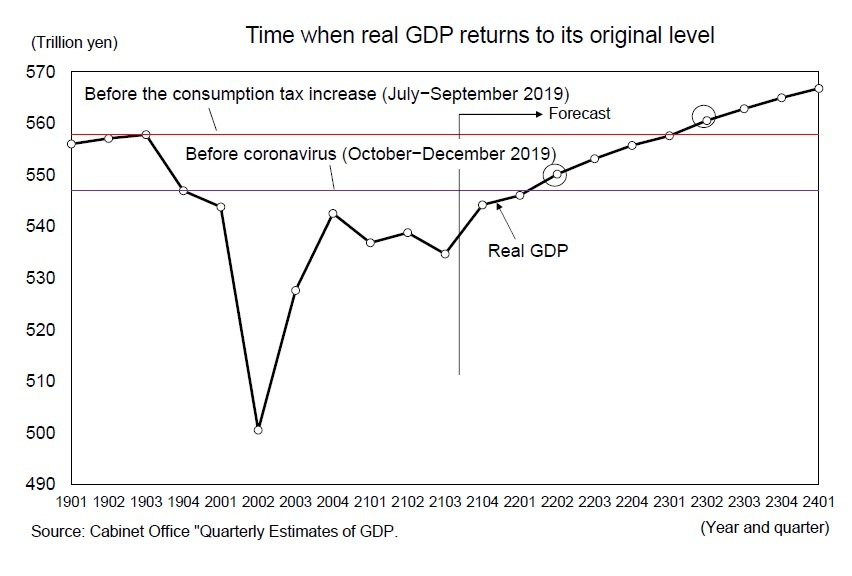

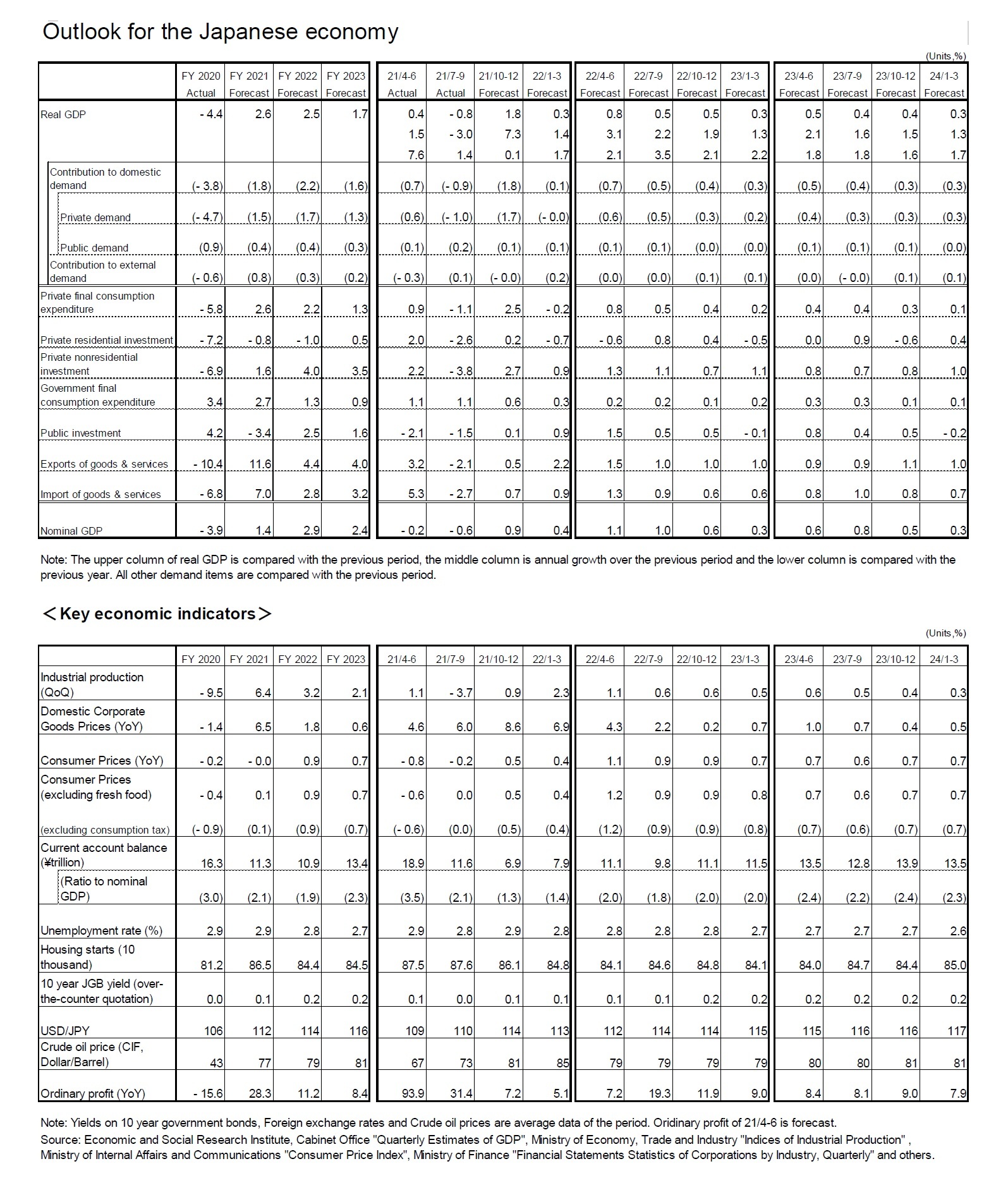

(Real GDP will surpass its most recent peak in FY 2023)

