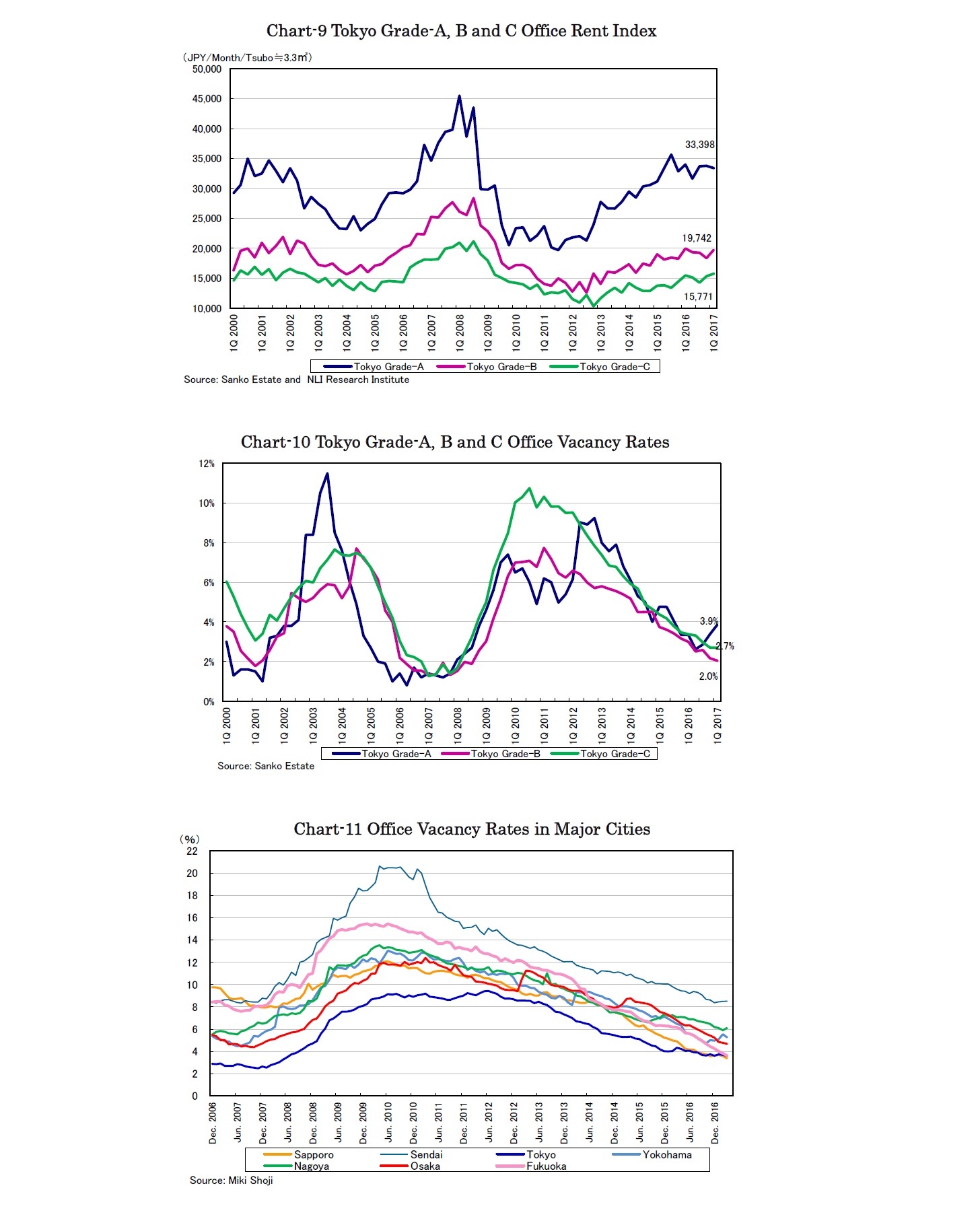

1) Office

The rent index of Tokyo Grade-A offices declined by 1.1% q-o-q and 1.8% y-o-y to 33,398 JPY per month per tsubo in the first quarter (Chart-9). Grade-A office rents have been on a declining trend since peaking in the third quarter of 2015. Tenants have taken the initiative in leasing negotiations on the back of the 1.4 million square meters of new supply scheduled in 2018, even with current favorable business conditions and corporate earnings.

On the other hand, the rent index of Tokyo Grade-

2 offices rose by 1.1% q-o-q and declined by 1.8% y-o-y while that of Tokyo Grade-C

3 offices rose by 1.1% q-o-q and 1.8% y-o-y. Grade-C office rents have been strong without direct influence by the glut of coming Grade-A supply. However, office rents of all grades have been much lower than those at the peak in 2008.

Vacancy rates of Grade-A offices deteriorated to 3.9% for the third consecutive quarter (Chart-10). On the contrary, vacancy rates of Grade-B and C have improved and have driven the rent increase.

Office vacancy rates in major cities other than Tokyo have been improving supported by limited new supply excluding Yokohama, where some tenants moved to their own buildings, and Nagoya, where a landmark building was completed next to a JR station (Chart-11).

{kind=link}

{kind=link}

{kind=link}