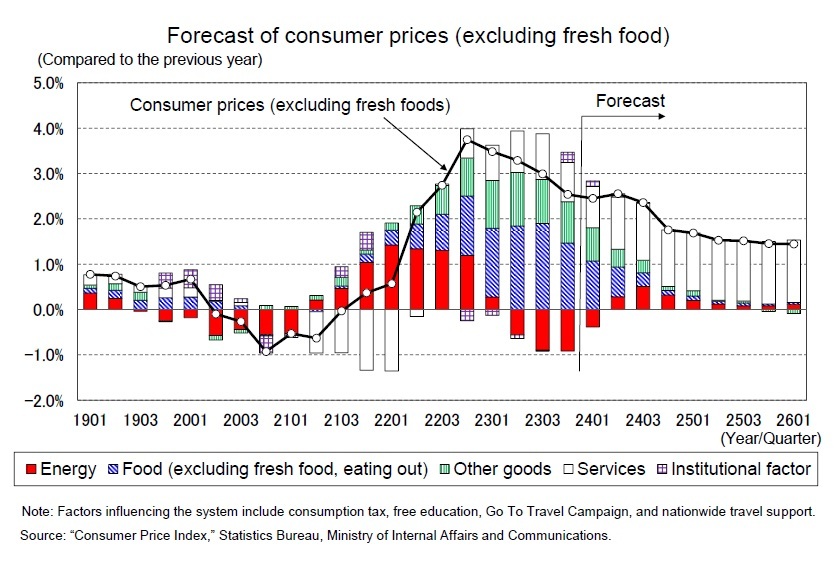

The current price hikes were initially due to large increases in the prices of energy and food, triggered by a sharp rise in import prices because of high crude oil prices and a weak yen. However, energy prices peaked at around 20% y/y in early 2022 and continued to slow down. After entering 2023, energy prices have been negative, partly because of the government’s drastic easing measures. In addition, food prices (excluding fresh food) rose to 9.2% y/y in August 2023 because of the spread of the price pass-on of higher raw material costs associated with soaring import prices, but decreased to 6.2% y/y in December, reflecting the stabilization of food prices in the upstream stage (i.e., import prices and domestic corporate prices).

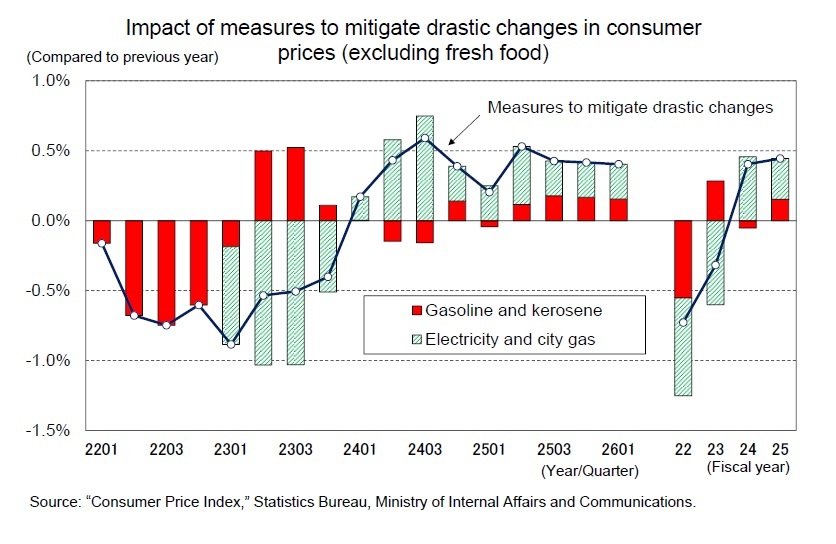

The price stabilization measures for gasoline and kerosene, in effect since January 2022, will continue until the end of April 2024. In addition, the measures for electricity and city gas, in effect since February 2023, will continue until April 2024, with an expected reduction of subsidies in May.

The current over-the-counter price of gasoline is about 190 yen per liter, without subsidies, and unless the yen appreciates and crude oil prices fall significantly, the price will remain well above the government’s target of 175 yen per liter for May 2024. Hence, it is highly probable that the drastic easing measures for gasoline and kerosene will continue after May 2024.

The current forecast assumes that the gasoline subsidy will remain as it is until the end of FY2024 and will continue in FY2025 with a reduced amount and that the subsidies for electricity and city gas will continue throughout FY2024 with a reduced amount and will end in FY2025.

The drastic easing measures depressed the core CPI inflation rate until the October–December quarter of 2023 but will boost it starting in the January–March quarter of 2024. On a fiscal year basis, the impact of the drastic easing measures on the core CPI inflation rate is expected to be about ˗0.7% in FY2022, ˗0.3% in FY2023, 0.4% in FY2024, and 0.4% in FY2025.

The rise in import prices, which are the main cause of high prices, has stopped and the increase rate in the prices of goods has already peaked. By contrast, the prices of services, which are linked to labor costs, have grown at about 2% y/y since August 2023, whereas, in December, the prices of goods (excluding fresh food) and services grew at the same rate (2.3%).

Furthermore, the prices of services which continue to grow in the low 2% range, slightly above the base salary increase in 2023, and will remain high as companies continue to pass on increased labor costs to their consumers.

Although the increase rate of the core CPI continues to be influenced by various support measures taken by the government, the underlying trend continues to slow down. Notwithstanding, the core CPI growth rate is not expected to fall below the BOJ’s target of 2% until the second half of FY2024, when the positive effect of the weaker yen is expected to wane, and the increase rate of the prices of food and other goods is expected to slow down.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}