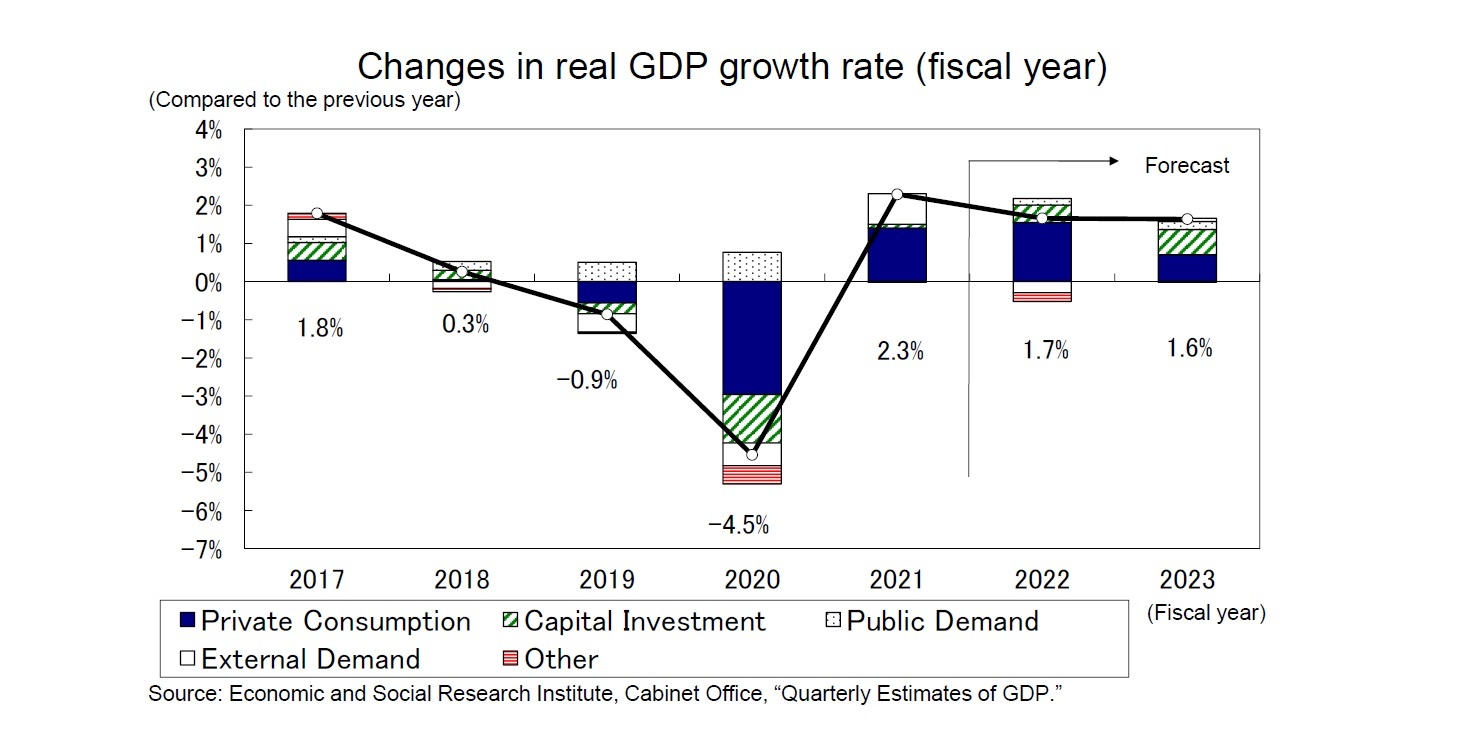

<Real GDP growth rate: 1.7% in FY 2022, 1.6% in FY 2023>

In the April–June quarter of 2022, real GDP grew from the previous quarter at an annualized rate of 2.2%, driven in part by a strong 1.1% quarter-on-quarter increase in private consumption following the end of COVID-19-related priority preventative measures.

Real GDP is expected to grow by 1.7% in FY 2022 and 1.6% in FY 2023. A boost from exports is not currently expected due to the continuing slump in overseas economies. However, positive growth is expected to continue beyond the July–September quarter of 2022 in the absence of state of emergency or other restrictive measures; this is mainly due to increases in private consumption and capital investment backed by high levels of household savings and corporate earnings.

However, there are significant downside risks, including a sharp slowdown in the United States economy due to monetary tightening, a downturn in China’s economy due to the government’s continued zero-COVID-19 policy, a worsening of the Ukrainian situation, curbs on economic activities due to winter electricity shortages, and uncertainty about policy responses to the spread of COVID-19.

Consumer price inflation (excluding fresh food) is forecast at 2.4% in FY 2022 and 1.0% in FY 2023. This rate will increase to the upper 2% range around autumn 2022 due to the accelerated pace of food inflation and increasing price pass-through for a wide range of products in response to the rise in import prices accompanying the yen’s depreciation. However, growth will slow to the upper zero percent range in the second half of FY 2023, when the impact of rising raw material prices will have run its course.

{kind=link}