(The impact of the re-accelerating weak yen and persistently high oil prices)

Since 2022, when the US began raising policy rates to cope with high inflation, the yen has continued to weaken against the dollar on the back of the widening Japan–US interest rate differential. The yen stopped weakening in the second half of 2023 when the US stopped raising interest rates but has been weakening again since April 2024 because the US interest rate cut is no longer expected due to the high inflation rate and other factors.

A weaker yen will improve corporate earnings, especially in the manufacturing sector, through higher exports. Additionally, the rise in import prices associated with a weaker yen will initially have a negative impact on households through a decline in real income associated with a rise in consumer prices. However, later, the improvement in corporate earnings will spill over to employment and wages, and households will generally benefit as well.

On the other hand, crude oil prices (WTI) have been calm recently, hovering around $80 per barrel, but remain high compared to pre-COVID-19 levels (2019 average in the low $50s per barrel). Rising oil prices will depress corporate earnings and reduce the real purchasing power of households through the outflow of income overseas due to worsening terms of trade.

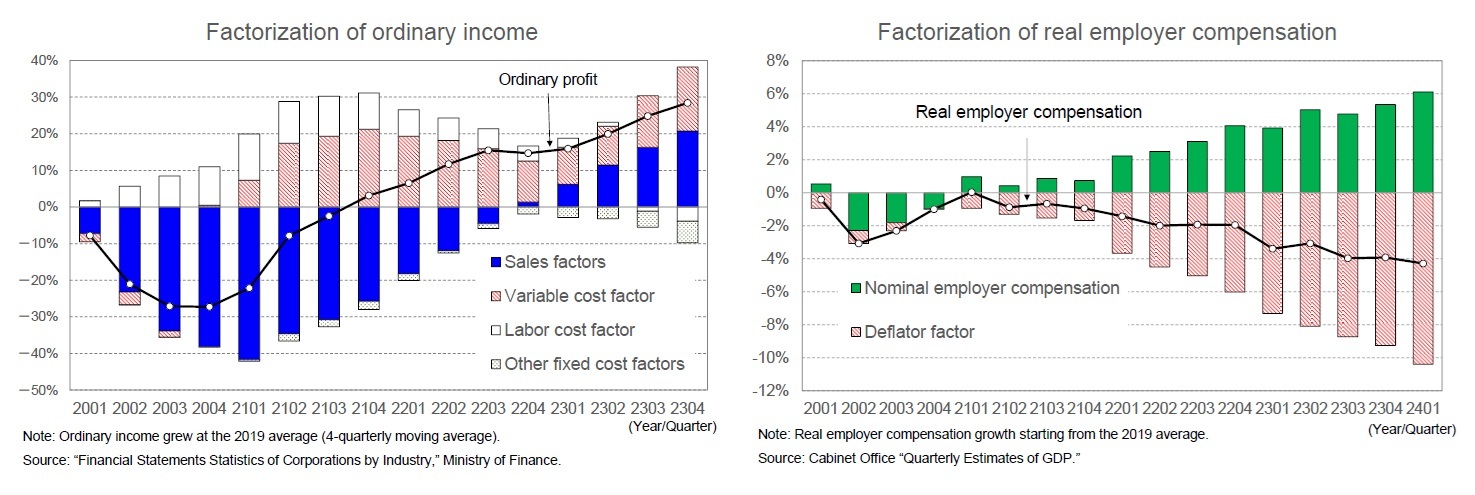

During the current phase of price hikes, companies have been able to fully pass on the increased costs associated with higher import prices to their prices, thus mitigating the negative impact of the weaker yen and higher oil prices. Corporate ordinary income for the most recent period (October–December quarter, 2023) is 28.4% higher than the pre-COVID-19 period (2019 average). Although the labor cost factor has slightly pushed down earnings, reflecting the higher wage rate, they have been significantly boosted by a substantial increase in sales, which had previously fallen due to the COVID-19 disaster. This increase has been due to the higher value of exports from the weaker yen and the transfer of prices to the domestic market (sales factor). Additionally, although variable costs have increased due to the weak yen and high crude oil prices, companies’ earnings have benefited from lower ratio of variable costs to sales due to sufficient price transfers (variable cost factor).

On the other hand, in the household sector, nominal employment compensation in the January–March quarter of 2024 increased by 6.1% from the pre-COVID-19 period (2019 average), but real employment compensation decreased by -4.3% because the household consumption deflator increased by 10.4% during that period. For the corporate sector, the benefits of a weaker yen outweighed the disadvantages of a weaker yen and higher oil prices, whereas, for the household sector, the disadvantages of a weaker yen and higher oil prices outweighed the benefits of a weaker yen.

{kind=link}

{kind=link}

{kind=link}