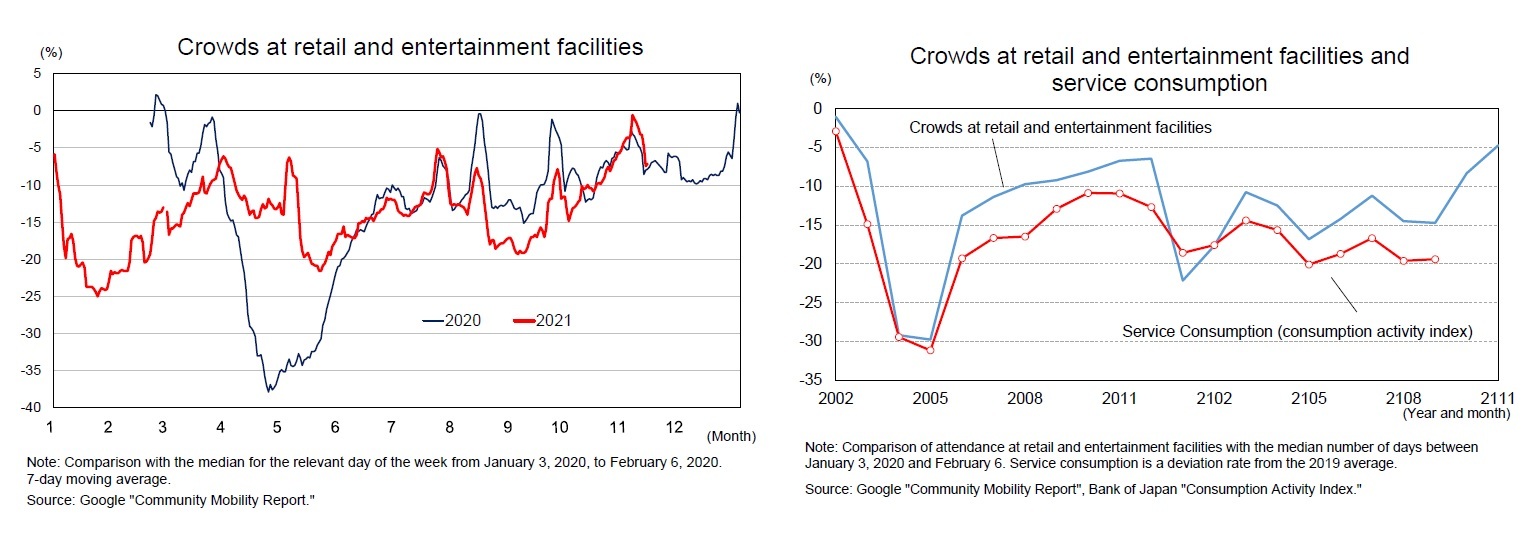

In 2020, the Japanese economy fell sharply in the first half of the year due to calls for self-restraint in the wake of the coronavirus outbreak and the issuance of the state of emergency order, but recovered at a faster pace than expected in the second half due to the resumption of economic activity following the lifting of the state of emergency order. However, with the reissuance of the state of emergency, economic activity remained sluggish from the beginning of 2021.

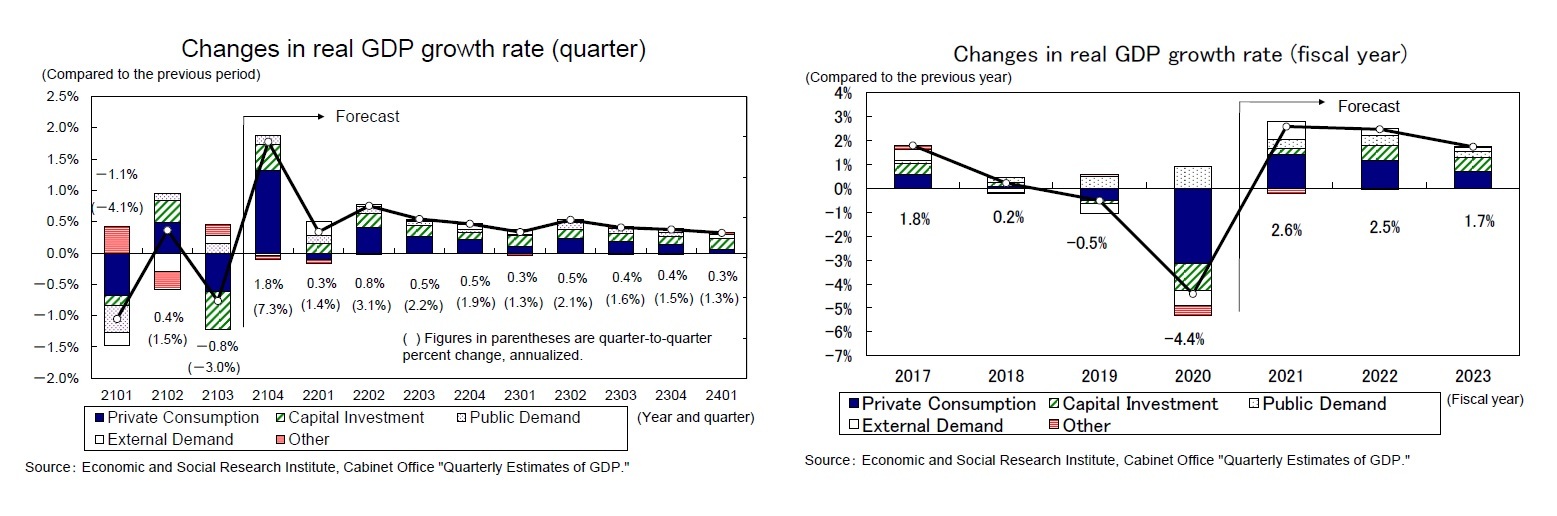

In the October–December quarter of 2021, we expect a high annual growth rate of 7.3%. Although exports, particularly of automobiles, will be sluggish due to the lingering effects of supply constraints, private consumption is expected to grow at a high rate of 2.5% from the previous quarter because consumption of face-to-face services, such as dining out and travel, will recover following the lifting of the state of emergency. Capital investment, which declined in the July–September quarter, is likely to turn upward in the October–December quarter, as corporate profits continue to improve.

Looking ahead, economic activity will continue to be heavily influenced by the coronavirus outbreak and the corresponding public health measures. Currently, the infection has been very limited in Japan, but the number of people infected with the virus has been rising again in Germany and the Netherlands.

