1| Formation Stage of the Real Estate Bubble in Japan

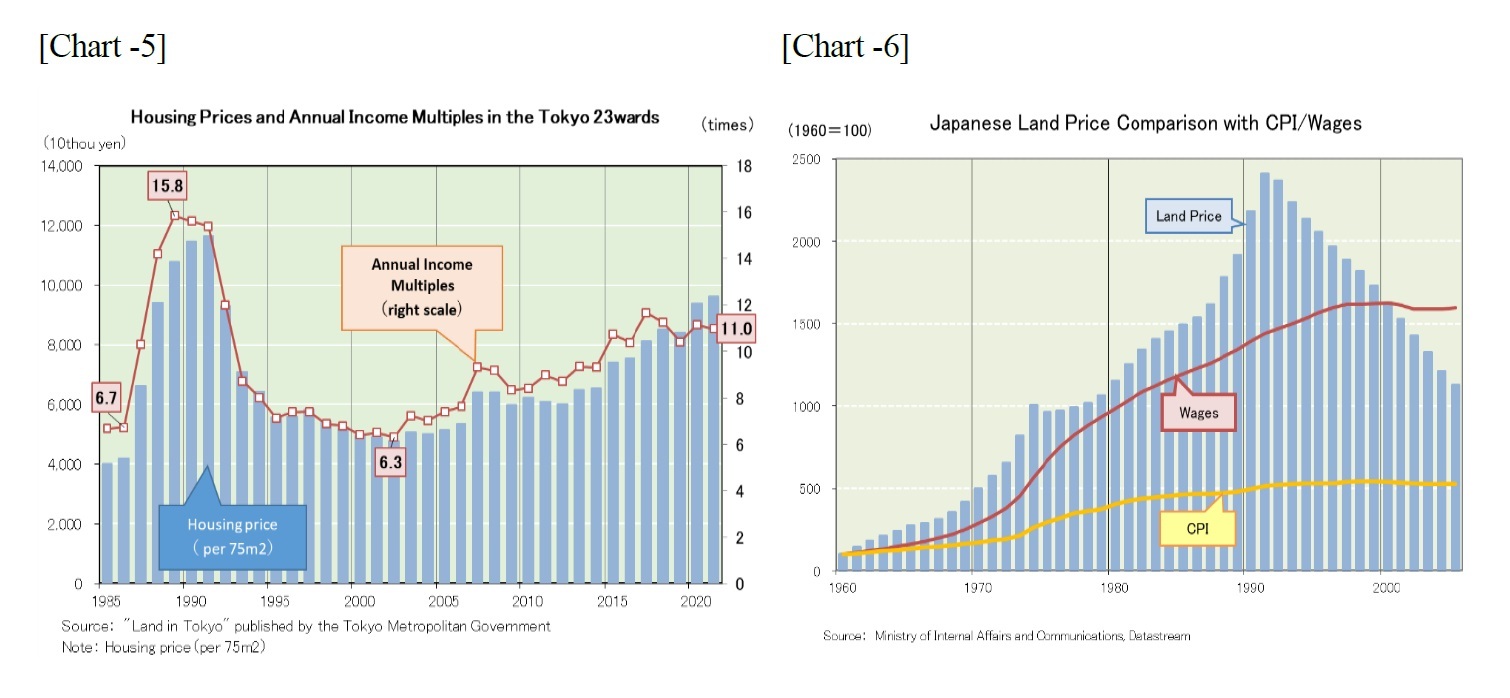

The real estate bubble in Japan began to take shape around 1987. According to data from "Land in Tokyo" published by the Tokyo Metropolitan Government (Chart 5), the price per 75 square meter of an apartment in the Tokyo 23wards area was 41.85 million yen (6.7 times the annual income) in 1986. However, it surged to 66.08 million yen (10.3 times the annual income) in 1987, 94.2 million yen (14.2 times the annual income) in 1988, and 107.85 million yen (15.8 times the annual income) in 1989.

