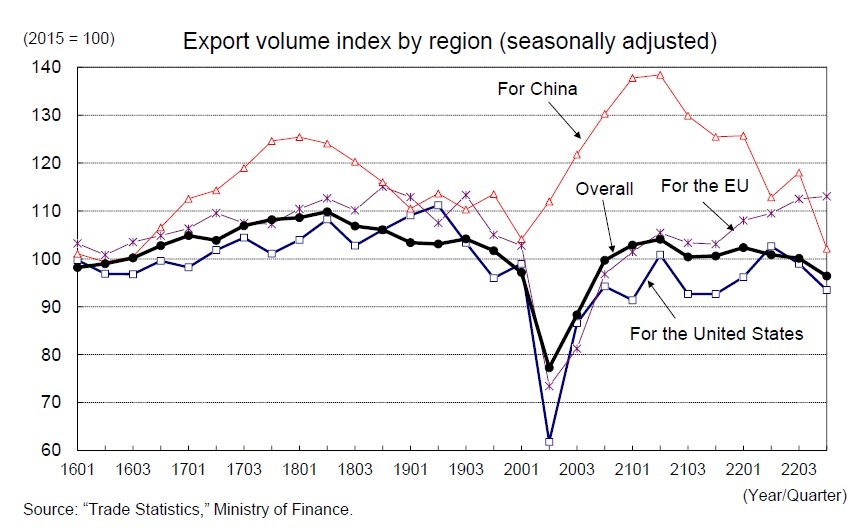

The export volume index (seasonally adjusted by the institute) for the October–December quarter of 2022 declined for the third consecutive quarter to -3.4% from the previous quarter, while the contraction widened from -0.4% in the July–September quarter. Regionally, exports to the EU remained firm, but those to China, whose economy has been in a slump since the spread of COVID-19 after the lifting of the zero-COVID-19 policy, fell sharply, while those to the United States, whose economy has been slowing, remained sluggish. By product category, sales of semiconductors and other electronic components as well as telecommunications equipment and other IT-related products have declined due to sluggish global demand for semiconductors, while sales of automobiles, which are still affected by supply constraints, have been seesawing.

In the July–September quarter of 2022, the Industrial Production Index increased by as much as 5.8% from the previous quarter, but in the October–December period, production decreased by 3.0%—the first decrease in two quarters. Automobiles, which are still affected by supply constraints, decreased by 4.3% from the previous quarter, and electronic components and devices decreased by 5.9% from the previous quarter (down 7.8% in the July–September quarter), reflecting the adjustment of the global IT cycle.

The manufacturing industry production forecast index, which shows companies' production plans, did not rise at all from the previous month in January 2023 but it did increase by 4.1% in February. However, considering that actual production tends to deviate significantly from the forecast index, it can effectively be read as a production cut plan. While domestic demand's steady strength, particularly in consumer spending, will be supportive, production is expected to remain weak for the time being because exports are likely to remain sluggish against the backdrop of deteriorating overseas economies, especially in Europe and the United States.

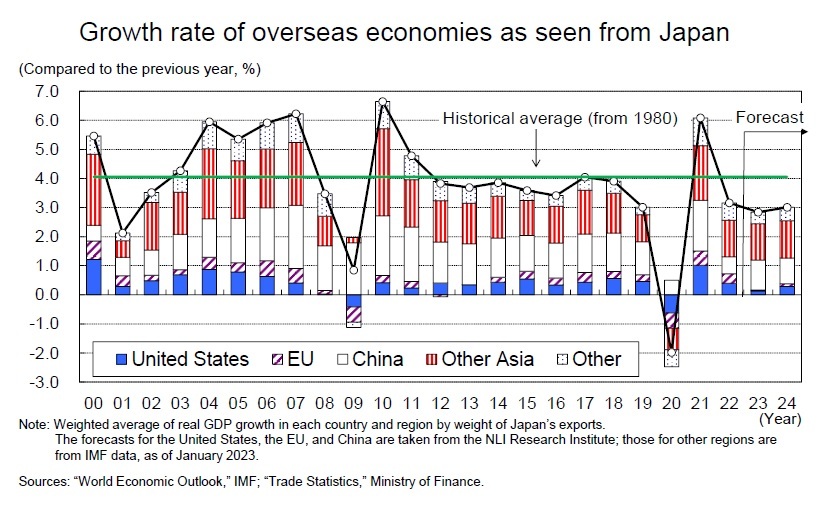

In the October–December quarter of 2022, real GDP grew at an annualized rate of 2.9% in the United States and at 0.4% in the euro area, but it is expected to contract in the January–March quarter of 2023 due to high inflation and monetary tightening. By contrast, China, which saw growth in real GDP growth rate drop sharply to 3.0% in 2022 from 8.4% in 2021 as a result of its zero-COVID-19 policy and the accompanying lockdown, is likely to recover in 2023 following the end of the zero-COVID-19 policy.

The growth rate of overseas economies, weighted by the weight of Japanese exports, declined by approximately 2% in 2020 as a result of the impact of the COVID-19 virus infection, then increased by as much as 6% in 2021 in response to the decline, but it will slow significantly again to around 3% in 2022 before declining further to the upper 2% range in 2023. This is because China’s real GDP's growth rate is expected to rise from 3% to 5%, the United States’ growth rate will fall to 0.7% in 2023 from 5.9% in 2021 and 2.1% in 2022, and the euro area’s growth rate will drop from 5.2% in 2021 to 3.5% in 2022 and finally to 0.4% in 2023.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}