3|Application Process of the EITC and Standard of Application

Unit of the assessment for South Korean income tax is an individual, while the EITC evaluates whether a household is eligible or not. Recipients of the EITC were limited to employees, and the eligibility has been expanded to the individual proprietor since 2015; however, proprietors without business registration and professionals like lawyers, patent agents, certified public accountants, physicians, pharmacists and so on are excluded. In the initial phase, employees were the only beneficiary of the EITC as income-capture rate of individual proprietors is lower than the rate of employees.

There are two ways to apply for the EITC: submitting an application within a certain period and after the period. If people apply for the EITC between 1

st of May and 1

st of June every year, they can apply for the assistance within a certain period. On the other hand, if a person applies after the period, between 2

nd of June and 1

st of December, 10% reduced subsidies for the EITC and the Child Tax Credit (CTC)

11are provided. People who are eligible to apply for the EITC can apply for it by telephones

12, mobile phones, mobile websites and the internet or visiting tax office

13.

To apply for the EITC and the CTC, following four standards are needed to be fulfilled.

(1)Standard for Household

- EITC: As of December 31 every year, the applicant has a spouse or a child under 18 to support, or the applicant is older than 60.

- CTC:As of December 31 every year, the applicant has a spouse or a child under 18 to support.

A child to support needs to meet all of the requirements.

・A child whom a householder supports or an adopted child who lives with a householder. However, grandchild and siblings can be included in his or her dependents

14.

・As of December 31 of the previous year, a child is younger than 18; however, there is no age requirement to the severely disabled.

・Annual gross income is 1 million won and less.

(2)Standard for Gross Income

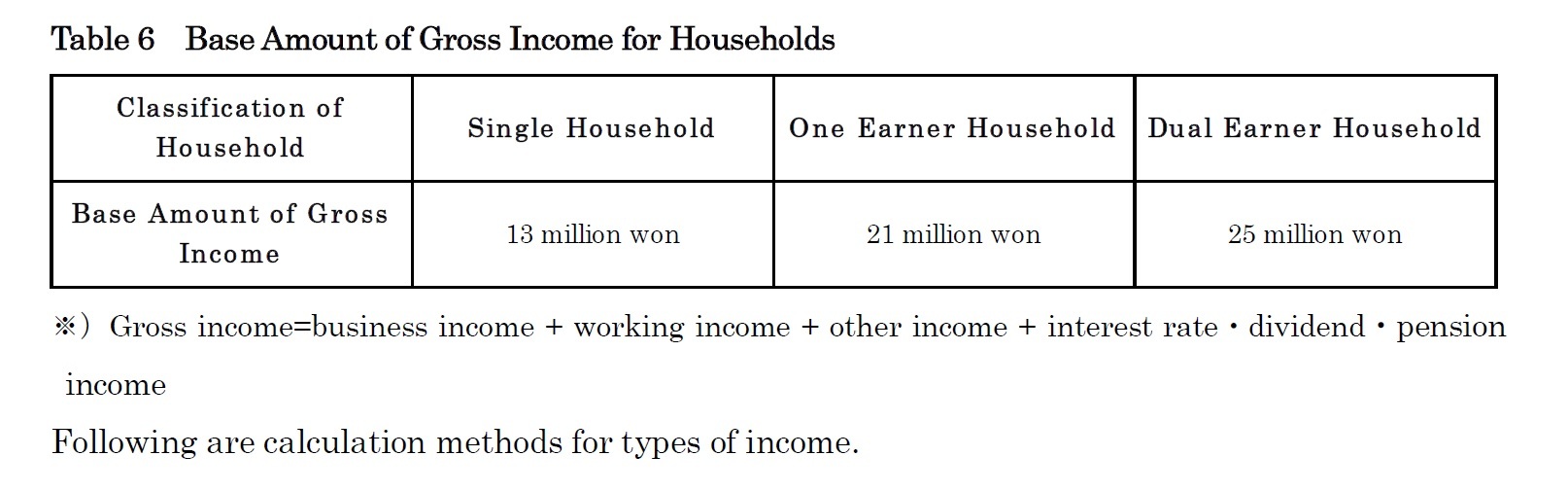

- EITC: To receive benefits, gross income of a married couple for the previous year is less than the base amount illustrated in Table 6.

{kind=link}

{kind=link}

{kind=link}

{kind=link}