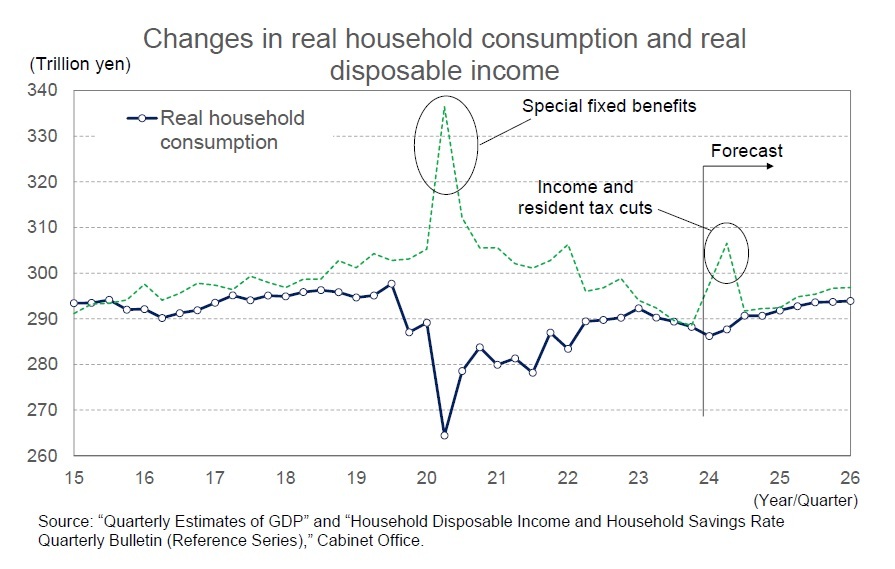

With the household savings rate having fallen to the pre-COVID-19 level and with no hope of a boost from excess savings, real disposable income will determine future consumption. Real disposable income is currently below the pre-COVID-19 level. Inflation will continue to restrain real income, but wage hikes and income and inhabitant tax cuts are expected to provide a boost. Although the effect of the tax cuts will be temporary, real disposable income is expected to remain firm from the second half of FY2024, mainly due to an increase in real employee compensation as the rate of inflation slows.

Since only 20–30% of the tax cuts are expected to go to consumption, the household savings rate will temporarily rise significantly. However, after the tax cut effects wear off, it is expected to decline to almost zero.

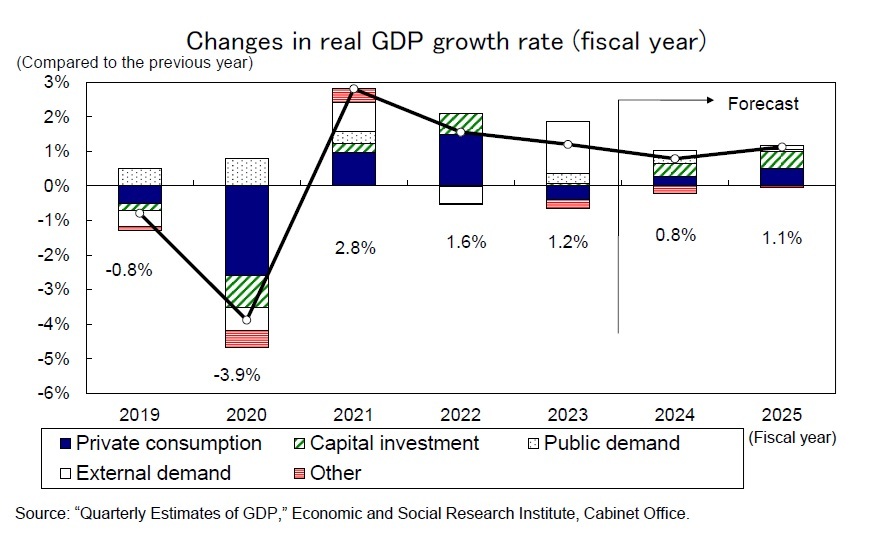

Private consumption declined -0.6% compared to the previous year in FY2023, the first decline in three years, but is expected to increase by 0.5% in FY2024, followed by an increase of 1.0% in FY2025. Although the effect of the tax cuts will wear off in FY2025, higher growth in real employee compensation will contribute to the increase in disposable income.

(Businesses have a strong appetite for capital investment)

Capital investment in FY2023 grew at a modest 0.4% compared to the previous year. However, it is expected to remain steady at 2.4% in FY2024 and 2.9% in FY2025.

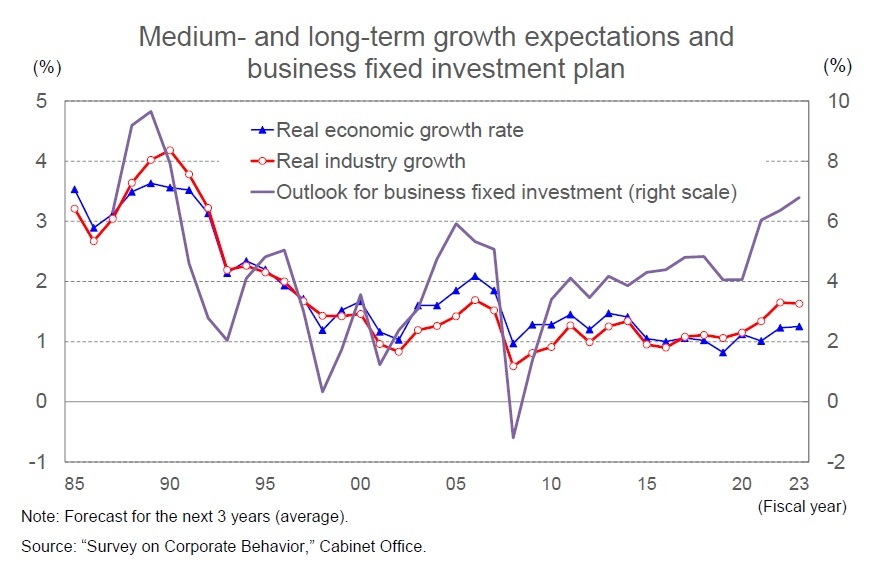

In the Bank of Japan’s March 2024 Tankan survey, capital investment plans for FY2023 (all sizes and all industries, including software and R&D investment but excluding land investment) were revised downward by -1.9% from the December 2023 survey but still showed a significant growth of 10.2% compared to the previous year. The initial plan for FY2024 is 4.5% year on year, which is approximately the same level of growth as the FY2023 initial plan (4.4% year on year).

Although capital investment in the GDP statistics has been sluggish partly due to supply constraints caused by labor shortages, the underlying trend appears to be recovering. This is mainly in response to labor shortages, telework-related investment, and software investment for digitization, supported by high corporate earnings.

A major influence on medium- to long-term trends in capital investment is the expected growth rate of companies. One reason for the long-term sluggishness in expected growth rates can be attributed to the belief among many corporate managers that a shrinking domestic market is inevitable due to a declining population.

{kind=link}

{kind=link}

{kind=link}