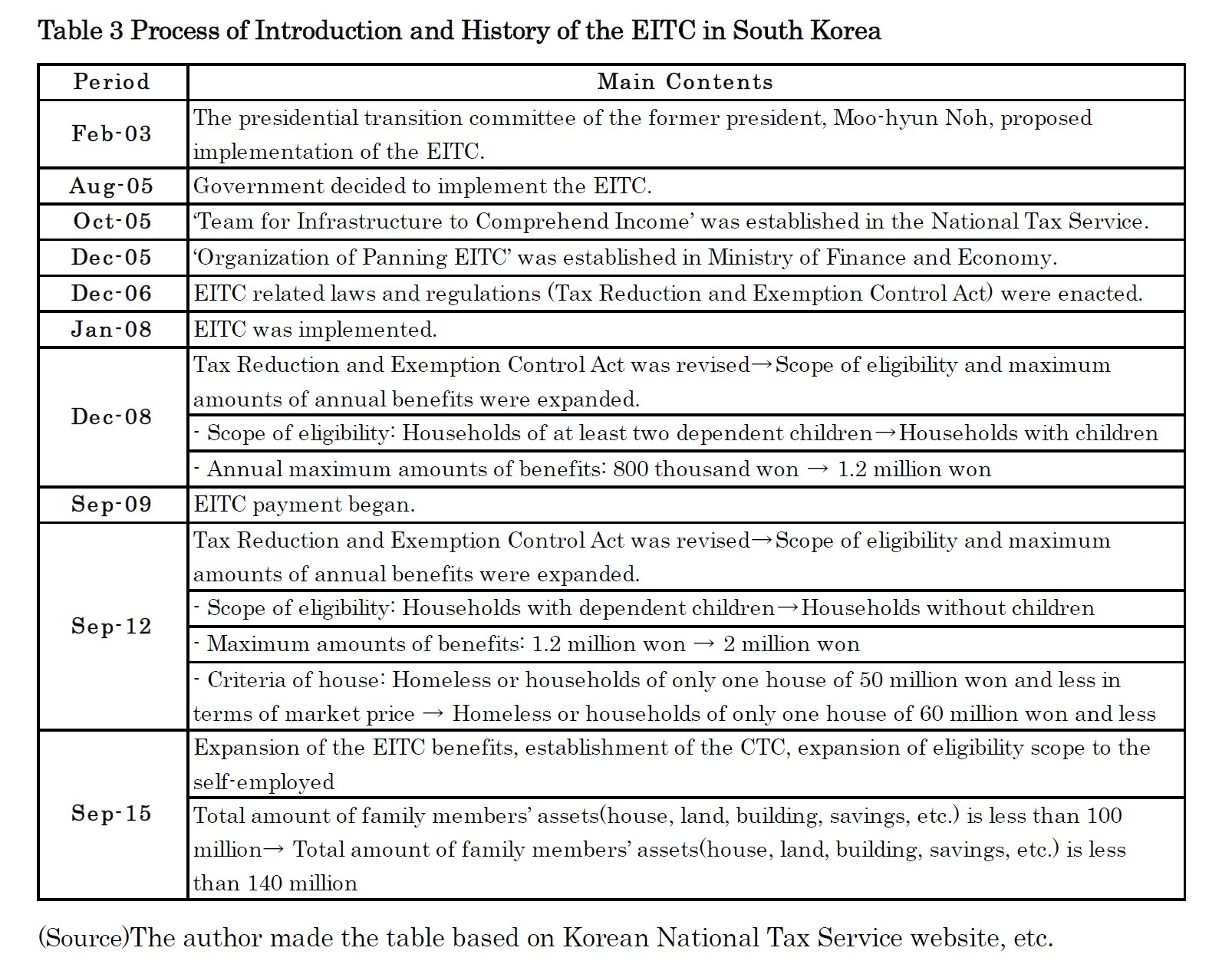

1|Process and Changes of the EITC

In 2003, the presidential transition committee of the former president Moo-hyun Noh proposed the implementation of the EITC, and the proposal was legislated. The EITC system related laws and regulations (Clause 2 and Clause 13, Article 100 of the Tax Reduction and Exemption Control Act) were enacted on December 26, 2006, and it was implemented from January 1, 2008; benefits have been paid since September 20098 (Table 3).

