The TSE REIT Index declined by 4.3% in the first quarter (Chart-21) as foreign investors sold aggressively with 28.5 billion JPY of net selling volume. The office sector declined by 5.1%, the residential sector by 2.1% and other sectors – including retail and logistics – by 4.1%.

At the end of March, the value of the J-REIT market was 11.9 trillion JPY, while the price-to-NAV ratio was 1.2 times and the dividend yield was 3.7%, with a 3.7% yield spread on 0% of 10-year JGBs.

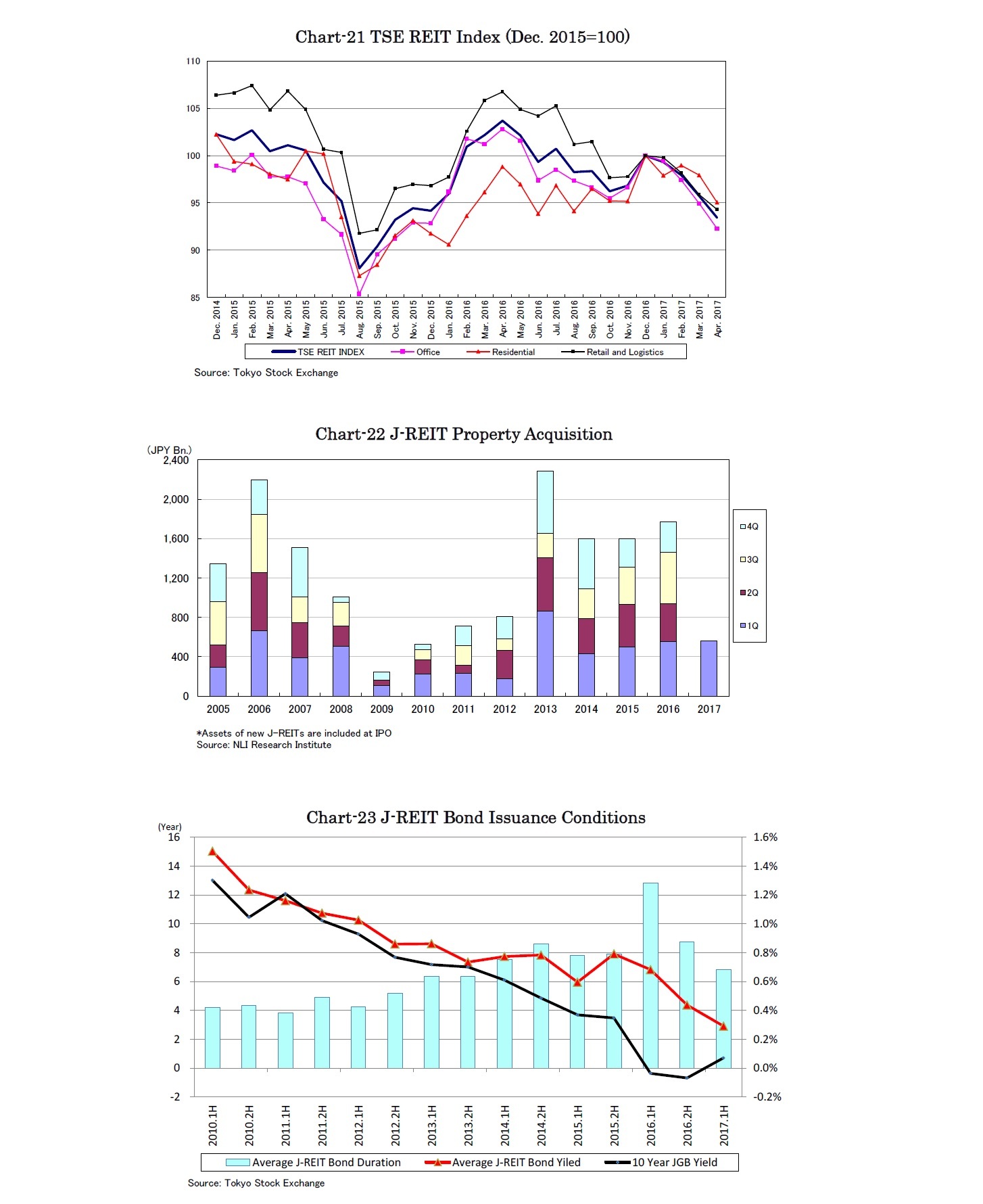

J-REITs acquired properties amounting to 561 billion JPY in the first quarter, increasing by 2% y-o-y (Chart-22). Mori Trust Hotel REIT was listed with 4 assets valued at 102 billion JPY, and the number of J-REITs increased to 58.

Though the recent interest rate hike in the U.S. has worried investors, 10-year JGB yields have remained around 0% due to the "yield curb control by Bank of Japan" while debt funding conditions have been extremely favorable.

J-REITs issued 32 billion JPY of bonds at an average yield of 0.32% in the first quarter, 0.51% lower than in the fourth quarter of 2016 (Chart-23). The current bond issuance conditions for J-REITs are 0% for 3-year, 0.2% for 5-year and 0.5% for 10-year bonds.

The average bond duration held by J-REITs was greater than 10 years under the negative interest rate environment last year. However, J-REITs have flexibly managed bond issuance conditions and the average duration has shortened to 7-8 years following introduction of "yield curb control by Bank of Japan." The current average debt costs of J-REITs are 0.8%. In the case that debt costs are brought to 0.5%, earnings of J-REITs will increase by 5%.

{kind=link}