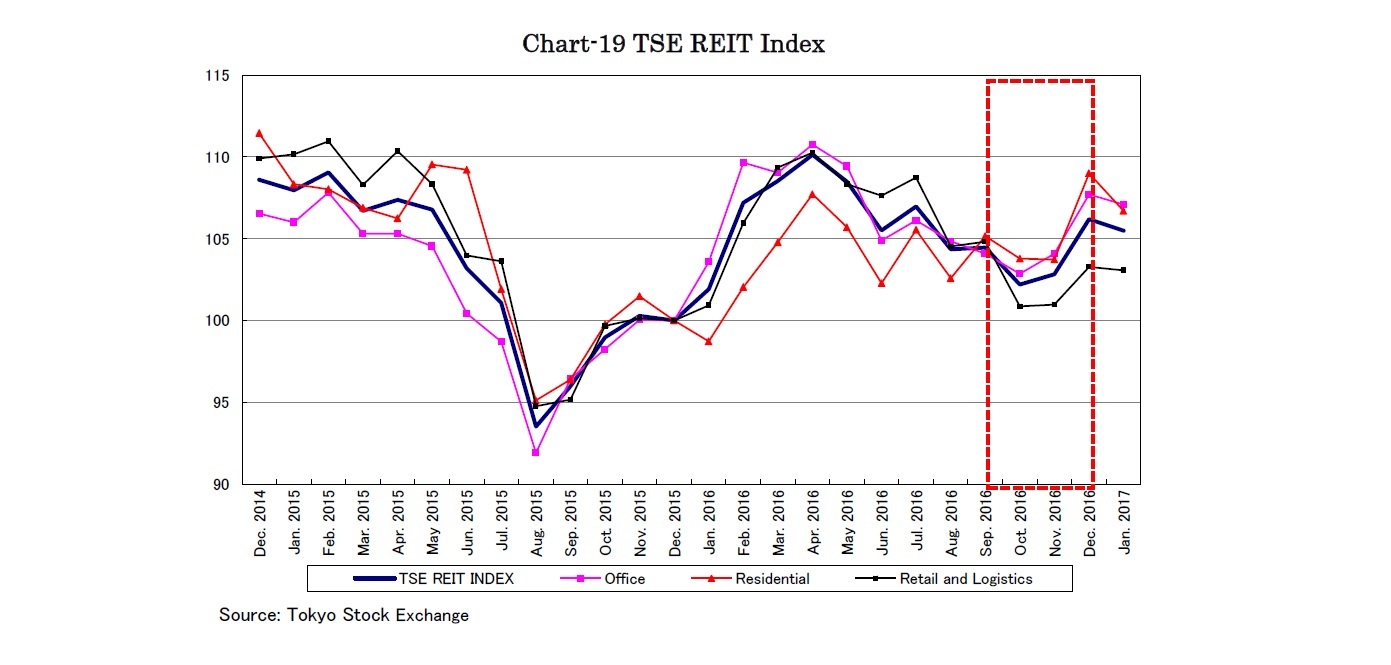

The TSE REIT Index rose by 1.7% q-o-q in the fourth quarter pulled up by the equity market rallying after the U.S. presidential election, despite having stagnated before the event. The office and residential sectors rose by 3.5% and 3.7% q-o-q respectively, while other sectors – including retail and logistics – declined by 5.1% (Chart-19). At the end of December, the J-REIT market value was 12.1 trillion JPY, while the price to NAV ratio was 1.2 times and the dividend yield was 3.5%, with a 3.5% yield spread on 0% of ten year JGBs.

The TSE REIT Index rose by 6.2% in 2016 after declining in 2015. Even affected by the significant events overseas such as the U.K. withdrawal from the EU and the U.S. presidential election, the financial results of J-REITs have steadily improved and supported the unit prices.

