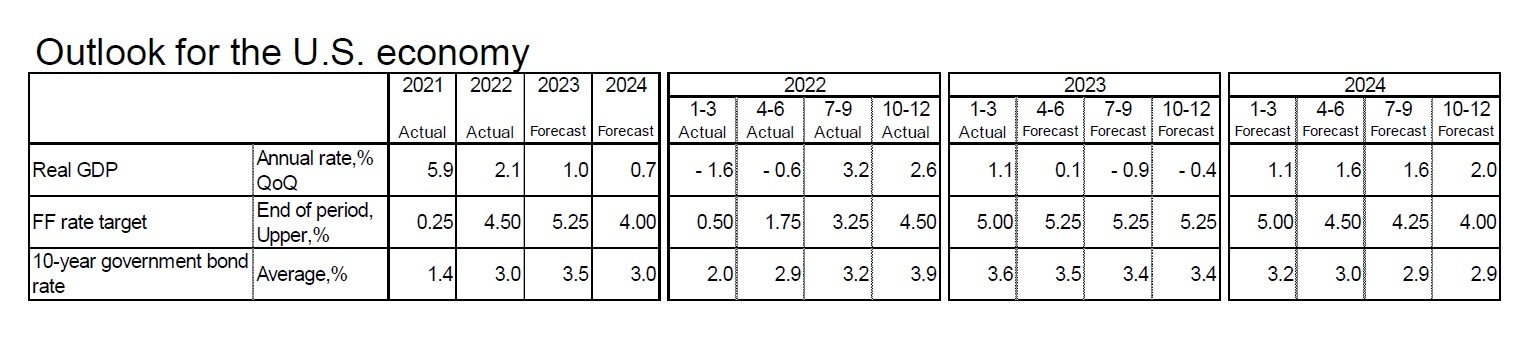

The growth rate will decelerate once to the zero percent level in the second half of 2023 when exports begin to decline due to the U.S. recession, but, after 2024, when the overseas economy is expected to recover, the growth rate will increase mainly due to a surge in exports.

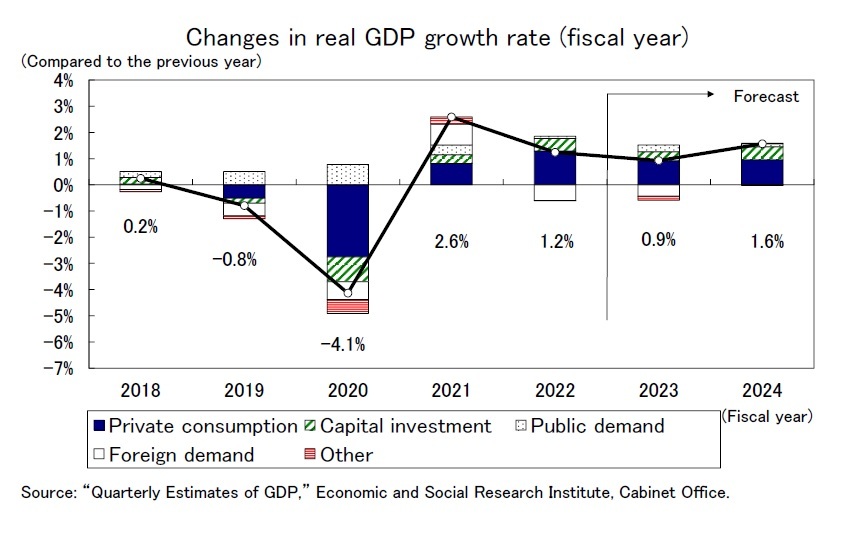

Real GDP growth is projected to be 0.9% in FY2023 and 1.6% in FY2024. At present, our main scenario is that the U.S. recession will remain mild and Japan will maintain its recovery trend. However, if the U.S. recession becomes severe, Japan's exports will suffer a significant downturn thanks to the deterioration of the global economy, and a recession will become inevitable for Japan as well.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}