In Japan, there is no denying the possibility that the number of infected people will increase in the future due to the emergence of new variants and changes in temperature, and if action restrictions are tightened as in the past, there is a risk that economic activity will stagnate again, particularly in the consumption of face-to-face services. On the other hand, if sufficient progress is made in the expansion of the medical system and the appropriate allocation of medical resources, even if the number of infected patients increases to a certain extent, the need to restrict economic activities strictly will decrease, and the economy may greatly improve.

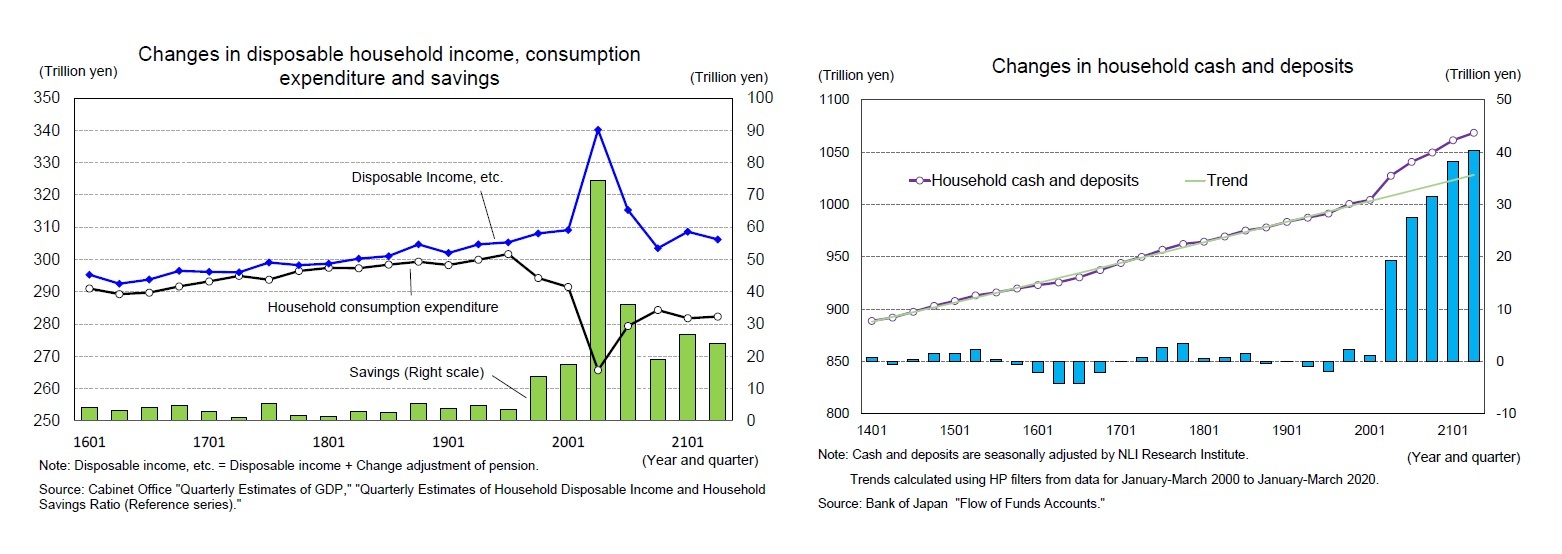

The real GDP growth rate is expected to be 2.6% in FY 2021, 2.5% in FY 2022, and 1.7% in FY 2023. Even if restrictions on economic activities are eased, consumer spending will not recover in earnest because a certain level of concern about infectious diseases will curb consumption of face-to-face services. Private consumption saw a sharp decline of 5.8% in FY 2020 and it is expected to increase 2.6% in FY 2021, 2.2% in FY 2022, and 1.3% in FY 2023. On the one hand, the pace of recovery of consumption is quite slow. The level of private consumption on a fiscal year basis will not exceed the latest peak (FY 2018) until FY 2024.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}