The financial system should support the corporate and household sectors to weather a temporary external shock, but the system has sometimes accelerated downward spirals in the past. The regulators aimed to ensure that the financial system would work as a shock absorber rather than as an amplifier.

The financial sector policy makers had to address the following four concerns to attain this aim.

(1). Operational risks

Regulators were concerned that the infection and public health policy measures such as lockdowns may disrupt the business continuity of financial institutions. They were also concerned that dependencies on remote work may increase the vulnerability against cyber and IT incidents.

(2). Credit crunch

Bankers are said to lend umbrellas on sunny days and take them back on rainy days. If bankers become excessively risk-averse, healthy corporations and households that face temporary cash shortages but have good prospects of recovering after the pandemic could unnecessarily go bankrupt. Households could be forced to sell their residences or face an impaired credit record and lose future recovery opportunities.

Regulators were also concerned whether the financial system could bear the shock.

(3). Market and liquidity risks

Financial institutions might incur losses due to increased market volatility arising from uncertain economic prospects. Market participants may become cautious about the counterparties’ credit standing and their own funding, refraining from purchasing assets and consequently lowering market liquidity. Declines in market liquidity aggravate the funding liquidity of entities as they cannot obtain cash by selling assets. Funding fears could lead to a run on the capital market.

(4). Solvency risks

If the COVID-19 pandemic continues to deprive corporations and households of revenues, banks’ loans to them may soar and the solvency of banks might be impaired. Problems at banks can exacerbate the credit crunch, market volatility, and liquidity shortages. A vicious circle between financial and economic crises could then be triggered.

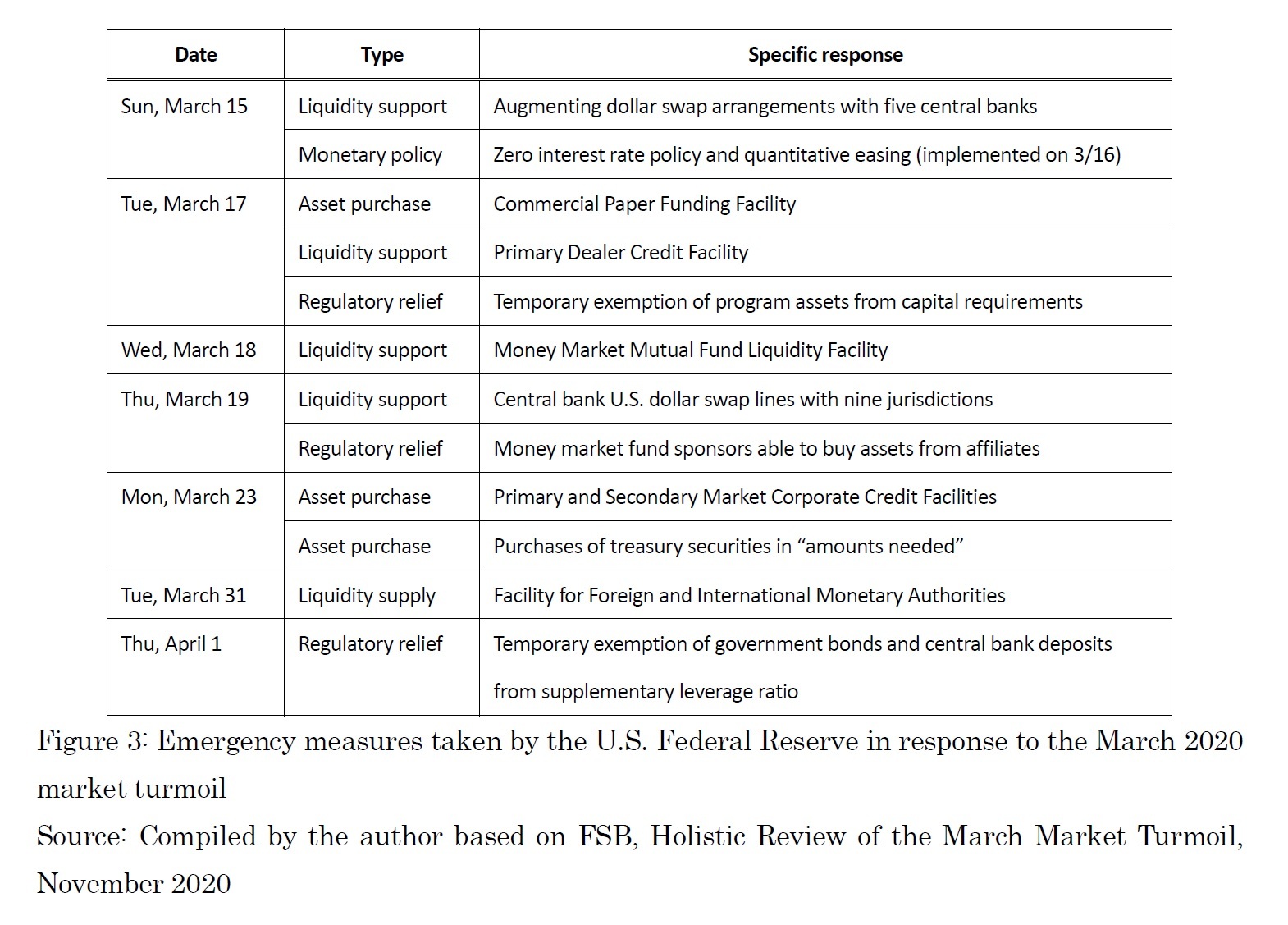

Initially, COVID-19 was considered an issue unique to China, but the second week of March 2020 saw a sudden change in perceptions. New York State declared an emergency on Saturday, March 7, 2020. Italy started a lockdown on Monday, March 9, and the World Health Organization declared a pandemic on Wednesday, March 11. U.S. President Donald Trump declared an emergency on Friday, March 13.