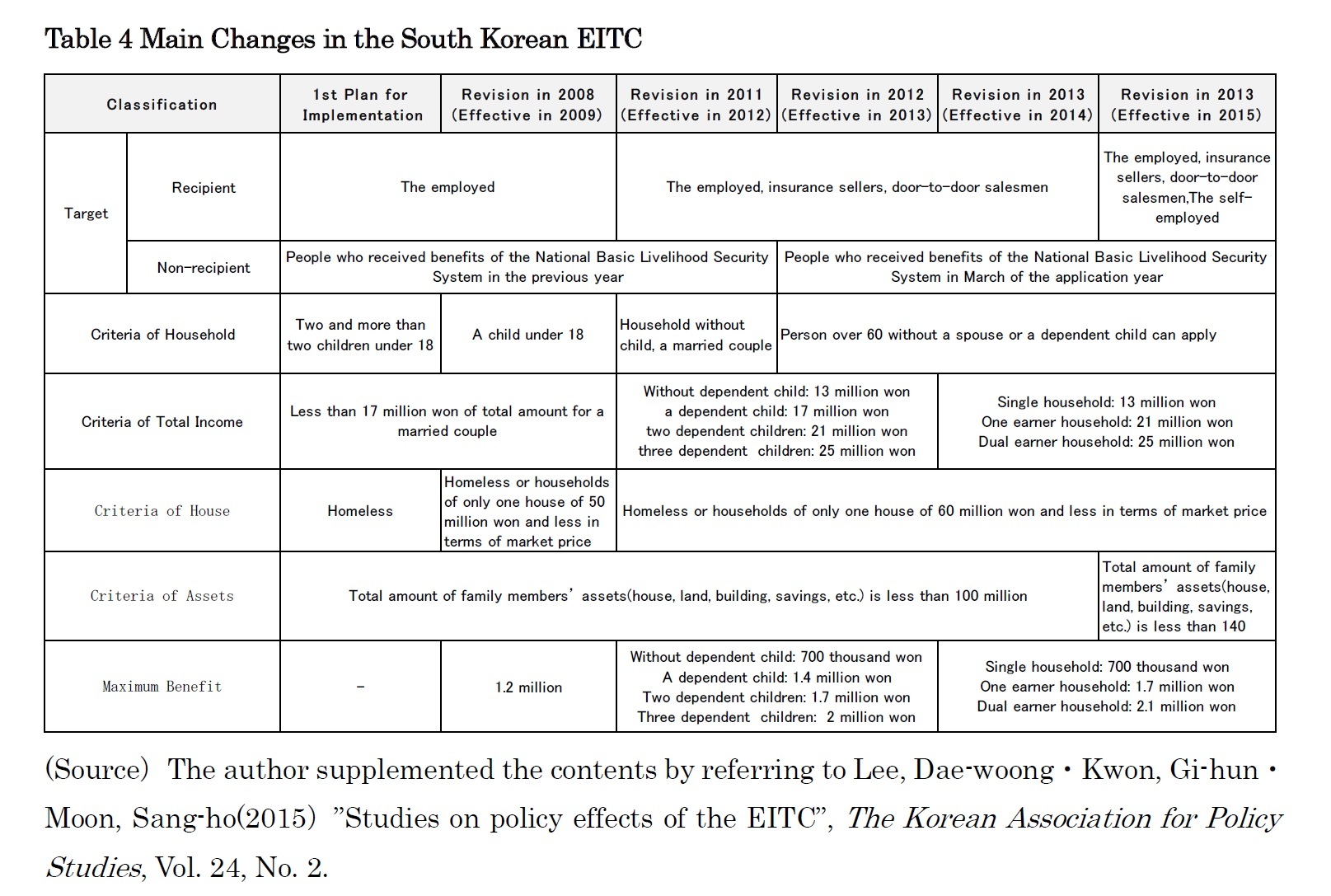

After the introduction of the EITC, amendments have been announced and the coverage has been expanded gradually. For example, the standard of household has been changed in the amendment of the year 2011, and families without dependent children (married households) also received benefits. Due to the amendment of the 2012, the elderly households of over 60 without a spouse or a child whom they support have been eligible since 2013. In addition, due to the amendment of 2013, the amount of benefits has increased since 2015 and benefits for children have been established. Please refer to Table 4 for main contents.

8 The South Korean EITC structure is basically referred to the EITC of the US.

2|Purpose of the EITC

The South Korean EITC system has purposes to raise work incentives and to support real income of workers and business owners (except for professionals, paid since 2015) who have difficulties in economic independence due to low income by providing the EITC. EITC payment is calculated on the basis of family members, annual gross income, and so on. Maximum payment for a year has been expanded from 1.2 million won of the beginning to 2.1 million won at present9.