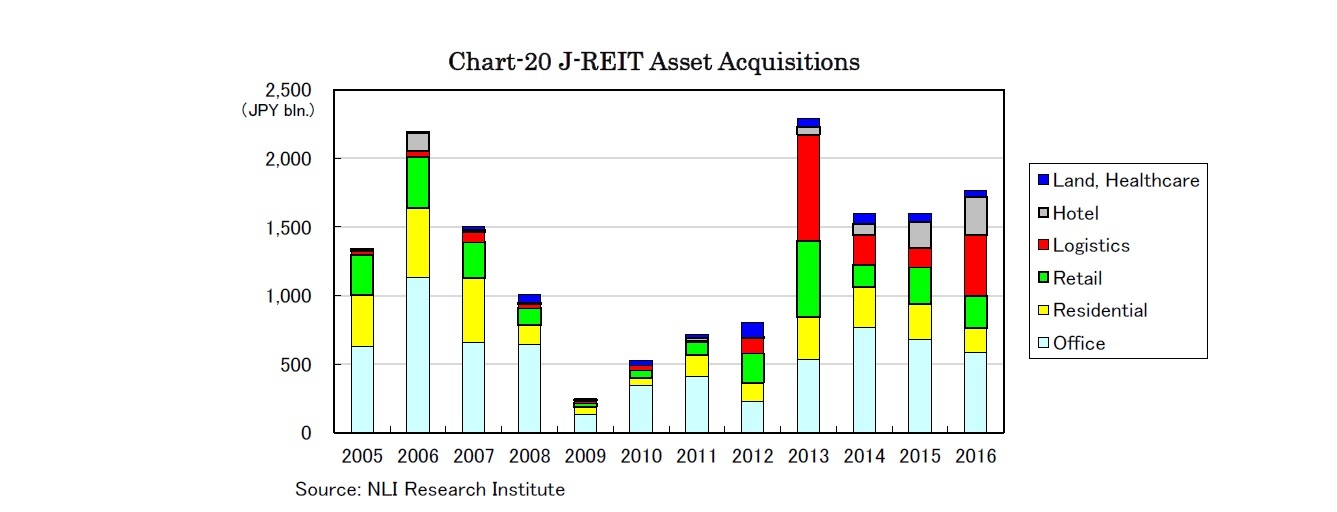

J-REITs acquired property assets amounting to 1.77 trillion JPY with seven IPOs in 2016 (Chart-20). The acquisition volume was 11% more than in 2015, posting the third largest yearly amount in history even when the entire market transaction volume shrank in Japan. J-REITs acquired an increasing number of logistics facilities and hotels noticeably, while the total acquisition volume of the traditional three sectors such as office, residential and retail decreased y-o-y, accounting for the lowest ever 56% of total volume. Besides that, acquisition volume in the five central wards of Tokyo accounted for only 23% of total volume, shrinking from 28% in 2015. Pursuing yield incremental acquisitions, J-REITs have shifted acquisition targets from central Tokyo to suburban areas and from core to sub categories.

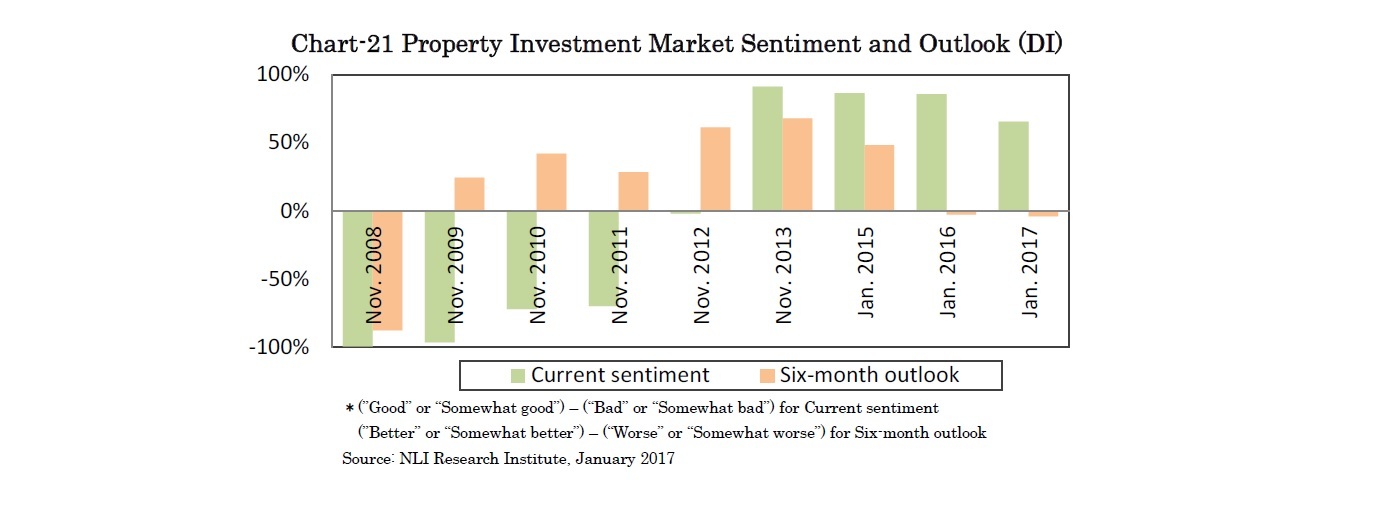

The funding environment has been comfortable with the average J-REIT bond issuance condition being 10 years and 0.51%.

{kind=link}

{kind=link}

{kind=link}