Regulatory authorities globally started to explore responses in financial sector policies while facing uncertainties over

・How long the pandemic would persist

・Whether a second or third wave would come

・When vaccines and remedies would become available

・How effective vaccines would be

・How the pandemic would affect supply and demand

・What the post-COVID-19 economy and society would be like.

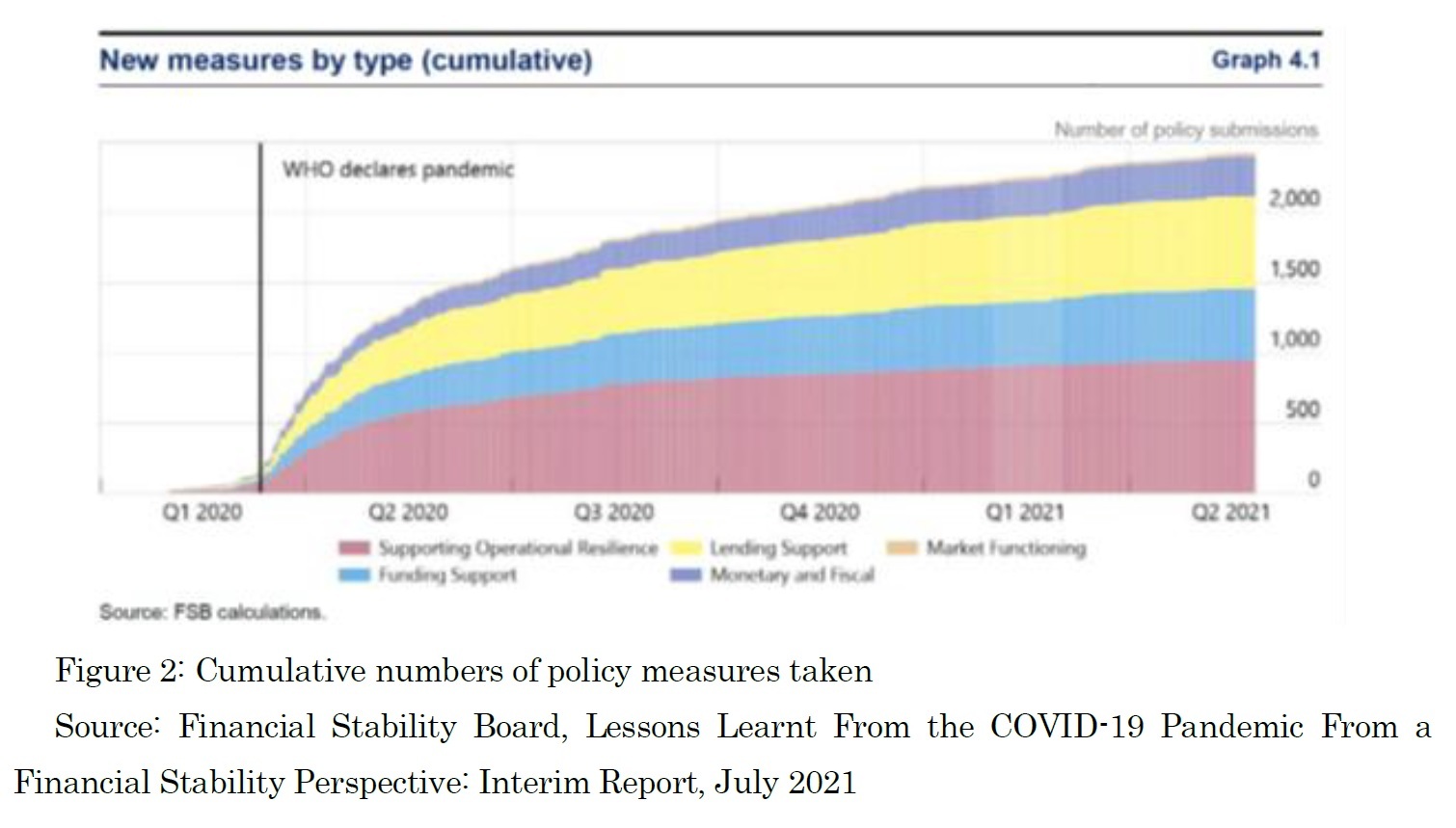

Despite the uncertainties, regulators acted promptly. Figure 2 shows the changes in the cumulative numbers of policy measures taken. According to the FSB, "The speed, scale and scope of the policy response to COVID-19 was without precedent."

1 Indeed, within a month from the second week of March 2020, more than 1,000 new measures were taken ranging from those supporting operational resilience (red) to lending support (yellow), funding support (blue), monetary and fiscal policy measures (purple), and those related to market functioning (brown).

{kind=link}

{kind=link}

{kind=link}