This surge was fueled by the "land price myth," which asserted that land prices would always rise. Following the Plaza Accord in 1985, Japan experienced a sharp appreciation of the yen, prompting Japanese companies to enhance their ability to cope with the strong yen by expanding overseas production and cutting costs through streamlining and automation. Additionally, the Bank of Japan lowered its discount rate five times to address the economic downturn caused by the strong yen, leading to a structural shift from reliance on external demand to domestic demand. With low interest rates, Japan witnessed a speculative boom known as "Zaitech," with real estate emerging as a favored investment option.

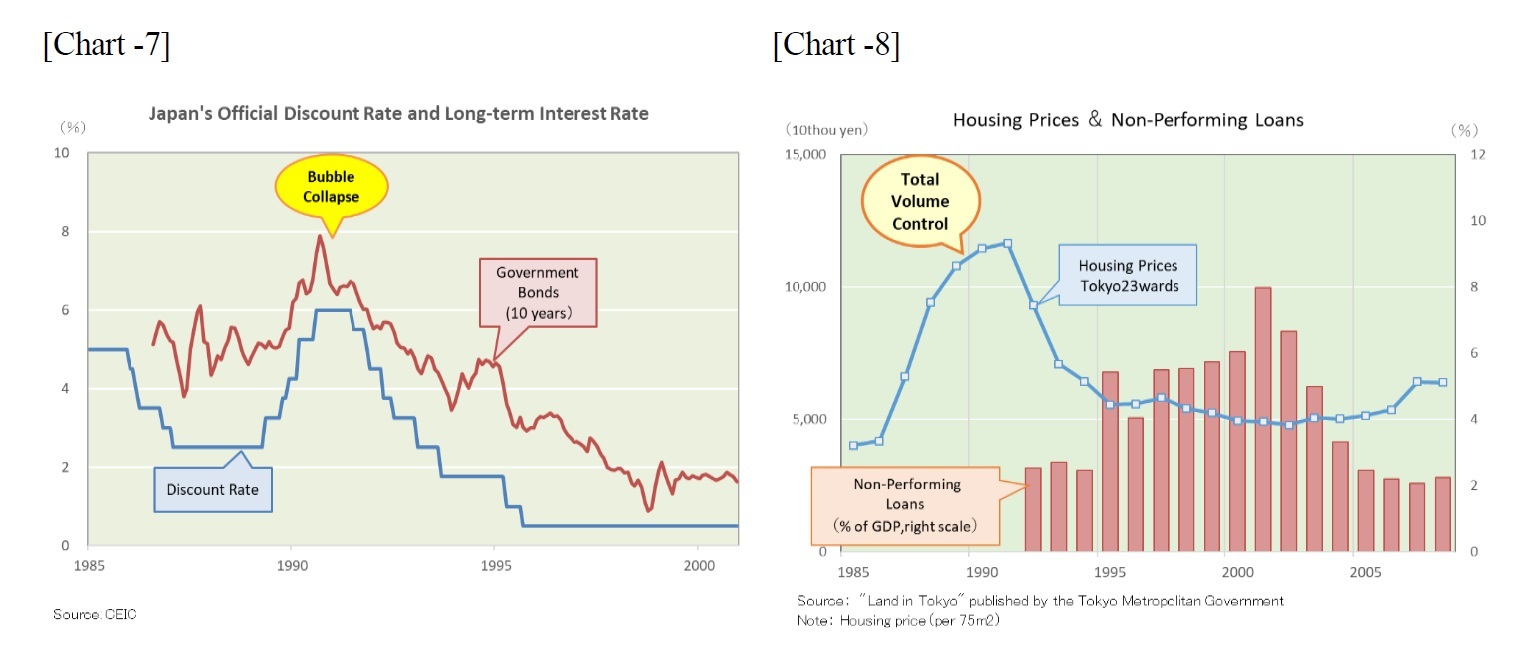

Examining the historical trends in land prices in Japan (Chart 6), we observe that while prices experienced periodic declines, they generally continued to rise over the long term, rebounding after a few years. Moreover, the growth in land prices consistently outpaced the growth in consumer prices and wages, reinforcing the notion of the "land price myth."

Consequently, real estate developers spearheaded a surge in real estate investments, while general corporations actively acquired real estate, and ordinary individuals began investing in condominiums with borrowed funds. Financial institutions provided financial backing for these speculative activities. As a result, Japan as a whole became complacent about high prices, leading to an unprecedented rise in real estate prices.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}