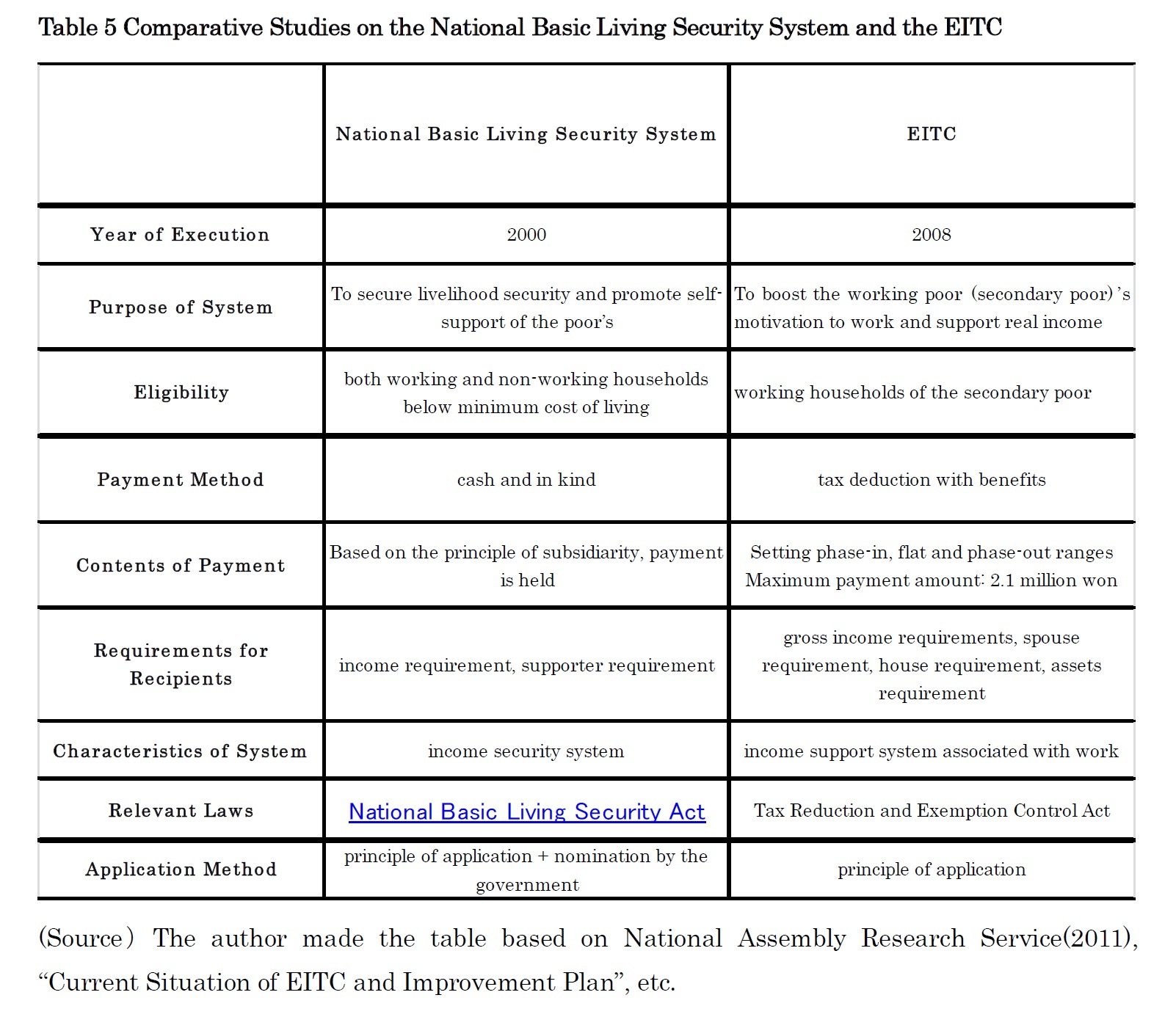

Table 5 describes the differences between National Basic Living Security System and the EITC. In October 2000, National Basic Living Security System, a public assistance system that corresponds to Japanese Livelihood Assistance System, was adopted to address problems under the previous public assistance system10.

9 In the initial phase, main target was ‘the secondary poor’; their household income is less than 120% of the minimum cost of living and they are excluded from receiving benefits of National Basic Living Security System. Working households whose annual gross income is less than 17 million won for the previous year received benefits up to 1.2 million won per year. 10 Kim, Myoung-jung (2004) "Social Economy Changes in Korea and Trends of Public・Private Social Expenditure after IMF System -Feature: Korean Social Policies after IMF System-", Foreign Social Security Study, No.146

{kind=link}

{kind=link}

{kind=link}